Executive Summary Electronic peer-to-peer (P2P) payments can serve as an effective alternative to other payment methods, such as cash and checks. Real-time payments (RTPs)—originally developed . . .

Executive Summary

Electronic peer-to-peer (P2P) payments can serve as an effective alternative to other payment methods, such as cash and checks. Real-time payments (RTPs)—originally developed to reduce settlement times and thereby lower float costs—have come into their own as means to facilitate interoperability between otherwise-closed P2P payments systems. That likely explains why 62 new RTP systems were created in the past decade, compared with a total of 22 in the prior four decades.

P2P payments and associated RTP rails are well-suited for payments where immediacy and finality are required, where the goods or services have already been delivered or are being supplied by a trusted provider, and where the payor is satisfied that the warranties provided by the payee are adequate and easily enforced. For such transactions, P2P payments are in many ways superior to cash, checks, or older EFT-based online debit transactions.

By contrast, P2P payments in general—including those made over RTP rails—are poorly suited to transactions where immediacy and/or finality are not required and where there are significant risks of nonperformance by the payee. This is because the speed and finality of P2P payments made over RTP rails makes it more difficult to detect, prevent, and rectify fraud, theft, and mistake. P2P-RTPs are thus particularly poorly suited to transactions where goods and services are delivered after payment has been sent and the payor does not have an established trust relationship with the merchant. In such circumstances, closed-loop or dual-message open-loop payment cards will typically be superior.

Organizations designing and implementing P2Ps and RTPs would do well to bear these lessons in mind and not pursue overly ambitious and impractical goals. Where those organizations are governmental entities—such as central banks—that have a remit to regulate payments, it is essential that they implement measures to mitigate potential conflicts of interest.

I. Introduction

This is the first in a series of ICLE issue briefs that will investigate innovations in and the regulation of payments technologies, with a particular focus on their effects on financial inclusion. The aim of this paper is to offer an overview of two important and related payment systems: peer-to-peer (P2P) and real-time payments (RTPs).[1] Subsequent papers in the series will look at specific aspects of these systems in greater detail.

In traditional payment systems, funds sent from one account to another can take from hours to days to clear and settle. These delays have an opportunity cost: once funds have been debited from a sender’s account, they are not available for use until they are credited at the recipient’s account. In addition, delays in clearing and settlement can contribute to counterparty risk for recipients. At the same time, there are tradeoffs between the speed and finality of payments and counterparty risk for senders.

In principle, P2P and RTPs hold significant potential to increase financial inclusion and enhance economic efficiency. But to do so successfully, such tradeoffs must be acknowledged and factored into system designs. Relatedly, it is important for system designers and regulators to understand both the likely use cases for P2P and RTP systems and the uses to which they are poorly suited. For example, some P2P and RTP evangelists have argued that they will replace credit cards.[2] As explored below, this seems unlikely for two reasons: first, credit cards have more effective mechanisms to address counterparty risk for consumers and, second, in many cases, credit cards better enable consumers to address timing mismatches between income and consumption.

P2Ps and RTPs come in various guises. Some are purely private systems, including P2Ps offered by Venmo, Zelle, and PayPal, and RTPs operated by The Clearing House, Visa, Mastercard, and PayUK. Some RTPs (such as India’s Unified Payments Interface, or UPI) are public-private partnerships. Other RTPs—such as Brazil’s Pix and the forthcoming FedNow system in the United States—are run by central banks. These various systems have adopted different approaches to implementation. By considering the particular system designs and the consequences of those differences, this paper offers tentative best practices for P2P and RTP design. Future papers will explore these issues in greater detail.

In order to put P2Ps and RTPs into the broader context of payment systems as they have evolved, Section II describes the means by which payments are cleared and settled, starting with an account of the basic process, followed by descriptions of some of the primary payment-settlement systems, including automated clearing houses, faster-payment systems, P2Ps, and RTPs. Section III considers the benefits and drawbacks to P2Ps and RTPs. Finally, Section IV offers concluding remarks.

II. Clearing and Settlement Systems

Bank accounts are essentially ledgers that record credits and debits. When funds move from account A to account B, a debit is recorded on account A and a credit recorded in account B. This is typically a four-stage process: authorization, verification, clearing, and settlement:

- Authorization is the process by which the sender authorizes a payment from A to B.

- Verification is the process by which the sender’s payment authorization is verified.

- Clearing is the process by which the banks reconcile the ledgers of accounts A and B. If there are insufficient funds in A to facilitate the payment, the transaction will not clear. (In some definitions, clearing is taken to comprise, in addition, the two steps above.)[3]

- Settlement is the process by which funds are transferred, either individually or in batches (often netted—see below), and the ledgers are updated.

Historically, this was primarily done through the use of checks and deposit slips. The signed check authorizes the transfer from the sender (debitor) account (A) and the deposit slip authorizes the receipt of funds by the creditor account (B). The bank—or banks, if the accounts are with different depository institutions—then verify the authenticity of the checks and deposit slips and clear the funds to be transferred. Finally, the bank(s) adjust the ledgers in each account, recording a debit in account A and a credit in account B.

Consider the simple case of a two-bank system with only one account holder in each bank. The owner of account A in bank X writes and signs a check to the owner of account B in bank Y authorizing the transfer of funds from A to B. In this case, X confirms the authenticity of the check signed by the owner of A and clears funds to be transferred to B. Meanwhile, settlement requires funds to be moved from X to Y, which entails the recording of a debit in X’s master ledger and a credit in Y’s master ledger. To avoid counterparty risk, while a debit will be recorded in A after clearing, a credit will only appear in B after settlement.

Now, consider the slightly more complicated case of multiple accountholders in each of the two banks. In this case, numerous accountholders in each bank write checks to account holders in the other bank. These checks are first cleared. Then, at the end of the day, the total amount of funds cleared between all accounts in X and Y would be calculated and any difference in the net amount would be settled by adjusting the ledgers of the two banks. As before, funds debited from senders’ accounts only appear as credits in recipients’ accounts following settlement.

In practice, there are many banks and many accountholders within each bank. On any day, some number of accountholders in each bank write checks to accountholders in other banks. It is therefore more efficient for clearing and settlement to occur on a multiparty basis. This led to the establishment of clearing houses, which are independent intermediaries that facilitate clearing and settlement. In 1863, the largest U.S. banks formed The Clearing House (TCH) for this purpose. The process is still essentially the same, however, with settlement occurring following the netting of amounts owed between each bank in the system.

