ICLE Comments to FCC on Title II NPRM

I. Introduction

Writing on behalf of the International Center for Law & Economics (ICLE), we thank the Federal Communications Commission (“FCC” or “the Commission”) for the opportunity to respond to this notice of proposed rulemaking (“NPRM”) as the Commission seeks, yet again, to reclassify broadband internet-access services under Title II of the Communications Act of 1934.

The new NPRM emphasizes the principles of an “open internet,” but falls short of providing a concrete operational definition of what this entails.[1] The Commission’s vague and open-ended description of a “open internet” introduces enormous ambiguities that could grant the FCC unwarranted and expanded scope of discretion. In suggesting that openness equates to basic consumer access, without clear limitations or exceptions, the order leaves room for interpretation of what constitutes “open” access. This not only hampers stakeholders from understanding the boundaries of compliance, but also gives the FCC an opaque veil of authority that could be applied both expansively and inconsistently.

Some critics see the FCC’s pursuit of common-carrier regulation of broadband internet as an attempt to “control” an industry with vast economic and political significance.[2] That may be true. As we discuss in Section II, a more charitable criticism is that the Commission mistakenly believes that the provision of broadband internet is a natural monopoly that is best served by utility-style regulation. Alternatively, it could be argued that the FCC mistakenly believes that a dynamic and competitive industry marked by rapid innovation, improving quality, and falling prices can be effectively regulated as if it were a public utility. Under any of these rationales, Title II regulation is mistaken at best, and nefarious at worst.

Although much has changed since the 2015 Order,[3] nothing has happened that newly justifies the Commission reimposing Title II on broadband service. Perhaps recognizing the difficulty this poses, the Commission offers several new justifications for Title II regulation. In particular, “national security” is offered as a primary justification. In the 2015 Order, “net neutrality” was mentioned nearly 70 times. In contrast, the recent NPRM uses the term only a handful of times: once in the text and the others in only two footnotes. The 2015 Order mentioned “national security” only three times, while the NPRM uses the term more than five dozen times.

In addition, the FCC’s NPRM provides several other new justifications for sweeping regulation of broadband-internet access:

- COVID-19: “[T]he COVID-19 pandemic and the rapid shift of work, education, and health care online demonstrated how essential broadband Internet connections are for consumers’ participation in our society and economy.”[4]

- Federal spending on provider investments and consumer subsidies: “Congress responded by investing tens of billions of dollars into building out broadband Internet networks and making access more affordable and equitable, culminating in the generational investment of $65 billion in the Infrastructure Investment and Jobs Act.”[5]

- The need for a uniform national regulatory system: “[T]his authority will allow the Commission to protect consumers, including by issuing straightforward, clear rules to prevent Internet service providers from engaging in practices harmful to consumers, competition, and public safety, and by establishing a uniform, national regulatory approach rather than disparate requirements that vary state-by-state.”[6]

We caution the Commission to take care when relying on these justifications, for several reasons. First, the COVID-19 justification is at odds with the way history unfolded. U.S. broadband providers’ responses to the steep increase in demand during the pandemic was a demonstrable success of broadband competition (especially compared to how networks abroad fared).[7]

The Commission’s reliance on the passage of the Infrastructure Investment and Jobs Act (IIJA) is also a problematic justification for Title II regulation. The legislative process would have been a perfect time for Congress to legislate net neutrality or Title II regulation as it was debating the investment of tens of billions of dollars to encourage broadband buildout for the next decade or so. But no such provisions were included in the spending bills. If anything, this should indicate that the Commission should refrain from such an excessive regulatory intervention.

Even the Commission’s newly enacted digital-discrimination rules undermine the case for Title II regulation. Congress included a very terse statement that the Commission should look into impermissible discrimination in broadband deployment, but gave zero indication that it wanted Title II reclassification to serve as a remedy, even if such discrimination was found.[8] In short, if Congress intended to regulate broadband internet under Title II, it had numerous opportunities to do so in the recent past, but chose otherwise.

When it comes to national security, Congress has created a number of entities that have oversight powers.[9] But despite recent legislative investment in broadband deployment, Congress gave no indication that it wished the FCC to become a body driven by a national-security mission. Thus, the Commission’s attempt to step into this arena appears both redundant and outside its core competencies. This further suggests that imposing net neutrality under the guise of such justifications might be unfounded, rather than grounded in a changed internet landscape or emergent security threats.

Aside from these overarching concerns advising against Title II regulation, the following comments seek to evaluate the FCC’s numerous beliefs and conclusions, as well as answer questions posed by the NPRM.

In Section II, we report that, by most measures, U.S. broadband competition is vibrant and has improved dramatically since the COVID-19 pandemic. We show that, since 2021, more households are connected to the internet, broadband speeds have increased while prices have declined, more households are served by more than a single provider, and new technologies—such as satellite and 5G—have increased internet access and intermodal competition among providers.

In that section, we also conclude that a mere “incentive and ability” of providers to engage in practices that pose a threat to “internet openness” (however defined) is insufficient justification to impose outright bans on certain practices that have been demonstrated to enhance internet performance, foster investment, and improve consumer and edge provider well-being. Moreover, robust and increasing broadband competition would place a substantial check on the “incentive and ability” for provider attempts to engage in anticompetitive or harmful conduct.

Rather than promoting “openness,” Title II may serve to suppress it, as it would ban or regulate both existing practices or future innovative practices that simultaneously boost provider returns and improve internet users’ experience. As such, Section II argues that the heavy-handed regulation proposed by the NPRM is likely to both reduce investment returns and increase the uncertainty of those returns. This would thereby stifle future broadband investment, especially among small and rural providers.

As discussed in Section II.C.2, paid prioritization has been demonstrated to benefit consumers and edge providers and, in some, cases may be necessary to deliver some high-demand internet services. We also present evidence that throttling of application-service providers is virtually nonexistent and that consumers are largely indifferent to throttling policies as currently practiced. While the NPRM does not anticipate regulating data caps or usage-based pricing, we argue that there is a significant likelihood these practices could be scrutinized under the proposed “internet conduct” rules. Both practices have been shown to be especially beneficial to low-income or low-usage internet subscribers.

Section III describes how already-existing laws and agencies are well-equipped to deal with competition, consumer protection, and national-security issues. Many of the issues the FCC uses to justify extending its purview do not require Title II reclassification, or even action from the FCC itself.

Lastly, in Section IV, we demonstrate that the FCC’s proposed rules will certainly invite challenge under the “major questions doctrine,” which requires a clear grant of authority from Congress when an agency action exercises powers of vast economic and political significance. Moreover, based on recent Supreme Court precedent, there is a significant likelihood that the Commission’s proposed Title II regulation will be struck down by the courts. Reclassification of broadband as a Title II telecommunications service would clearly be an exercise of powers of “vast economic and political significance.” Broadband providers have invested billions of dollars per year into building out reliable high-speed networks throughout the country, serving hundreds of millions of consumers.[10] Nearly every U.S. resident, business, public agency, and other organization uses broadband internet over large portions of the day. Both federal and state governments have supported this continued buildout through subsidies to providers and consumers. As then-Judge Brett Kavanaugh put it when considering the 2015 Order, the “FCC’s net neutrality rule is a major rule for the purposes of The Supreme Court’s major rules doctrine. Indeed, I believe that proposition is indisputable.”[11] It is also clear the classification of broadband under the Communications Act is ambiguous, as every court to review the question has found it to be so.[12]

II. Title II Is Inappropriate to Regulate Broadband

The Commission’s NPRM proposes regulating broadband as a Title II telecommunications service. But such regulations are unnecessary to protect the public and will harm investment, competition, and innovation. Part II.A details the absence of evidence that would justify reclassifying broadband as a common carrier under Title II. Part II.B shows how the current “light-touch” regulatory approach under Title I promotes innovation and competition. Part II.C presents evidence that Title II reclassification will reduce investment, and Part II.D explains how the NPRM’s proposed rules will reduce innovation by broadband providers.