A. Automated Clearing and Settlement

Electronic payments enable more rapid funds transfer. The earliest such payments were “wires,” which began in the 19th century, with information about the sender and recipient being sent between individual banks over telegraph wires. In 1970, TCH established the Clearing House Interbank Payment Services (CHIPS) to clear and settle wire payments for eight of its largest members. Membership was subsequently expanded to banks across the United States and internationally.

During the 1950s and 1960s, banks introduced computers and gradually shifted from paper-based ledgers to electronic ledgers. As the cost of computers and telecommunications fell, it became increasingly efficient to send information relating to smaller-value payments electronically, which in turn facilitated automation of the entire payments system. In 1968, UK banks introduced the first automated electronic clearing house, called Bankers’ Automated Clearing System (BACS).[4] In 1972, a group of California banks established the first automated clearing-house (ACH) network in the United States to clear and settle accounts electronically.[5] Other regional networks and the Federal Reserve (FedACH) followed and, in 1974, these networks established the National Automated Clearing House Association (NACHA). Similar networks were developed in many other countries, typically supported by—and, in many cases, run by—central banks.

B. Settlement Times

In the United States, settlement over NACHA and CHIPS originally took two to three days.[6] Settlement on payment systems in other jurisdictions, such as BACS in the United Kingdom, typically occurred on similar timeframes.[7] Over time, settlement times for payment systems have gradually been reduced. Most U.S. settlements now take only a day or less. Since 2010, FedACH has offered a same-day clearing/settlement service,[8] while NACHA has offered a similar same-day clearing/settlement service since 2016.[9] CHIPS settles at the end of the day over Fedwire.[10]

Separate from the ACH systems, real-time gross-settlement (RTGS) systems, such as Fedwire, are used for settling large-value payments between banks without netting. These typically settle immediately upon receipt, during hours of operation.[11] Because there is no netting, banks must either ensure they have sufficient reserves to send funds, or borrow funds to cover outgoing payments. Potential mismatches between outgoing and expected incoming funds can lead to cash hoarding, driving up demands for intraday borrowing, as occurred during the 2008 financial crisis.[12]

C. Fast Payments, Faster Payments, and Real-Time Payments

So-called “fast payments” or “faster payments” systems are RTGS systems designed to clear and settle smaller sums quickly between accounts. In general, such systems have the following features: (1) payment messages transmit and clear sufficiently quickly that payor and payee can see changes in their respective account balances more-or-less instantly (practically speaking, that means under a minute); (2) payment is final and irrevocable.[13]

In 1973, Japan introduced Zengin, the first nationwide fast-payments system, and many others have followed suit in the ensuing half-century.[14] An early driver of fast payments’ introduction of was the desire to reduce float (see Section III Part B below). More recently, interoperability among P2P payment networks has become a major driver, leading to the introduction of systems that operate continuously. Such round-the-clock fast-payment systems are typically referred to as real-time payments (RTPs). (Various other labels, including “instant payments,” are also used.)

With improvements in the speed and capacity of data processing and transfer, settlement times have gradually fallen. Indeed, some RTPs, such as TCH’s RTP, settle instantly. This requires payment service providers (PSPs) to maintain a balance with the settlement provider sufficient to “pre-fund” any payment (similar to RTGS). Indeed, some proponents of RTPs argue that instantaneous settlement is a defining feature of such systems.[15] Other fast-payment systems, such as the UK’s Faster Payments Service (FPS), continue to operate on a deferred-settlement basis but are nevertheless referred to as RTPs because the other criteria are met. For the purposes of this primer, a payment system is considered an RTP if transactions using the system:

- enable the payor and payee to see changes in their respective account balances instantly;

- result in final and irrevocable transfers of funds from payor to payee; and

- may be made 24 hours a day, seven days a week.

D. Peer-to-Peer Payments

As noted, one of the drivers leading to the introduction of RTPs has been peer-to-peer (P2P) payments. Most P2P payments systems began as closed systems. While transfers within these P2P systems would often occur in real time, transfers into and out of the system—including to other P2P systems—could take days. RTPs offer a solution to this problem, enabling interoperability among different P2P systems, as well as interoperability between traditional bank accounts and P2P systems.

The first electronic peer-to-peer (P2P) payment system was M-Pesa,[16] a pilot of which was established in Kenya in 2005 by Safaricom, a cellphone-service provider, and subsequently rolled out nationwide in 2007. M-Pesa was inspired by the sharing of air-time credits by cellphone users in various sub-Saharan African countries.[17] Realizing that such air-time credit sharing was effectively acting as a form of money transmission and had the potential to enhance financial inclusion and associated economic development, the UK Department for International Development provided a challenge grant to Vodafone to support the development of more formal systems.[18] Initially, Vodafone worked with its Kenyan affiliate, Safaricom, to offer subscribers the ability to purchase M-Pesa funds at registered retailers in exchange for cash, thereby effectively turning their cell phones into mobile wallets. Users could send funds to others via SMS. Over time, M-Pesa expanded into other markets[19] and built numerous service offerings, including online payments[20] and savings and loans.[21] It now enables funding of accounts via online bank debits.[22]

Numerous companies subsequently built wallet applications for smartphones that enable users to link their bank accounts. This allows them to add funds by debiting those accounts and to deposit funds by sending credit to their accounts. Users of these wallets can send funds directly to other users of the same wallet. Examples include Venmo, Zelle, PayPal, Google Pay, Apple Pay Cash, Cash App, Paytm (India), WhatsAppPay (currently in India and Brazil), ViberPay (currently in Greece and Germany), and China’s AliPay and WeChatPay.