A. No Adequate Justification to Change Regulatory Classification of Broadband Providers

The NPRM argues that the Commission must restore Title II authority to “safeguard the open Internet” by “clear rules to prevent Internet service providers from engaging in practices harmful to consumers, competition, and public safety….”[13] But the NPRM’s arguments to support this assertion are weak, and the evidence is sparse.

Part II.A.1 argues that the alleged harms to openness are based on poor economic logic and lack any evidence demonstrating that broadband providers have reduced “openness” in the absence of Title II regulation. Part II.A.2 examines the logic of regulating broadband as a monopoly utility, and finds it wanting in light of competitive conditions in the market. Part II.A.3 furthers that argument by detailing the level of competition in the market for high-speed internet, noting the growth in the number of providers, the falling prices and increasing speeds made available, and the increased level of intermodal competition since repeal of the 2015 Order.

1. NPRM has not sufficiently supported its assertion of a threat to openness

In the NPRM, the Commission notes that:

We believe that the rules we propose today will establish a baseline that the Commission can use to prevent and address conduct that harms consumers and competition when it occurs. Above, we express our belief that consumers perceive and use BIAS as an essential service, critical to accessing healthcare, education, work, commerce, and civic engagement. Because of its importance, we further believe it is paramount that consumers be able to use their BIAS connections without degradation due to blocking, throttling, paid prioritization, or other harmful conduct.[14]

Relatedly, the Commission roots its proposed rules in the so-called “incentive and ability [of ISPs] to engage in practices that pose a threat to Internet openness.”[15]

But the NPRM’s proposed rules, rooted in the presumption of ISPs’ “incentive and ability” to engage in practices that threaten internet openness, rest on a speculative foundation, rather than any substantive record of violations. Given the voluminous scale of internet traffic, the evidence of actual infractions is remarkably scant. This paucity of evidence undermines the rationale for preemptive, industrywide prohibitions, which would be based on hypothetical future harms. The mere possibility of ISPs engaging in deleterious conduct does not, in itself, warrant imposing onerous rules that could impede investment in innovative business models.

The assertion that ISPs have the incentive and ability to harm open internet access lacks convincing substantiation of demonstrable harmful conduct.[16] Speculative harm cannot justify regulations that could dissuade ISPs from exploring novel and potentially pro-consumer arrangements. Where there is evidence of consumer ignorance of the tradeoffs inherent in various product offerings, the solution may lie in enhanced disclosure—providing notice and choice to consumers—not in the imposition of broad restrictions.

Furthermore, the Commission fails to distinguish between instances where so-called “paid prioritization” has pro-consumer benefits and where it may constitute an anticompetitive harm. Many business relationships that might be labeled as paid prioritization—such as Netflix’s collocation of data centers within different networks to expedite service and reduce overall network load—are unequivocally pro-consumer. Such arrangements are better understood as sensible network optimization, rather than as anticompetitive behavior.

This narrow focus on ISPs as a potential vector of consumer harm also overlooks the broader ecosystem in which content aggregators like Netflix or Google exert significant influence over access to content. These platforms can, and often do, have a more immediate effect on consumer access than do ISPs. While edge providers sometimes come under fire themselves (wrongly, in our view), it is relevant to assessing the desirability of these proposed rules whether edge providers are made more or less powerful if ISPs are constrained, and what effect that would have on consumer welfare. Relatedly, many of the concerns over blocking, throttling, and paid prioritization are, in essence, expressing a concern that these edge providers will be unable to successfully bargain with ISPs. This, however, is a strange basis for such rules, as many of these firms are as large as or larger than any particular ISP. Moreover, the power these large firms exert in business relationships with ISPs establishes conditions that have downstream benefits for all edge providers.

Thus, the NPRM’s concern over the need for “neutral” connection lanes fails to recognize that neutrality may not be the sole (or even the best) path to fostering innovation. Startups could benefit from making agreements with ISPs to ensure optimized data transmission, which could be more achievable and less costly than the NPRM suggests. Moreover, the emergence of distributed cloud computing blurs the lines between established firms and newcomers, as they often share the same infrastructure and delivery networks, muting the Commission’s concerns.

Before moving forward, the Commission should diligently investigate the likelihood of future harms absent regulation, considering that no concrete evidence has surfaced since the last two rounds of rules on this matter—or even prior—of ISPs using their alleged incentive and ability to affect consumers and edge providers detrimentally. The FCC should substantiate actual harm rather than legislate against conjectural threats. Moreover, the FCC might find that transparency rules alone, or even the mere risk of public disclosure without formal regulation, could sufficiently deter quality degradation without the need for more intrusive regulations.

2. Widespread use of high-speed internet does not render broadband internet a public utility

The Commission concludes that broadband internet access services are “[n]ot unlike other essential utilities, such as electricity and water” and that high-speed internet “was essential or important to 90 percent of U.S. adults during the COVID-19 pandemic.”[17] The Commission appears to argue that broadband internet is therefore an essential public utility and should be regulated as such.

But many essentials to human survival—shelter, food, clothing—are thus not subject to common-carrier regulations, because they are provided by multiple suppliers in competitive markets. Utilities are considered distinct because they tend to have such significant economies of scale that (1) a single monopoly provider can provide the goods or services at a lower cost than multiple competing firms and/or (2) market demand is insufficient to support more than a single supplier.[18] Water, sewer, electricity, and natural gas are typically considered “natural” monopolies under this definition.[19] In many cases, not only are these industries treated as monopolies, but their monopoly status is codified by laws forbidding competition. At one time, local and long-distance telephone services were considered—and treated as—natural monopolies, as was cable television.[20]

Over time, innovations have eroded the “natural” monopolies in telephone and cable.[21] In 2000, 94% of U.S. households had a landline telephone, and only 42% had a mobile phone.[22] By 2018, those numbers flipped.[23] In 2015, 73% of households subscribed to cable or satellite-television service.[24] Today, fewer than half of U.S. households subscribe.[25] Much of that transition is due to the enormous improvements in broadband speed, reliability, and affordability discussed in Part II.A.3.a. Similarly, entry and intermodal competition from 5G, fixed wireless, and satellite—as discussed in Part II.A.3.c—has meant that more than 94% of the country can now access high-speed broadband from three or more providers, thereby eroding the already tenuous claims that broadband-internet service is akin to a utility.

Regulating a competitive industry as a monopoly utility is what former Justice Stephen Breyer identified as a regulatory “mismatch,” which he defined as:

[A]n area where the rationale for regulation, judged by empirical fact, is not compelling, or where there are apparently less restrictive or more incentive-based forms of governmental intervention that can obtain regulation’s purported objective. [26]

As we note throughout these comments, the federal government already has in place many laws, rules, and policies that could satisfy many of the objectives the FCC seeks with Title II reclassification. In nearly every case, existing regulations are less-restrictive, more incentive-based, or less-capricious than common-carrier regulation under Title II.

3. Existing broadband competition renders common-carrier regulations unnecessary

The FCC seeks comment on the state of competition in broadband internet-access services.[27] The NPRM claims that more than one-third of households lack competitive choice for fixed broadband at speeds of 100/20 Mbps, and that 70% of rural households lack such choice.[28] Despite the fact that nearly one-in-eight households with at-home internet are mobile-only, the Commission concludes that fixed and mobile internet are not substitutable.[29] Against this backdrop, the FCC seeks comment regarding whether services with substantially different technologies can substitute for each other competitively, and whether consumers nationwide have an adequate choice of providers.[30]

By most measures, U.S. broadband competition is vibrant and has increased dramatically since the COVID-19 pandemic. Since 2021, more households are connected to the internet, broadband speeds have increased while prices have declined, more households are served by more than a single provider, and new technologies—such as satellite and 5G—have expanded internet access and intermodal competition among providers.

a. More households are served by two or more providers

Criticisms of the current state of broadband deployment tend to presume it results from widespread market failure. Specifically, the critics believe that too few Americans have affordable access to adequate broadband speed and capacity and that this, in turn, is the result of insufficient competition among broadband providers.[31] For example, in her speech announcing the FCC’s latest proposal to regulate internet services under Title II, Chair Jessica Rosenworcel claimed that 80% of the country faces a monopoly or duopoly for 100 Mbps or higher download speeds.[32] But, in fact, nearly all of the country has access to at-home internet, a vast majority has access to high-speed internet, and much of the country has access to these speeds from three or more providers.

The Federal Communications Commission (FCC) defines high-speed broadband as Internet service that offers speeds of at least 25/3 Mbps.[33] The IIJA defines a location as “unserved” if it has no internet connection available or only has a connection offering speeds of less than 25/3 Mbps.[34] A location is considered “underserved” if the only options available offer speeds of less than 100/20 Mbps.[35] The third iteration of the National Broadband Map, released in November 2023, indicates:[36]

- 8% of locations have access to connections of 25/3 Mbps or higher;

- 5% of locations have access to speeds of 200/25 Mbps or higher.

- Only 6.2% of locations are unserved, and 2.6% are “underserved” with connections of less than 100/20 Mbps.

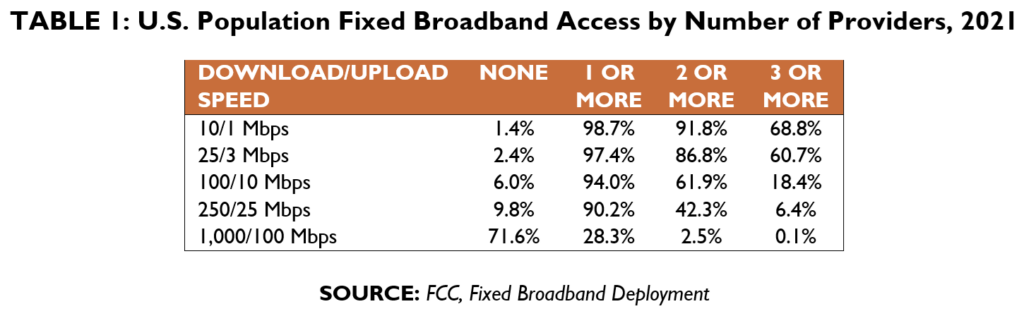

The most recent FCC data on U.S. broadband deployment finds that 90% of the population in 2021 was served by one or more providers offering 250/25 Mbps or higher speeds (Table 1).[37] That is more than double the share of the population five years earlier, when only 44% of Americans had access to such speeds.[38] In 2019, the FCC did not report the share of population with access to 1,000/100 Mbps speeds or higher. In 2021, 28% of the population had access to these gigabit download speeds.

Table 1 shows that, in 2021, more than 85% of the population was covered by two or more fixed broadband providers offering 25/3 Mbps or higher speeds and more than 60% of the country was covered by three or more providers providing such speeds. If satellite and 5G providers are included, then close to 100% of the country is served by two or more high-speed providers.

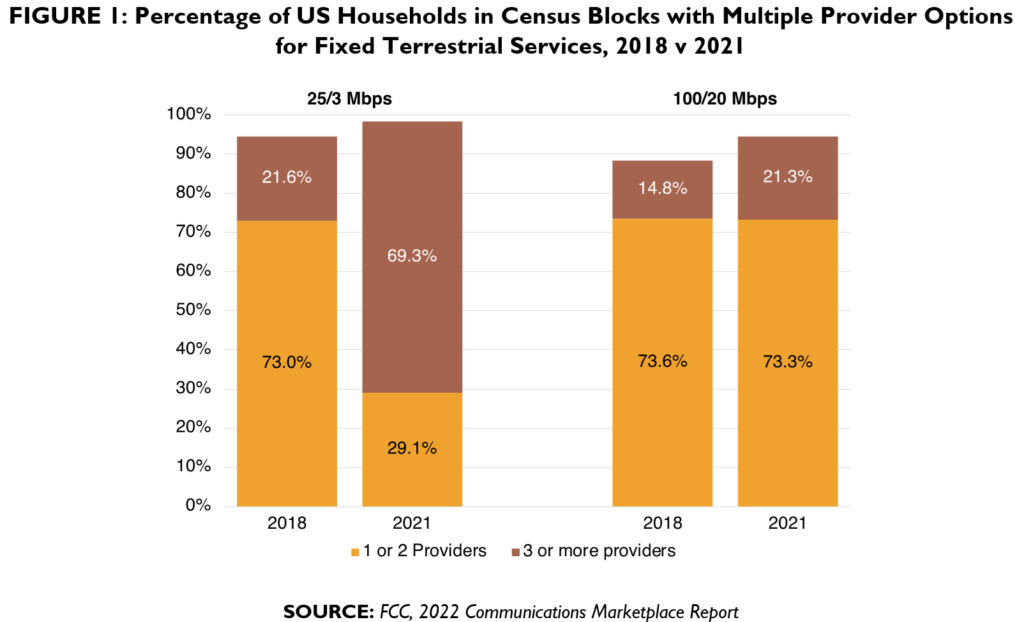

Moreover, the evidence indicates that broadband competition has increased over time, as measured by the number of competing high-speed providers (Figure 1).[39]

- 25/3 Mbps: In 2018, 73.0% of households had access to 25/3 Mbps speeds from only one or two fixed broadband providers and only 21.6% had access from three or more providers. In 2021, only 29.1% of households had access from one or two providers while 69.3% were served by three or more providers. Thus, the number of households served by three or more providers increased by 47.7 percentage points from 2018 through 2021.

- 100/20 Mbps: In 2018, 11.6% of households had no access to 100/20 Mbps speeds and 14.8% had access from three or more fixed broadband providers. In 2021, 5.4% of households had no access, while 21.3% were served by three or more providers. Thus, the number of households served by three or more providers increased by 6.5 percentage points from 2018 through 2021.