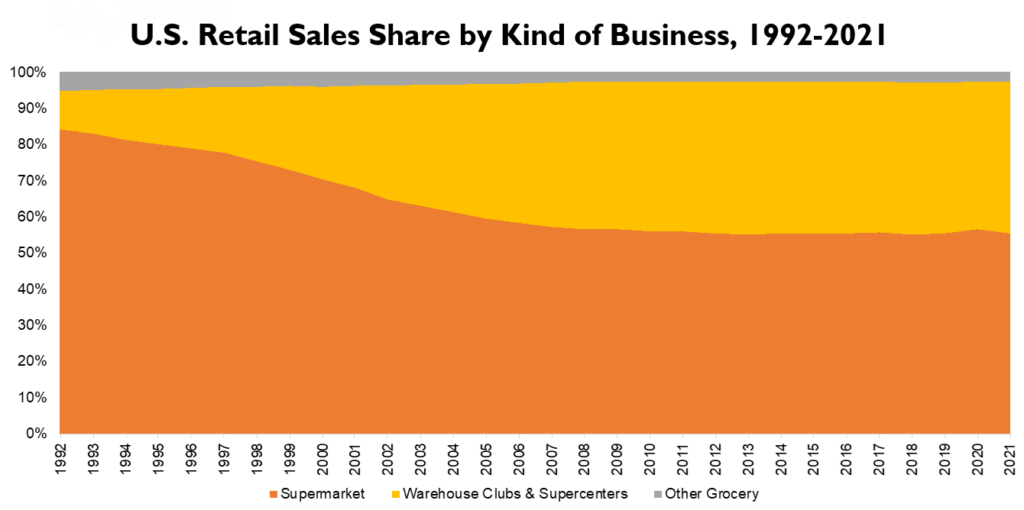

More recently, several bank associations and clearing houses have established RTP systems that facilitate interbank payments in real time, thereby in principle enabling interoperability between P2P systems. In some cases, interoperability has been baked in by design. For example, in 2016, the National Payments Corporation of India (NPCI) created the Unified Payments Interface (UPI), which is an RTP with an associated API that facilitates “push” credit payments and requests for payment for NPCI member banks.[23] As Figure I shows, around 400 banks are now part of UPI, which sees 8 billion monthly transactions with a total value of 14 trillion Rupees (about $170 billion).

SOURCE: NPCI[24]

SOURCE: NPCI[24]

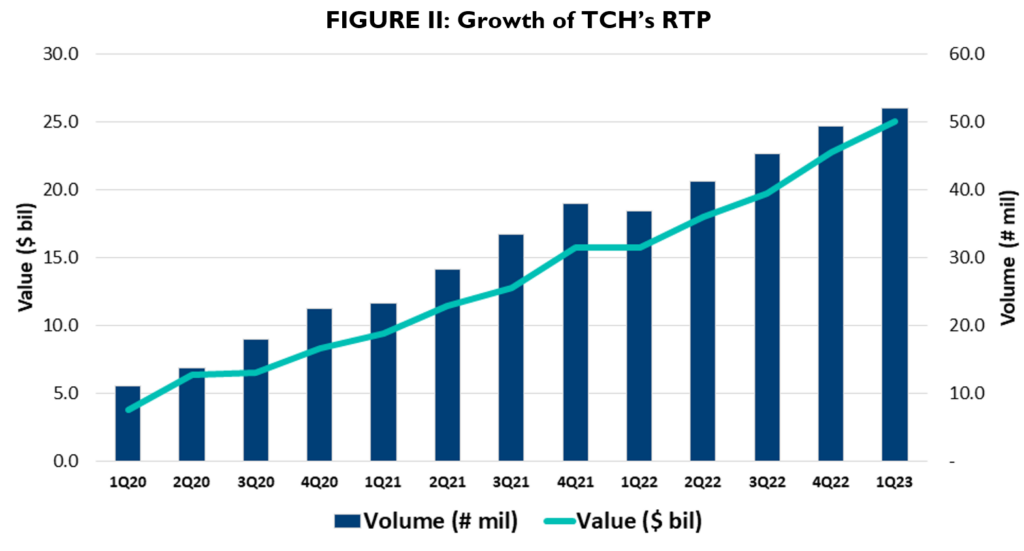

TCH introduced an RTP system for member banks in 2017.[25] As Figure II shows, the RTP has experienced explosive growth over the past three years and many U.S. P2P services now operate over it, effectively turning those P2Ps into RTPs.

In the first quarter of 2023 alone, TCH’s RTP facilitated 50 million transactions with a total value of about $25 billion. While P2Ps operating over TCH’s RTP are not necessarily interoperable, Zelle users can send funds directly to a counterparty’s bank account over RTP, even if that counterparty does not have Zelle installed at the time the payment is sent (they will have to install Zelle to be able to receive the funds).

SOURCE: TCH[26]

Central banks have also established and are establishing RTPs. Notable examples include Brazil’s Pix,[27] which was launched in 2020; the U.S. Federal Reserve’s FedNow, which launched in July 2023;[28] and Bank of Canada’s Real Time Rail.[29]

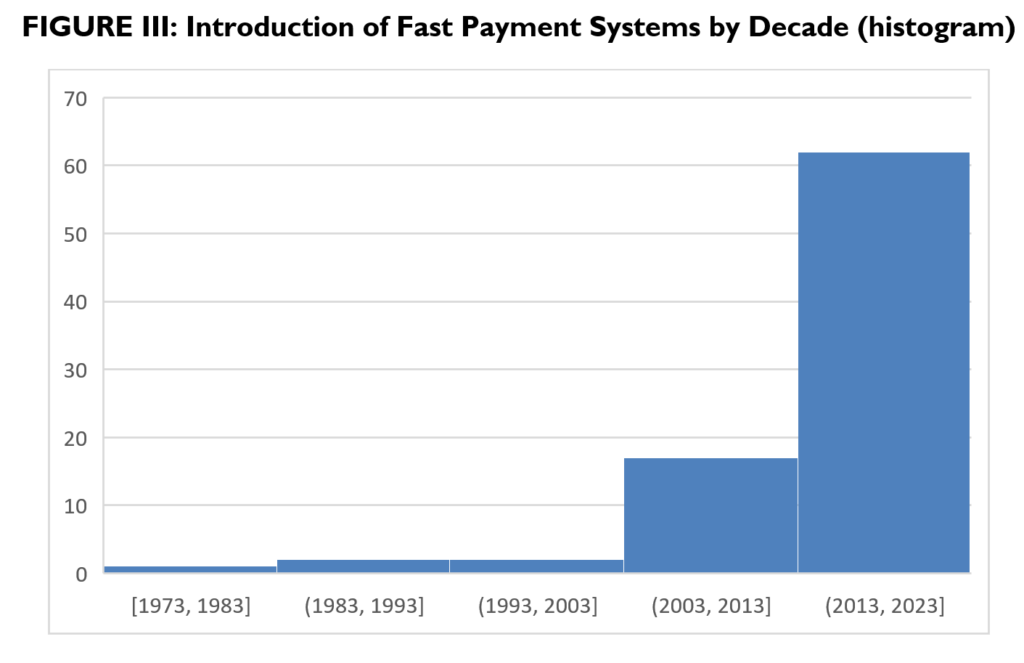

At the time of writing, fast payments systems have been introduced in 72 countries,[30] with several of those jurisdictions having more than one such system. As can be seen in Figure III, the vast majority of fast payment systems were introduced in the past decade; most of those are RTPs.