Since the 2018 Order[40] that reclassified broadband under Title I, broadband competition has increased. The share of households with high-speed fixed broadband connections offered by three or more providers has increased. Over the same period, entry and intermodal competition from 5G, fixed wireless, and satellite, as discussed in more depth below, has meant that more than 94% of the country can now access high-speed broadband from three or more providers. The growing consumer adoption of technologies that differ substantially from fixed broadband demonstrate that consumers view these technologies as competitive substitutes for each other.

b. Broadband speeds have increased while prices have declined

Critics of the current state of U.S. broadband competition claim that U.S. prices are among the highest in the developed world because the U.S. market is not as competitive as other jurisdictions. For example, the Community Tech Network asks rhetorically, “So why does the internet cost so much more in the U.S. than in other countries? One possible answer is the lack of competition.”[41] Their article includes a graphic in which U.S. internet is described as “expensive and slow” while Australia is categorized as “fast and cheap.”

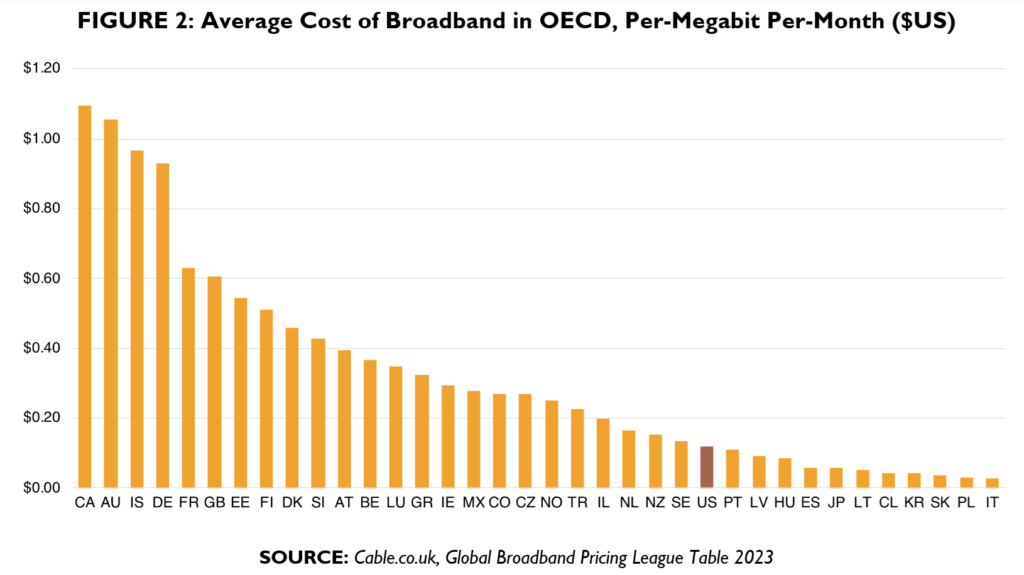

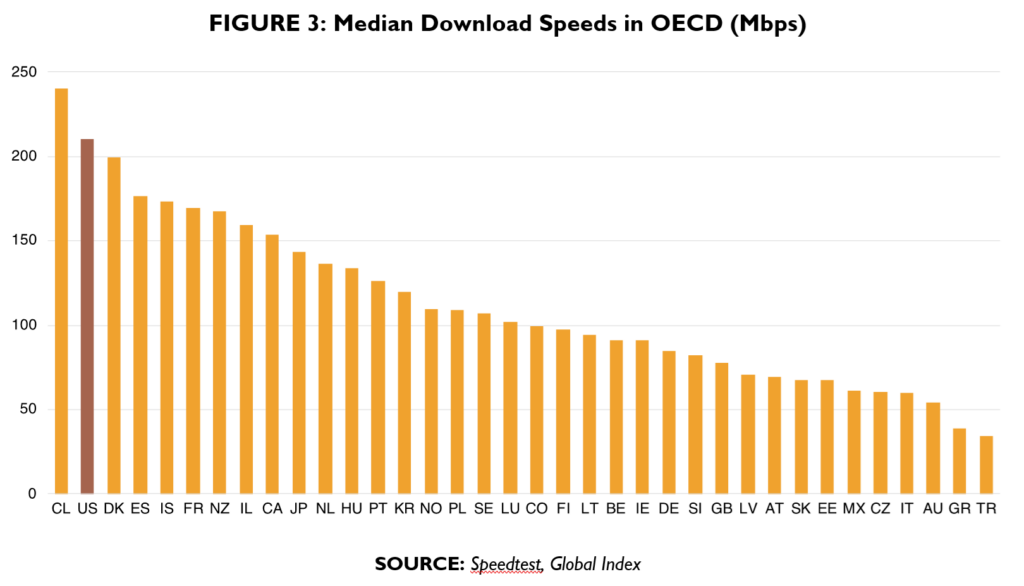

None of these claims appear to hold up under scrutiny. Instead, adjusting for consumption and download speeds, U.S. fixed-broadband pricing is among the lowest in the developed world. On a cost-per-megabit basis, the United States is among the least costly (Figure 2).[42] In addition, Speedtest’s Global Index of median speeds reports the United States as having the second-fastest median speed among OECD countries (Figure 3).[43]

Cross-country comparisons of broadband pricing are especially fraught, due to country-by-country variations in factors that drive the costs of delivering broadband and the prices paid by consumers. Deployment costs are driven largely by population density and terrain, as well as each country’s unique regulatory and tax policies.[44] Consumer choices often drive the prices paid by subscribers. These include choices regarding the mix of fixed broadband and mobile, speed preferences, and data consumption.[45]

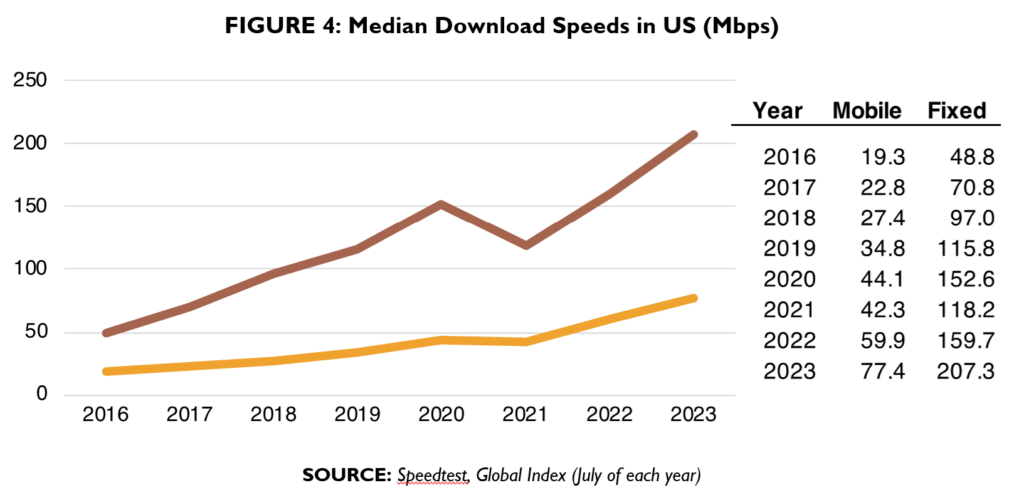

A broadband-pricing index published annually by USTelecom reports that inflation-adjusted broadband prices for the most popular speed tiers among consumers have decreased by 54.7% from 2015 to 2023, or 5.6% a year.[46] Prices for the highest-speed tiers have decreased by 55.8% over the same period. The Producer Price Index for residential internet-access services decreased by 11.2% from 2015 through July 2023.[47] The median fixed-broadband connection in the United States delivers more than 207 Mbps download service, an 80% increase over the pre-pandemic median speed (Figure 4).[48]

An industry experiencing increasing quality along with decreasing prices is consistent with an industry that faces robust, if not increasing, competition. By these measures, the U.S. broadband industry, under Title I regulation, is both competitive and dynamic. To date, proponents of Title II regulation have not demonstrated that net neutrality or other common-carrier obligations have or will improve internet speeds or pricing for consumers.

c. New technologies have increased intermodal competition

Nearly one-in-eight households with at-home internet are mobile-only.[49] According to Pew Research, 19% of adults who do not have at-home broadband report that their smartphone does everything they need to do online.[50] Even so, the Commission concludes that fixed and mobile internet are not substitutable,[51] and seeks comments regarding its conclusion that, “fixed broadband and mobile wireless broadband are not substitutes in all cases,” as well as its finding that broadband service and mobile-wireless service “enable[] different situational uses.”[52]

“All cases” is an unreasonably high threshold that fails to recognize the central question of competition—namely, how do or would consumers respond to a significant change in prices, quality, or terms and conditions? It’s been long-established that goods and services need not be perfect—or even close—substitutes to exert competitive pressure.[53] Indeed, as we discuss in this section, consumer adoption of 5G and satellite broadband indicate that many consumers view fixed, mobile, and satellite broadband as competitive substitutes. Thus, any FCC evaluation of broadband competition must account for competitive threats and pressures associated with intermodal competition.

One of the most important changes to occur since the last two net-neutrality rounds is the intensification of intermodal competition, primarily due to the introduction and expansion of satellite and fixed-wireless options, alongside the rapid growth of high-speed 5G technology. These developments have not only diversified the array of available services, but also enhanced their quality and accessibility. Moreover, the advent of widely available satellite and fixed-wireless technologies offers viable alternatives to traditional broadband, breaking down previous geographical and infrastructural barriers. Satellite-broadband services, 5G wireless, and fixed wireless now offer robust competition in areas previously served by, at most, one or two fixed-broadband providers. When considering the state of competition in broadband access, acknowledging this growing intermodal competition is crucial.

The advent of low-earth orbit (LEO) satellite broadband has dramatically expanded the geographic reach of high-speed internet access. Starlink satellite service has been made available to all locations in the United States.[54] Starlink’s reported speeds are between 25/5 Mbps and 220/25 Mbps.[55] Project Kuiper has successfully launched its first test satellites,[56] with commercial service expected to begin in the second half of 2024.[57] Starlink and Project Kuiper provide new broadband options, especially for rural and remote households previously limited to slow DSL services. S&P Global Market Intelligence reports:

Satellite broadband subs … have lingered in the 1 million to 2 million subscriber range since 2008 but finally broke above 2 million last year due largely to growth at Low Earth Orbit new entrant Starlink.” [58]

Research published in 2017—two years before the first launch of Starlink satellites—found that households in manufactured or modular homes are more likely to adopt satellite internet instead of wired, cable connections.[59] One explanation is that many manufactured homes are not cable-ready and lack the wiring for cable-internet connections. Thus, despite the higher monthly costs, the “all-in” cost of satellite connections is relatively lower. These consumers clearly considered cable and satellite to be competitors. In research published last month, Gregory Rosston and Scott Wallsten highlighted the importance of satellite broadband for competition in rural areas:

Starlink (and its likely future LEO competitors) are creating real, facilities-based broadband competition in areas that are currently not served by low-latency service or are served only by companies that rely on heavy subsidies. The opportunities, therefore are broadband competition in rural areas and large reductions in taxpayer spending on broadband availability.[60]

Citing estimates from research firm Omdia, the Wall Street Journal reports that about 43% of U.S. consumers had 5G mobile subscriptions as of June 2023.[61] The increasing deployment of 5G wireless technology has led to faster speeds, lower latency, and greater reliability, leading to 5G becoming increasingly competitive with fixed broadband.

- Recent data reports 5G download speeds of 80.0 Mbps to 195.5 Mbps among the three largest U.S. providers.[62] These speeds are sufficient to support a household of two to five users, streaming high-resolution and 4K video, streaming music, online gaming, remote work, and home-security services.[63] Moreover, these speeds far exceed the FCC’s definition of “high-speed broadband” as speeds of at least 25/3 Mbps.[64]

- Analysis of Speedtest data by Ericsson finds “the vast majority” of speed tests have measured a latency of less than 50 ms for both 4G and 5G.[65] In comparison, the FCC reports cable latencies of between 13 ms and 26 ms and fiber latencies of between 9 ms and 13 ms.[66]

As the 5G rollout continues and more spectrum is deployed, wireless speeds will continue to increase.[67] And enhancements like 5G fixed-wireless access (FWA) enable carriers to compete directly with wired services. For example, one study concludes:

We find that at current prices, full FWA entry to a cable-only market, which constitutes approximately 30 percent of all cable modem subscribers in the United States, would convert 18 percent of cable-only households to FWA …. In cable/fiber markets, we find that full FWA entry would convert 2 percent of households from cable modem to FWA ….[68]

B. Title I Enables Business-Model Experimentation and Differentiation

The NPRM assumes that net-neutrality rules assuring an “open Internet” are necessary to promote “edge innovation,” which creates consumer demand for high-speed internet and therefore “expanded investments in broadband infrastructure.”[69] But the NPRM essentially ignores the dynamic competition in broadband markets that leads to significant investment and innovation by broadband providers, as the market since the repeal 2015 Order shows. Part II.B.1 describes this dynamic competition in broadband markets. Part II.B.2 makes the case that Title I classification is what has allowed continued experimentation and innovation by broadband providers.

1. Broadband markets are characterized by dynamic competition

Potential competition plays a pivotal role in dynamic technology markets. The threat that new technologies like LEO satellite and 5G fixed wireless could disrupt incumbents’ market share stimulates continued infrastructure investment and innovation. Even where substitution currently is incomplete, the looming threat of competitive disruption disciplines behavior.

To this point, as we have previously noted,[70] broadband-market competition should be understood as dynamic, not static. Related to the question of intermodal competition (which can often present imperfect substitutes) are market dynamics driven by potential competition:

In dynamic contexts, potential competitors can have much greater importance. What today appears merely to be a potential competitor can obliterate incumbents tomorrow in acts of Schumpeterian creative destruction. To exclude such a competitor from the boundaries of the market would clearly be a mistake.[71]

Where traditional competition analysis tends to gauge competitiveness using narrow, static indicia such as price levels and market share, a focus on “dynamic competition” may be more appropriate in technology-driven markets like broadband service. Dynamic markets are not typically composed of many competitors making marginal price adjustments to capture small slices of market share. Instead, such markets often experience sequential competition: firms vie to capture the entire market (or most of it), with would-be competitors and new entrants attempting to disrupt incumbents by introducing innovative new products or business models to supplant previous technologies.