SOURCE: Based on information from ACI Worldwide[31]

E. Payment Cards

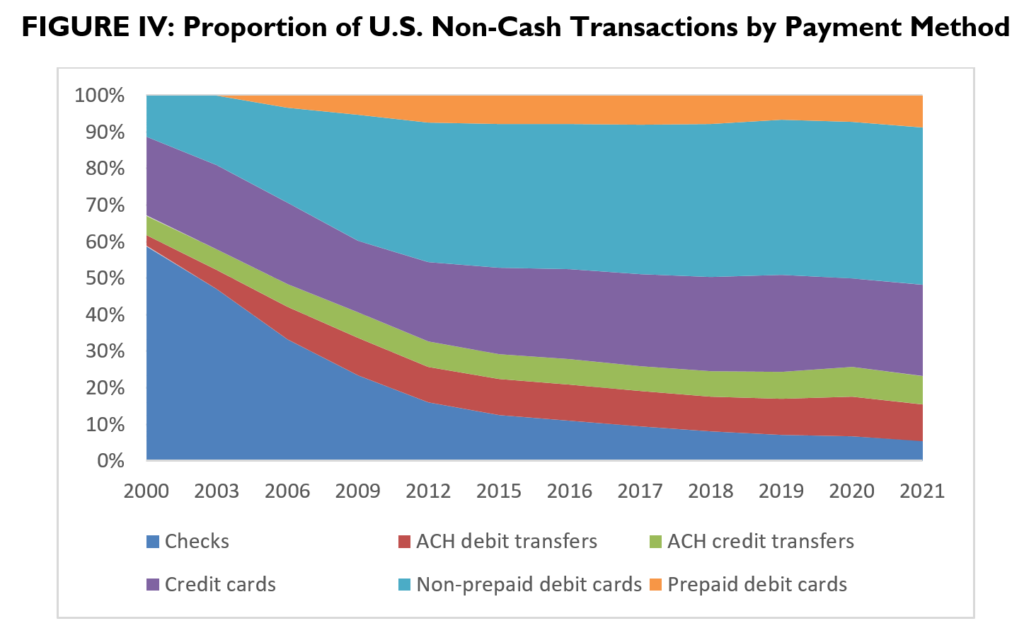

Payment-card networks emerged in the 1950s and have grown rapidly since, becoming the dominant means of retail payment in the United States and other OECD jurisdictions. Figure IV shows the dramatic increase in the proportion of U.S. transactions made using payment cards over the past two decades, which rose from 32% in 2000 to 77% in 2021.

The earliest payment cards—Diners Club and American Express—were and are still largely closed-loop systems, operating separately from bank networks. In the late 1950s, banks began operating their own payment-card networks. Over time, these bank-card networks gradually became more expansive and independent, with Visa and Mastercard becoming the largest such networks in the world, although there remain many competitors, including JCB, China Union Pay, and numerous national schemes.

Today, payment card systems can be divided into three main types:

- Closed-loop (three-party) credit cards

- Open-loop (four-party) dual-message (“signature”) systems

- Open-loop (four-party) single-message (“PIN”) systems

SOURCE: Federal Reserve Payment Study[32]

As the name suggests, closed-loop cards, such as American Express and Discover, operate largely outside the banking system. When a payor uses a closed-loop card to make a purchase, the card issuer decides whether the payment is legitimate (for example, by authenticating the payor and undertaking fraud checks) and whether the payor has sufficient credit; if it passes those checks, the issuer guarantees to pay the payee.

When a payor uses a card operating over an open-loop dual-message (“signature”) payment network, two messages are sent. The first is a request for authorization sent to the issuing bank, which confirms the authenticity of the card and checks whether the cardholder has sufficient credit remaining (for a credit transaction) or funds in their account (for a debit transaction). But the message is also parsed by the network, which is able to monitor for fraud. If authorized, the second message contains information confirming the actual amount of the transaction, which is then either added to the cardholders’ credit-card bill or debited from the cardholder’s account during clearing and settlement, as appropriate.

In this sense, the dual-message settlement process is analogous to a check, in that there is some delay in the posting and clearing of the transaction. The ability to put a “hold” on a dual-message card payment enables merchants to delay payment (sometimes by as much as several days), thereby reducing the likelihood of fraud and associated chargebacks.[33]

Single-message debit networks generally rely on the personal identification number (PIN) programmed on the card to authenticate a transaction. As a result, the only message that is required is a notification to the issuing bank to debit the account of the cardholder in the amount they have authorized, and to credit that amount to the account of the merchant—less the discount fee, which is paid to the acquiring bank. Because of the nature of the transaction, settlement can be effected over banks’ electronic-funds-transfer (EFT) networks, which were initially built to settle transactions at shared ATMs, and subsequently over networks of ATMs.[34] As with an ATM transaction, single-message debit transactions settle and funds are transferred more or less immediately from the consumer’s account.

One of the major advantages of card payments has always been that merchants are guaranteed payment (on the condition that they comply with the payment-card rules). The closed-loop systems and dual-message open-loop systems are not RTPs, however, because they do not settle instantly. As discussed below, this has certain advantages. Open-loop single-message systems, by contrast, can and increasingly do operate over RTPs for debit payments. For example, Visa Now and Mastercard Send enable debit-card holders to make real-time payments.[35]

III. Benefits and Drawbacks of P2Ps and RTPs

P2Ps and RTPs have some significant advantages over other payment systems. In particular, they can reduce counterparty risk for recipients, decrease opportunity costs of funds, and facilitate more advanced bilateral messaging between payor and payee. But they also have some drawbacks. Most notably, they entail high counterparty risk for payors; have engendered new types of fraud and theft risk; and lack any built-in credit facility. This section discusses these benefits (parts A, B, and C) and drawbacks (parts D, E, and F).

A. Reduced Counterparty Risk for Payees

Transfers sent using a system that nets payments, such as ACH or BACS, take some time to settle. As such, use of these payment systems creates a risk for recipients that payments will not arrive. This is particularly problematic for large-value transactions, such as home purchases, and for retail payments where the purchaser takes possession of the goods before the payment settles.

One way to reduce such payee counterparty risk is to use escrow (whereby funds are held on trust by a third party until the transaction is completed), banker’s drafts (also known as teller’s checks), or same-day wires. But these are all relatively costly solutions and hence only viable for larger-value transactions, such as the purchase of a car or a house. Wire transfers are clearly not suitable for transactions where the goods or services are of relatively low value, especially in cases where the purchaser will have left the premises before the wire has arrived, which would typically be the case for retail sales.

In comparison to wires, banker’s drafts, and escrow, credit and debit cards offer a lower-cost solution to counterparty risk. In both cases, payment is effectively guaranteed by the issuer (if the merchant complies with the card-network rules). In order to be able to accept credit or debit cards, however, the payee must establish a merchant account with an acquiring bank. While the costs and difficulty of establishing such an account has fallen with the introduction of modern payment-processing technologies, it can still be a barrier for merchants selling relatively small amounts of lower-valued items and is unlikely to make sense for individuals who make only occasional sales.

In contrast to these other payment methods, RTPs essentially eliminate counterparty risk for payees through the simple expedient of finality. This means that payees can see that funds have arrived nearly the moment that they are sent and know that the payment cannot be reversed. Meanwhile, when associated with a P2P system, RTPs can have very low setup costs, making them attractive for individuals and low-volume merchants.

B. Reduced Opportunity Costs

RTPs also eliminate the opportunity cost associated with funds that take time to settle. Compared with some other forms of payment—such as checks or credit cards, which can take a day or more to settle—the instantaneous settlement available with RTPs can create significant benefits for payees.

The Federal Reserve estimates that approximately 12 billion checks were written in 2021, with a total value of $27.47 trillion.[36] Of those, approximately 800 million, with a value of $240 billion, were converted to ACH. This means that the remainder—i.e., 11.2 billion checks, with a combined value of $27.23 trillion—were processed through conventional clearing. It typically takes about two business days for a check to clear and settle, which means that U.S. businesses require an additional gross daily “collection float” of about $210 billion to cover this lag between payment and settlement.[37] In practice, the net collection float required is far lower, because most checks are paid from one business to another; at any point in time, many businesses will be both debtors and creditors. Nonetheless, the need for even a few billion dollars of collection float is a significant cost, either reducing the amount of cash available for other uses or requiring lines of credit and associated interest payments. Using RTPs in place of checks can eliminate this float and associated costs.

C. Improved Bilateral Messaging

Another advantage of RTPs is improved documentation and bilateral communications. Some RTPs have introduced enhanced bilateral messaging between payer and payee.[38] Among other things, this enables senders to verify the identity of the account to which they are sending funds, which can reduce the incidence of mistakes. In addition, payees can send requests for payment to payors, which can simplify the payment process (but as noted below, can lead to fraud). In addition, messages can include human-readable documents such as invoices and receipts that can improve reconciliation by both parties.

D. Increased Counterparty Risk for Payors

While counterparty risk for payees is low when using a RTP, the opposite is true for those who use RTPs to pay for goods and services—and for largely the same reason: the finality of payments made using an RTP means that, once a payment has been initiated, it cannot be stopped or reversed. This reduces counterparty risk for payees and increases it for payors. If the goods or services purchased using an RTP system are not supplied or do not meet the payor’s expectations, the payor cannot initiate a reversal or chargeback. (The payor could send a request-for-payment to the recipient, but the recipient is under no obligation to comply.)

E. Fraud and Theft

Fraud and theft are perennial problems with payment systems of all kinds. Cash sales are particularly susceptible to “skimming,” whereby the till operator takes some of the cash tended (for example, by overcharging or by failing to ring up the correct amount in the register).[39] Cash is also susceptible to theft while in transit. To reduce such problems, merchants invest in such technologies as product bar codes, which prevent till operators from inputting incorrect prices (as well as improving inventory management) and security firms that use armored vehicles to transport cash.[40]

Non-cash payment methods are not subject to physical theft per se, but criminals have deployed all manner of schemes to use them to steal and defraud. Among other things, checks have been used to steal funds by impersonation of account holders; to defraud merchants by pretending to spend funds that are not available (“bouncing”); and to embezzle funds from companies. To address these problems, merchants introduced requirements like identity confirmation and caps on check amounts, while banks introduced card-based guarantees, and payor companies and banks introduced multi-signature requirements.[41]

Payment cards have suffered some similar problems. In response, issuing banks, merchants, card-payment networks, and other participants in the card-payments ecosystem have introduced rules and technologies designed to prevent fraud and theft. Early solutions included payment-authorization requirements; floor limits (above which authorization is required); and chargebacks (the ability to charge a transaction back to the merchant when an illegitimate transaction has not been authorized).[42] More recent innovations include machine-learning-based systems that monitor individual-payment patterns, with suspicious transactions subject to rejection or additional authorization requirements, as well as tokenized payments, which prevent the collection and transmission of personal account numbers (PANs).[43]

These rules and technologies have dramatically reduced fraud at the point of sale. But new technologies have created new opportunities for criminals to adapt old scams and develop new ones. The shift toward online transactions, for example, led to an explosion of card-not-present fraud.[44] As before, companies in the payment-network ecosystem have responded by developing systems that limit such fraud, such as the use of cookies, address verification, one-time passwords, velocity checks, multi-factor authentication, notification alerts, fraud scoring, and tokenization using token vaults.[45]

RTP systems are able to reduce some kinds of fraud and mistake. For example, the ability to check the identity of the recipient of the payee should, in principle, reduce the likelihood that a payment is sent to the wrong recipient. Raising the confidence of the payor, however, can also contribute to push-payment fraud. The lack of ability to reverse payments made over an RTP makes such systems particularly prone not only to push-payment fraud, but also to other kinds of frauds, as discussed in the subsections below.

1. Authorized Push-Payment Fraud

One of the most common types of payment fraud is also one of the oldest. A fraudster pretends to offer goods or services (often apparently in the name of a real business) and asks for upfront payment, but never delivers the goods or services. Such cons can take many forms, but increasingly they use online communications (websites, emails, app-based systems) and take advantage of irrevocable electronic transfers of funds.

This is the essence of “authorized push payment” (APP) fraud, which involves a con artist sending a request for payment (RFP) from a fake business (usually with a name that is very similar to that of a real business). The victim, assuming the request is from a legitimate business, then authorizes payment. APP fraud has become particularly prevalent in the United Kingdom since the introduction of the country’s Faster Payment System (FPS) RTP.[46]

2. Lightning Kidnappings, Data Breaches, and Malware Attacks

In some jurisdictions, the immediacy and finality of RTPs has been associated with an increase in other more disturbing crimes. Shortly after the introduction of Pix, Brazil saw a 40% rise in the phenomenon of “lightning kidnappings.” [47] Traditionally, such kidnappings involved victims being taken to an ATM and forced to take out money to secure their release. In the more recent iteration of the scheme, kidnappers simply demand that victims make a transfer to the kidnapper’s Pix account.

In response, Brazil’s central bank (BCB) capped the value of P2P Pix transactions made between the hours of 8 p.m. and 6 a.m. to R1,000 ($182, at the time).[48] Meanwhile, some Brazilians have taken matters into their own hands, responding to the threat of Pix kidnappings by purchasing secondary “Pix phones.”[49] Users load these mid-range Android phones with banking and Pix apps and leave them at home. Meanwhile, they delete all banking apps from their primary phone. While such an approach allows those who can afford a second phone to prevent criminals from stealing potentially large amounts of money, it is quite a costly solution.