An assumption that more concentration must mean less competition stems from a blackboard model of “perfect competition,” where innovation is merely a competitive dimension that emerges from a healthy market structure, rather than innovation driving the evolution of market structures. Rivalry is, of course, important, but no one seriously believes we live in a world of perfect competition characterized by atomistic firms competing to produce commodity goods and services. Yet this simplistic structuralist view of markets is frequently advanced in policy discussions.[72]

As Harold Demsetz famously observed, “the asserted relationship between market concentration and competition cannot be derived from existing theoretical considerations and that it is based largely on an incorrect understanding of the concept of competition or rivalry.”[73] In the case of natural monopolies, scale economies may make it more efficient for one firm to produce a good or service in a given market than it would be for two or more firms. Scale economies arise when high fixed costs are spread over a larger number of goods, allowing larger firms to enjoy lower per-unit costs of production. Due to economies of scale, markets like broadband, with high fixed costs, will tend to have fewer firms than markets with lower fixed costs. But Demsetz demonstrated that, even then, competition for the market itself can lead to an efficient result that prevents the typical welfare harms attributed to monopolies.[74]

The oft-neglected literature on dynamic capabilities and organizational strategy, by contrast, supports the supposition that innovation drives market structure.[75] For the last several decades, this literature has demonstrated that static price-effect-focused analysis is insufficient to understand dynamic markets. For dynamic markets, instead, it is performance that matters, with price as a secondary consideration and innovation as an important component of performance.[76] So long as a market remains contestable, even if it’s highly concentrated, firms’ performance will determine the likelihood of new entrants. It is pressure from those potential new entrants that continues to drive market competitiveness.[77]

Indeed, in highly dynamic economies, particularly those characterized by scale economies, there can be just as much reason to be concerned about too many competitors as by too few. Further, these dynamic markets tend to see a continual rebalancing between equilibrium and disruption:

With dynamic competition, new entrants and incumbents alike engage in new product and process development and other adjustments to change. Frequent new product introductions followed by rapid price declines are commonplace. Innovations stem from investment in R&D or from the improvement and combination of older technologies. Firms continuously introduce product innovations, and from time to time, dominant designs emerge. With innovation, the number of new entrants explodes, but once dominant designs emerge, implosions are likely, and markets become more concentrated. With dynamic competition, innovation and competition are tightly linked.[78]

Thus, in any given market at a given time, there is likely some optimal number of firms that maximizes social welfare.[79] That optimal number—which is sometimes just one and is never the maximum possible—is subject to change, as technological shocks affect the dominant paradigms controlling the market.[80] The optimal number of firms also varies with the strength of scale economies, such that consumers may benefit from an increase in concentration if economies of scale are strong enough.[81] Therefore, in dynamic markets characterized by high fixed costs and strong economies of scale, like broadband markets, the optimal number of firms is reached much more quickly than in, for instance, relatively more commodity-like markets.

Broadband has many of the attributes of a dynamic market, which tends to make static analyses of broadband competition fail to accurately appreciate competitive realities.[82] Broadband markets are driven by technological trends and can be disrupted by rapid modal shifts (e.g., from DSL to cable, or, looking forward, from cable to 5G wireless, satellite, and fixed wireless). Moreover, the infrastructure necessary to deliver broadband requires both long-term planning, as well as substantial sustained investment. Firms in broadband markets are driven not merely by potential entrants today, but by the necessity of intense and expensive planning for future shifts in technology and consumption preferences. Thus, firms operate with an eye toward future competitive pressures, not merely in response to winning market share in the present.

Contrary to some assumptions, the U.S. broadband market is characterized by a significant amount of entry (and exit). As Connolly & Prieger find:

The striking conclusion is that there is a tremendous amount of dynamic activity in the US broadband market. In the national market, the entry rate averages 14-19% annually, which is greater than the entry rates the economic literature has found for many other industries. The exit rate for broadband is also higher than for other industries, but not as high as the entry rate, so that net entry averages 3.1% annually. With narrower geographic or service type market definitions, the entry rates average from 24% to an astounding 49% per annum.[83]

Thus, broadband providers must balance the need to offer attractive pricing in response to immediate competitive pressures with a simultaneous need to make risky and costly investments in technological upgrades in order to compete with advanced technologies that may not be implemented for a decade or more.

Just as market share is a poor indicator of competition, basic accounting measures of profitability and investment often fail to demonstrate how risk/return expectations are realized in dynamic markets over the entire innovation lifecycle. A very large and very profitable ISP may have experienced prior negative returns on invested capital, a result of the need to assume risk and make enormous investments under conditions of uncertainty. The broadband market is constantly evolving as a result of historical and ongoing infrastructure investment, rapidly changing technology, the evolution of content and content-delivery technology, new regulations, and shifting usage patterns, among other factors. Facilities-based competition (e.g., among fiber, cable, mobile, and satellite) has ebbed and flowed depending on these various characteristics, but it has consistently produced higher-quality connectivity at lower quality-adjusted prices. An accurate assessment of competitiveness in broadband markets must take account of all these characteristics.

Further, it is well-known that process and product innovation does not arise solely from new entry; incumbent firms frequently are important sources of innovation, as well as increased market competitiveness.[84] Dynamic analysis does take entry seriously, but it is much more sensitive to potential entry as a constraint on incumbents than a structuralist view would permit. Thus, for example, an incumbent broadband provider that offers a 250 Mbps tier must consider the potential capabilities of an existing competitor that only offers 100 Mbps service; it must incorporate potential threats from that competitor in its decision matrix when evaluating whether to upgrade its network to 1 Gbps in order to retain its customer base. An incumbent’s dominant position can quickly erode thanks to imperfect in-market substitutes, as well as from out-of-market firms that may decide to enter in the future.[85]

2. Title I classification promotes dynamic competition

The debate surrounding the optimal regulatory framework for broadband services often hinges on finding a balance that fosters innovation and consumer welfare without stifling competition. The broadband industry has thrived, for decades delivering lower prices and faster speeds under a Title I classification.[86] History has demonstrated that a light-touch regulatory regime under Title I of the Communications Act is the most conducive environment to achieve these objectives.

One of the primary functions of a firm is to discover consumer needs, a process that frequently requires firms to “think outside the box.” To attract and retain customers, firms must experiment with offerings that introduce competition from unexpected quarters and keep competitive pressures in place through technological and business-model innovation.

Light-touch regulatory frameworks are inherently more compatible with this approach than are more onerous regimes, like Title II of the Communications Act. For example, in 2011, MetroPCS attempted to introduce a limited data plan offering subsidized, unlimited access to YouTube and other content providers, targeting price-sensitive consumers.[87] This plan, though unconventional, was poised to help bridge the digital divide by making wireless data more accessible to a segment traditionally underserved by larger carriers. This type of business model is a non-neutral form of paid prioritization, but it would very likely have helped price-conscious consumers access more internet services. MetroPCS ultimately abandoned this plan, and such a plan would almost certainly run afoul of the proposed rules in this NPRM.[88]

Since then, ISPs have experimented with other potentially non-neutral paid-prioritization approaches that nonetheless would yield enormous consumer surplus, such as AT&T’s Sponsored Data program[89] and T-Mobile’s Binge On.[90] Such business models provide more choices, potentially lower prices, and introduce competitive threats to other players in the market. Ex ante rules that presumptively ban this kind of experimentation foreclose the ability to discover if such models actually serve the interests of consumers in practice.