Brazil’s Pix also appears to be particularly susceptible to cybersecurity risks. Over the past 18 months, there have been three significant cybersecurity violations relating to Pix accounts. The first three were data breaches that appear to have arisen as a result of inadequate cybersecurity protections at banks and fintech companies whose account holders had the Pix app installed.[50] One concern is that criminals may be seeking to use data gathered from these account breaches to create fake accounts in the names of real people, which they could then use to receive funds from the hostages they kidnap and/or engage in other criminal activities. They could then launder the money by using Pix to buy goods and, after depleting the account, destroy the phone used to create it.

The fourth breach, identified in late 2022, is by far the largest and potentially most serious, as it involved the use of a piece of malware nicknamed PixPirate, which targets Android versions of the Pix app itself and potentially affects all Pix customers using Android phones.[51] It would appear that PixPirate enables the theft of passwords used to access bank accounts, as well as the interception of SMS messages. In combination, these data could be used to defeat some types of two-factor authentication.

F. Governance

In some respects, the problems of fraud and theft discussed above may be considered part of a wider problem of “governance” of P2P and RTP systems. While space precludes a detailed discussion of this issue here (it will be the subject of a forthcoming paper in this series), from an economic perspective, it is important for payment-network operators’ incentives to be aligned with those of users. Among other things, this means that the operator of a payment network should not also have monopoly powers to regulate all other payment networks and PSPs, since this creates a potential conflict of interest whereby the payment network that the regulator operates is privileged relative to other networks and PSPs, thereby undermining competition and harming users.

In practice, central banks often operate at least part of the payment-network infrastructure and have broad regulatory powers with respect to payment-network operations. In such circumstances, conflicts of interest cannot be entirely avoided, but can at least be mitigated by ensuring that there is separation between the division responsible for operating payments infrastructure and the division charged with regulation. As the BIS Committee on Payment and Settlement Systems has noted:

A central bank needs to be clear when it is acting as regulator and when as owner and/or operator. This can be facilitated by separating the functions into different organisational units, managed by different personnel.[52]

Such best practices are followed by central banks such as the U.S. Federal Reserve and the Reserve Bank of Australia.[53] By contrast, at the Central Bank of Brazil (BCB), the same unit that operates Pix also regulates other private PSPs.[54]

G. No Automatic Credit

One of the key advantages of credit cards is that cardholders can pay for goods and services when they face temporary liquidity constraints—i.e., when they have insufficient funds immediately available to make a purchase. Most credit-cards issuers provide cardholders with interest-free credit from the time of a purchase until the bill is due, which typically ranges from 15 to 45 days, depending on when the purchase was made during the billing cycle. If the bill is settled in full by the due date, then no interest is payable. If the bill is not settled in full by the due date, then interest is payable on the outstanding amount.

Unlike payments made using credit cards, those made using a P2P-RTP do not inherently offer the payor the ability to spend more than they have in their account at the time of a purchase. Some P2P payments platforms have, however, developed credit facilities via buy-now-pay-later (BNPL) providers such as Afterpay (owned by Square), Affirm, Flexpay, Klarna, Sezzle, Splitit, and Zip.[55] BNPLs offer various ways to defer payment. For example, payors may be offered an option to defer the payment for a short period (such as four to eight weeks) at 0% interest, in which case the BNPL typically charges the retailer a transaction fee of between 2% and 8% (depending on the consumer’s credit score and the type of merchant).[56] Square charges the purchaser a standard rate of 6% plus a transaction fee of $0.30.[57] Alternatively, payors may be offered longer-term payment solutions, in which case, the merchant pays a transaction fee and the consumer pays the interest.[58]

Nonetheless, unlike credit cards, which automatically provide credit, BNPLs require the user to make an additional step when making a purchase, slowing the process down. And as noted, BNPLs can end up being more costly to the merchant and/or consumer than using a credit card.

IV. Conclusions

P2Ps and RTPs clearly have both advantages and drawbacks compared to other payment systems. They are well-suited for payments where immediacy and finality are required, where the goods or services have already been delivered or are being supplied by a trusted provider, and where the payor is satisfied that the warranties provided by the payee are adequate and easily enforced. For such transactions, payments made using P2Ps and RTPs are in many ways superior to cash, checks, or older EFT-based online debit transactions.

By offering a means of sending credit in real time between banks operating on the same system, RTP rails have facilitated more widespread use of P2P payments. Indeed, it is likely this characteristic, as much as improved bandwidth and processing speeds for online transactions, that explains the dramatic increase in the number of RTP systems over the course of the past decade.

By contrast, P2Ps and RTPs are poorly suited to transactions where immediacy and/or finality are not required, either because the goods or services have not yet been delivered or because of concerns regarding the quality of those goods or services. This is because the finality of P2P and RTPs makes it more difficult for the systems to detect, prevent, and rectify fraud, theft, and mistake. P2Ps and RTPs are thus poorly suited to transactions where goods and services are delivered after payment has been sent and the payor does not have an established trust relationship with the merchant. That includes many online purchases.

In such circumstances, closed-loop or dual-message open-loop payment cards will typically be superior to P2Ps and RTPs. For example, cardholders may dispute charges and make chargebacks if products have not been received or are defective. Acquirers and/or issuers also may delay payment until fraud checks have been completed, reducing the likelihood of a fraudulent transaction and thereby protecting merchants from chargebacks and protecting cardholders from fraud.

P2Ps and RTPs are also less well-suited to paying for goods or services when the payor does not have adequate funds in their bank account. While BNPLs may offer a solution in such cases, in most cases, it will be quicker and in many cases, it will be less costly to use a credit card. Subsequent papers in this series will look in more detail at issues relating to adoption of P2Ps and RTPs, the problem of APP fraud, and governance of RTPs.

[1] P2P is sometimes used in a more restrictive sense to mean “person-to-person”; the broader meaning used here includes person-to-person, person-to-business, and business-to-business.

[2] Marcela Ayres, Brazil’s Central Bank Chief Predicts End of Credit Cards, Reuters (Aug. 12, 2022), https://www.reuters.com/world/americas/brazils-central-bank-chief-says-credit-card-will-cease-exist-soon-2022-08-12.

[3] For example, the European Central Bank defines clearing as “the process of transmitting, reconciling and, in some cases, confirming transfer orders prior to settlement, potentially including the netting of orders and the establishment of final positions for settlement.” See, All Glossary Entries, European Central Bank, https://www.ecb.europa.eu/services/glossary/html/glossa.en.html (last accessed Aug. 19, 2023).