And the harms that flow from reduced innovation affect not just ISPs and their consumers, but all parts of the internet ecosystem. As Sidak and Teece have observed:

The lost benefits [of bans on paid prioritization] would affect both end users and suppliers of content and applications. Optional business-to-business transactions for QoS will enhance the efficiency of traffic flow over broadband networks, reducing congestion. That enhanced efficiency benefits both the end users receiving content or applications and the content providers whose content or applications are demanded. Superior QoS is a form of product differentiation, and it therefore increases welfare by increasing the production choices available to content and applications providers and the consumption choices available to end users. Finally, as in other two-sided platforms, optional business-to-business transactions for QoS will allow broadband network operators to reduce subscription prices for broadband end users, promoting broadband adoption by end users, which will increase the value of the platform for all users.[91]

This follows from the nature of ISPs as platforms sitting at the center of a two-sided market. On one side are end users who pay the ISP for access to the internet; on the other are content providers who want access to the end users. A ban on paid prioritization assures that the ISP can monetize only one side of the market. Aside from putting upward pricing pressure on end consumers, this also has a detrimental effect on the overall value of the platform for users and content providers alike.

Prescriptive ex ante regulations under Title II amount to per se bans on certain conduct, without even inquiring whether such conduct is a net harm. Antitrust law, which is sensitive to exactly the sort of vertical harms that are the subject of concern in this NPRM,[92] has developed rule-of-reason analysis to parse when challenged conduct is harmful to consumer welfare.[93] That is, antitrust law does not assume that vertical restraints always harm consumers, but has learned that, in many cases, vertical restraints are a net benefit. But this analysis always occurs ex post, allowing companies to experiment with innovative business models like the many variations of paid prioritization.

C. Title II Reclassification Introduces Regulatory Uncertainty

The Commission tentatively deems unsubstantiated the 2018 Order’s conclusions that ISP investment is closely tied to the Title II classification.[94] This is because the Commission now concludes that network-infrastructure owners make long-term, irreversible investments and that the adoption of orders reclassifying broadband internet-access services would be unlikely to change these investment decisions. In addition, because the Commission received conflicting viewpoints on the actual effect of Title II classification on investment, it concludes that no one can “quantify with any reasonable degree of accuracy how either a Title I or a Title II approach may affect future investment.”[95] Instead, the Commission tentatively concludes that changes in ISP investment following adoption of reclassification orders were more likely related to factors such as economic conditions, technology changes, and general business decisions, rather than to Title I or Title II classification.[96] The Commission seeks comments on these findings, beliefs, and conclusions.

Put simply, Title II reclassification will hinder investment. The see-sawing between Title I and Title II regulation over the years has already injected regulatory uncertainty into the broadband market. Reimposing Title II regulations will inject additional uncertainty.[97] This uncertainty is compounded by the FCC’s recent digital-discrimination rules. Title II combined with digital discrimination imposes a double whammy of ex ante regulation of some conduct, combined with ex post monitoring, scrutiny, and enforcement of vast array of other conduct.[98]

Firms’ investment decisions are often likened to a pipeline. But a more appropriate analogy would be an assembly line, where investment opportunities are investigated and evaluated. Opportunities with negative returns on investment are rejected and those with positive returns are further evaluated and ranked. Because firms have limited resources, some of the investments with positive returns are rejected. Once a firm decides to pursue an investment opportunity, the project is further evaluated throughout the deployment timeframe. Just as a product can be pulled from the assembly line for defects, investments can be pulled for economic or technical defects. Generally speaking, the further down the assembly line the project goes, the less likely it is to be pulled. Thus, an interruption at the end of the assembly line is likely to be less disruptive than an interruption at the beginning.

In this sense, the Commission is correct to conclude that Title II classification would have relatively less impact on investments that are near the end of their assembly line. But that observation misses the much bigger picture of investments at the beginning of the assembly line and potential investments that are still in the investigation and evaluation stage. For these projects, Title II classification can turn projects with positive expected returns into projects with negative expected returns. In addition, the regulatory uncertainty that is endemic to Title II regulation reduces firms’ confidence in the reliability of their return-on-investment projections. Because of the well-known and widely accepted risk-return tradeoff, firms facing increased uncertainty in investment returns will demand higher expected returns from the investments they pursue.[99]

Put simply, Title II classification may not have a significant effect on investments near completion, but could have a statistically and economically significant impact on future and early-stage investments. Recently published peer-reviewed research supports this conclusion.

Wolfgang Briglauer and his co-authors examine the impact of net-neutrality regulations on broadband-network investment, specifically fiber-optic networks in OECD countries.[100] Roslyn Layton and Mark Jamison describe Briglauer, et al.’s research as “the only empirical, non-anecdotal analysis of net neutrality and investment to date.”[101] Using panel data from 2000 through 2021, Briglauer and his co-authors find evidence that net-neutrality regulations have a significant negative impact on fiber-optic network investment by internet service providers. They employ several econometric techniques, including fixed effects and instrumental variables models, to establish evidence of a causal relationship between net-neutrality rules and reduced investment. The main finding is that the introduction of net-neutrality regulations leads to an estimated 22-25% decrease in new fiber-optic network investments by ISPs.

Briglauer et al. argue their statistical analysis provides evidence that strict net-neutrality rules tend to slow deployment of new high-speed broadband connections. They find the negative impact manifests with a delay, rather than immediately, likely due to rigidities and lags in broadband-deployment projects, thus pointing to a long-run effect. In addition, their fiber investment variable measures newly installed fiber connections, representing new broadband-infrastructure capacity. This is more indicative of long-run capital investment rather than short-run variations in spending.

Briglauer et al. control for other factors unrelated to net-neutrality regulations by including macroeconomic conditions relevant for investment decisions, such as long-term interest rates and a measure of investment freedom. They also control for deployment costs, measured by population density and wages. In addition, their statistical model includes measures of cable competition, mobile competition, telecommunications services prices, and the number of broadband subscriptions. In many cases, these control variables have a statistically significant relationship with fiber investment. Nevertheless, even controlling for these other factors, the authors found that net-neutrality regulations were associated with decreased fiber-optic network investments by ISPs.

The Commission concludes that “changes in ISP investment following the adoption of each Order were more likely the result of other factors unrelated to the classification of BIAS, such as broader economic conditions.”[102] In this framing, it seems the Commission is arguing that if something contributes “more” (however “more” is measured) to investment than Title II classification, then the Commission should conclude that classification has no effect. But this is the wrong framing. Using statistical analysis, the effect of net-neutrality regulations on investment can be estimated while controlling for these other variables. The fact that other variables also affect investment does not invalidate a finding that net-neutrality regulations have some statistically and economically significant negative relationship with investment.