[4] History of Bacs, Bacs Payment Schemes Ltd. (Feb. 23, 2015), available at https://www.bacs.co.uk/DocumentLibrary/History_of_Bacs.pdf.

[5] History of Nacha and the ACH Network, Nacha (Apr. 20, 2019), https://www.nacha.org/content/history-nacha-and-ach-network.

[6] Id.

[7] As recently as 2012, standard settlement over BACS was 3 days. See, Payment, Clearing and Settlement Systems in the United Kingdom (CPSS Red Book), Bank for International Settlement Committee on Payment and Market Infrastructure (2012), at 455, available at https://www.bis.org/cpmi/publ/d105_uk.pdf.

[8] Press Release, Federal Reserve Announces Posting Rules for New Same-Day Automated Clearing House Service, Federal Reserve (Jun. 21, 2010), https://www.federalreserve.gov/newsevents/pressreleases/other20100621a.htm.

[9] Same Day ACH, NACHA, https://www.nacha.org/content/same-day-ach (last accessed Aug. 19, 2023).

[10] CHIPS, Modern Treasury, https://www.moderntreasury.com/learn/chips (last accessed Aug. 19, 2023).

[11] Fedwire Funds Services, Federal Reserve (May 7, 2021), https://www.federalreserve.gov/paymentsystems/fedfunds_about.htm.

[12] Gara Alfonso et al., Interbank Payment Timing is Still Closely Coupled, Working Paper (Jun. 2022), available at https://www.dnb.nl/media/raafily1/presentation-session-vii.pdf.

[13] The Bank for International Settlements offers the following definition: “Fast payments can be defined by two key features: speed and continuous service availability. Based on these features, fast payments can be defined as payments in which the transmission of the payment message and the availability of final funds to the payee occur in real time or near-real time and on as near to a 24-hour and 7-day (24/7) basis as possible.” See, Fast Payments – Enhancing the Speed and Availability of Retail Payments, Bank for International Settlements (Nov. 2016), at 1, available at https://www.bis.org/cpmi/publ/d154.pdf; Meanwhile, the Federal Reserve notes that: “To be classified as a faster payment, the payment option must 1) enable both payer and payee to see the transaction reflected in their respective account balances immediately and 2) provide funds that the payee can use right after the payer initiates the payment. And because of this, the payment is, by its nature, also irrevocable, meaning it cannot be reversed by the payer or the payer’s financial institution (FI) after it is sent.” See, Fast, Faster, Instant Payments: What’s in a Name?, Federal Reserve, https://www.frbservices.org/financial-services/fednow/instant-payments-education/whats-in-a-name.html (last accessed Aug. 19, 2023).

[14] Alfonso, supra note 12, at 5.

[15] The Distinctions Between Faster Payments and Real-Time Payments, Payments Journal (Aug. 18, 2020), https://www.paymentsjournal.com/the-distinctions-between-faster-payments-and-real-time-payments.

[16] The name is an abbreviation of “Mobile Pesa”; Pesa means money in Swahili.

[17] Mobile Money: From Transferring Cash by SMS to a Digital Payments Ecosystem (2000–20) in Russell Southwood, Africa 2.0, Manchester University Press (2022).

[18] Nick Hughes & Susie Lonie, M-PESA: Mobile Money for the “Unbanked”, Innovations (Winter and Spring 2007), 63-81, available at https://www.gsma.com/mobilefordevelopment/wp-content/uploads/2012/06/innovationsarticleonmpesa_0_d_14.pdf.

[19] What is M-PESA?, Vodaphone, https://www.vodafone.com/about-vodafone/what-we-do/consumer-products-and-services/m-pesa (last accessed Aug. 19, 2023).

[20] M-Pesa for Business, https://m-pesaforbusiness.co.ke (last accessed Aug. 19, 2023).

[21] M-Pesa: Credit and Savings, Safaricom, https://www.safaricom.co.ke/personal/m-pesa/credit-and-savings (last accessed Aug. 19, 2023).

[22] M-Pesa, Safaricom, https://www.safaricom.co.ke/personal/m-pesa (last accessed Aug. 19, 2023).

[23] Unified Payments Interface (UPI) Overview, NPCI, https://www.npci.org.in/what-we-do/upi/product-overview (last accessed Aug. 19, 2023).

[24] Statistics of NPCI, NPCI, https://www.npci.org.in/statistics (last accessed Aug. 19, 2023).

[25] Frequently Asked Questions, The Clearing House, https://www.theclearinghouse.org/payment-systems/rtp/institution (last accessed Aug. 19, 2023).

[26] RTP Quarterly Payment Activity (1Q23), The Clearing House, https://www.theclearinghouse.org/payment-systems/rtp.

[27] Julian Morris, Is Pix Really the End of Credit Cards? Truth on the Market (Sep. 28, 2022), https://truthonthemarket.com/2022/09/28/is-pix-really-the-end-of-credit-cards.

[28] About the FedNow Service, Federal Reserve Board, https://www.frbservices.org/financial-services/fednow/about.html (last accessed Aug. 19, 2023).

[29] The Real-Time Rail: Canada’s Fastest Payment System, Payments Canada, https://payments.ca/systems-services/payment-systems/real-time-rail-payment-system (last accessed Aug. 19, 2023).

[30] Prime Time for Real-Time Global Payments Report, ACI Worldwide (2023), https://www.aciworldwide.com/real-time-payments-report.

[31] RTP Quarterly Payment Activity (1Q23), The Clearing House, https://www.theclearinghouse.org/payment-systems/rtp (last accessed Aug. 19, 2023).

[32] Federal Reserve Payments Study (FRPS), Federal Reserve Board (2023), https://www.federalreserve.gov/paymentsystems/fr-payments-study.htm.

[33] Tyler DeLarm, Credit Card Authorization Hold- How and When to Use, Chargeback Gurus (Dec. 26, 2021), https://www.chargebackgurus.com/blog/credit-card-authorization-holds.

[34] Stan Sienkiewicz, The Evolution of EFT Networks from ATMs to New On-Line Debit Payment Products, Fed. Rsrv. Bank of Phila (Apr. 2002), https://papers.ssrn.com/sol3/papers.cfm?abstract_id=927473.

[35] Enable Individuals and Businesses to Move Money Globally, Visa, https://usa.visa.com/run-your-business/visa-direct/use-cases.html (last accessed Aug. 19, 2023); Send Money Quickly, Securely and Simply, Mastercard, https://www.mastercard.us/en-us/business/large-enterprise/grow-your-business/mastercard-send/mc-send-domestic-payments.html (last accessed Aug. 19, 2023).

[36] Federal Reserve Board, supra note 32.

[37] It should be noted that on the other side of the equation is “disbursement float,”—i.e., funds that have not yet left the payor’s account and are thus still available to the payor. The float is thus effectively a short-term loan made by the payee to the payor.

[38] For example, these features will be enabled for FedNow payments. See, The Real Value of Real-Time Payments, J.P. Morgan, https://www.jpmorgan.com/solutions/treasury-payments/insights/real-value-real-time-payments (last accessed Aug. 19, 2023).

[39] Skimming Fraud, Corporate Finance Institute (Jun. 8, 2020), https://corporatefinanceinstitute.com/resources/esg/skimming-fraud.

[40] Cash Larceny, Corporate Finance Institute (Jun. 7, 2020), https://corporatefinanceinstitute.com/resources/risk-management/cash-larceny.

[41] Check Fraud: A Guide to Avoiding Losses, U.S. Office of the Comptroller of the Currency (Feb. 1999), available at https://www.occ.gov/publications-and-resources/publications/banker-education/files/pub-check-fraud.pdf.

[42] David L Stearns, “Think of it as Money”: A History of the VISA Payment System, 1970–1984, PhD Thesis, University of Edinburgh (Aug. 2007), at 46 and 57-59, available at https://era.ed.ac.uk/bitstream/handle/1842/2672/Stearns%20DL%20thesis%2007.pdf.

[43] Julian Morris & Todd J. Zywicki, Regulating Routing in Payment Networks, International Center for Law & Economics (Aug. 17, 2022), available at https://laweconcenter.org/wp-content/uploads/2022/08/Regulating-Routing-in-Payment-Networks-final.pdf.

[44] Card Fraud Losses Dip to $28.58 Billion, Nilson Report (Dec. 2021), 5-7, available at https://nilsonreport.com/upload/content_promo/NilsonReport_Issue1209.pdf.

[45] Id.; see also, Card-Not-Present (CNP) Fraud Mitigation Techniques, U.S. Payments Forum (2020), available at https://www.uspaymentsforum.org/wp-content/uploads/2020/07/CNP-Fraud-Mitigation-Techniques-WP-FINAL-July-2020.pdf.

[46] Over £1.2 Billion Stolen Through Fraud In 2022, With Nearly 80 Per Cent of APP Fraud Cases Starting Online, UK Finance (May 11, 2023), https://www.ukfinance.org.uk/news-and-insight/press-release/over-ps12-billion-stolen-through-fraud-in-2022-nearly-80-cent-app.

[47] Bryan Harris, Brazil’s Criminals Turn to Flash Kidnapping as They Take Advantage of New Tech, Financial Times (Sep. 3, 2021), https://www.ft.com/content/225fd97c-ef82-4dfa-b09b-97b1671e1e00.

[48] Id.

[49] Alana Fernandes, Brasileiros Estão Apostando no Celular do PIX, Edital Concursos Brasil (May 21, 2022), https://editalconcursosbrasil.com.br/noticias/2022/05/brasileiros-estao-apostando-no-celular-do-pix-entenda-o-que-e-e-como-usar.

[50] The first, in late September 2021, resulted in the theft of information from nearly 400,000 Pix users due to a systems failure at state-owned Bank of the State of Sergipe (Banese). See Angelica Mari, Brazilian Data Protection Authority Investigates First PIX Data Leak, ZDNet (Oct. 6, 2021), https://www.zdnet.com/article/brazilian-data-protection-authority-investigates-first-pix-data-leak. See also Larissa Garcia & Alvaro Campos, New Leak Threatens Pix’s Credibility Central Bank Reports a Third Hacker Attack in Six Months, Now With 2,112 Keys Exposed, Valor International (Feb. 3, 2022). The second breach occurred in late January 2022 and involved the theft of data relating to approximately 160,000 Pix users from Acesso Pagamentos. See Gabriel Shinohara, Banco Central Comunica Vazamento de Dados de 160,1 Mil Chaves Pix da Acesso Pagamentos Segundo o BC, Não Houve Vazamento de Dados Sensíveis Como Senhas e Saldos, O Globo (Jan. 21, 2022), https://oglobo.globo.com/economia/banco-central-comunica-vazamento-de-dados-de-1601-mil-chaves-pix-da-acesso-pagamentos-25362574. The third breach, reported in February 2022 but relating to an incident in early December 2021, involved the theft of data from around 2,100 Pix users from LogBank. See Fernanda Capelli, Central Bank Confirms Another Leak of Pix Keys from Logbank, Programadores Brasil (Feb. 4, 2022), https://programadoresbrasil.com.br/en/2022/02/see-central-bank-confirms-yet-another-logbank-pix-key-leak.

[51] New Banking Trojan Targeting 100M Pix Payment Platform Accounts, Dark Reading (Feb 7, 2023), https://www.darkreading.com/risk/new-bank-trojan-targeting-100m-pix-payment-platform-accounts; PixPirate: A New Brazilian Banking Trojan, Cleafy (Feb. 3, 2023), https://www.cleafy.com/cleafy-labs/pixpirate-a-new-brazilian-banking-trojan.

[52] Central Bank Oversight of Payment and Settlement Systems, Bank for International Settlements Committee on Payment and Settlement Systems (May 2005), available at https://www.bis.org/cpmi/publ/d68.pdf.

[53] Policies: The Federal Reserve in the Payments System, Board of Governors of the Federal Reserve System (Jan. 2001), https://www.federalreserve.gov/paymentsystems/pfs_frpaysys.htm; Managing Potential Conflicts of Interest Arising from the Bank’s Commercial Activities, Reserve Bank of Australia (Feb. 2022), https://www.rba.gov.au/payments-andinfrastructure/payments-system-regulation/conflict-of-interest.html.

[54] Julian Morris, Central Banks and Real-Time Payments: Lessons from Brazil’s Pix, IInternational Center for Law & Economics (Jun. 1, 2022), at 13, available at https://laweconcenter.org/wp-content/uploads/2022/06/Lessons-from-Brazils-Pix.pdf.

[55] Erin Gregory, How Does Buy Now Pay Later (BNPL) Work for Businesses?, Tech Radar (Mar. 4, 2022), https://www.techradar.com/features/how-does-buy-now-pay-later-bnpl-work-for-businesses; Jaros?aw ?ci?lak, Top 10 Buy Now Pay Later Companies to Watch in 2022, Code & Pepper (Aug. 5, 2022), https://codeandpepper.com/buy-now-pay-later-2022.

[56] Id.

[57] Bring in More Business With Buy Now, Pay Later, Square, https://squareup.com/us/en/buy-now-pay-later (last accessed Aug. 19, 2023).

[58] Id.