D. Title II Would Deter Future Innovation in Business Models

1. Paid prioritization is an essential component of many online business models

The Commission proposes to ban paid or affiliated prioritization arrangements, concluding such arrangements harm consumers, competition, and innovation, as well as creating disincentives to promote broadband deployment.”[103] Chair Rosensworcel has characterized paid prioritization as creating “fast lanes that favor those who can pay for access.”[104] This framing invites the question that was raised years ago, “Do fast lanes mean there are, by definition, slow lanes?”[105] The answer is “no,” as explained by Vox:

An ISP’s bandwidth is not fixed at current levels: As MVPDs shift to all-digital infrastructures, they have significant capacity to dedicate a larger portion of their “pipes” to broadband, which can meaningfully increase bandwidth available to consumers from today’s levels.

Think of bandwidth as a highway: If an entirely new lane is added at the ISP’s expense, that does not harm anyone riding along on the preexisting highway. We struggle to understand why enabling an “extra” HOV lane is bad policy that requires government regulation.

One should not simply assume that the creation of fast lanes of dedicated bandwidth forces everyone else who chooses not to pay ISPs, or cannot pay ISPs, into slow lanes. While those lanes may be slower than the fast lanes, they were slower with or without the fast lanes.

And if bandwidth-heavy traffic that would have traveled over the open Internet (adding to congestion) is offloaded onto a separate fast lane that does not impair the preexisting pipe’s bandwidth capabilities, it should actually ease congestion on the existing lanes, rather than create slow lanes.[106]

Prioritization is a longstanding and widespread practice and, as discussed at length in The Verge regarding Netflix’s Open Connect technology, the internet can’t work without some form of it:

When Open Connect originally launched a decade ago, the service started working collaboratively with ISPs on deployment. Netflix provides ISPs with the servers for free, and Netflix has an internal reliability team that works with ISP resources to maintain the servers. The benefit to ISPs, according to both Netflix and Akamai, is fewer costs to ISPs by alleviating the need for them to have to fetch copies of content themselves.[107]

Indeed, the Verge piece makes clear that even paid prioritization can be an essential tool for edge providers. As we’ve previously noted, paid prioritization offers an economically efficient means to distribute the costs of network optimization.[108]

Axel Gautier and Robert Somogyi developed a model that includes both paid prioritization and zero rating and conclude:

Prioritization is the preferred option of both the ISP and consumers under severe congestion and high-value content, because the low price charged by the ISP to consumers is counterbalanced by large payments from the [content providers].[109]

Banning paid prioritization forces all data to be treated equally, even if customers or services would benefit from differentiated offerings. Without flexibility in how services are delivered and priced, companies lose incentives to develop better networks and new innovations for specific use cases like high-bandwidth video streaming or remote medical services.

-

Throttling is an effective traffic-management tool

The Commission proposes to ban throttling lawful content, applications, services, and nonharmful devices.[110] While the Commission notes that throttling is “not outright blocking,” it also concludes such conduct “can have the same effects as outright blocking.”[111] The proposed ban would not ban throttling when it is “based on a choice clearly made by the end user,” such as a consumer’s choice of a plan in which a set amount of data is provided at one speed tier and any remaining data is provided at a lower tier.[112]

Internet bandwidth is a scarce and congestible resource subject to wild swings in consumer use. For example, Taylor Swift’s 2023 U.S. concerts have been associated with record-breaking levels of 5G data use on AT&T’s network.[113] Thus, allowing application-specific throttling gives companies incentives to streamline data demands. For mobile networks, excessive data usage impacts spectrum resources available to other customers. If networks cannot limit bandwidth-hungry apps during busy periods, then smartphone app developers lose incentives to tighten data usage. As internet-video traffic occupies about two-thirds of bandwidth, networks need some ability to manage congestion.[114] Outright throttling bans, rather than specific rules against anticompetitive discrimination, eliminate useful tools.

There is a dearth of empirical research regarding the throttling of application-service providers. In the only known published academic research, Daeho Lee and Junseok Hwang categorize application-service providers into four groups by bandwidth-usage attributes and latency sensitivity.[115] Using data from South Korea, they test the hypothesis that ISPs would be more likely to discriminate against content providers needing more bandwidth and more sensitive to latency. A regression of estimated technology-gap ratios on these variables, however, shows no significance, suggesting that ISPs do not discriminate against content providers based on bandwidth usage or latency. Using crowdsourced measurements across 2,735 ISPs in 183 countries and regions, Li et al. find that U.S. mobile providers seem to throttle content providers, but not to the extent in which consumers would likely notice.[116]

On the consumer side, recent research published in Telecommunications Policy finds no evidence that subscribers change their behavior in the face of throttled data rates.[117] Christoph Bauner and Augusto Espin analyze throughput levels measured for mobile ISPs in the United States with usage data to evaluate how sensitive users are to throttling. Using regression analysis of app usage on various measures of throttling, Bauner & Espin find no significant effect of data throughput on app usage. They argue that users may benefit from a modest degree of throttling when it aids network stability and reliability.[118] Bauner & Espin conclude their finding “seemingly weakens the … argument in favor of net neutrality rules.”[119]

In another consumer study, Hyun Ji Lee and Brian Whitacre found that low-income users were willing to pay for an extra GB of data each month, but were not willing to pay extra for a higher speed.[120] This is likely because, if a subscriber has a higher data limit, then they have a lower chance of being throttled for exceeding the cap. Lee & Whitacre’s results indicate Lifeline consumers are willing to pay for the option to use more unthrottled data, but are not willing to pay for higher speeds at all levels of data usage. This data-speed tradeoff suggests those consumers would benefit from a plan that offered a larger data allowance, but throttled speeds if the allowance is exceeded.

If, in fact, ISPs do not generally engage in throttling application-service providers and, when throttling does happen, consumers do not significantly change their usage in the face of throttling, then a ban on throttling is a solution in search of problem. In fact, it could be a solution that is worse than any perceived problem. A ban on data throttling removes essential network-management tools that could prevent congestion and improve overall customer experience. Moreover, discrimination against specific applications or competing services can already be scrutinized under existing antitrust and consumer-protection laws, as discussed in Part III.

-

Data caps and usage-based pricing can benefit both consumers and providers

In addition to the Commission’s proposed rules prohibiting throttling, the agency is also investigating data caps and usage-based pricing (UBP).[121] A 2021 survey reports that, during the pandemic, 37% of those surveyed hit their data cap, and 68% of those who exceeded their data-cap limit paid overage fees.[122]

Data caps and UBP are not a new issue. In 2013, an FCC advisory committee issued a report on data caps and UBP.[123] That report identified several ways in which the policies improve network performance, consumer experience, and investment and innovation among ISPs and edge providers:

- Data caps allow ISPs to employ various forms of price discrimination to recover the substantial fixed costs of building broadband networks. Without the ability to charge heavier users more through caps or usage-based pricing, ISPs lose flexibility in designing business models that align costs and willingness-to-pay. This could hamper their incentives and financial ability to continue investing in next-generation network upgrades.

- The ability to implement data caps or UBP provides incentive for internet application and edge service providers to develop more efficient ways of delivering data-intensive services. For example, data caps may “encourage edge providers to innovate more efficient means of delivering their services” by optimizing video compression algorithms and streamlining data transfers. Removing the possibility of caps or UBP eliminates a motivation for driving such innovation on the edge provider side.

- Prohibiting data caps or UBP would restrict future business-model experimentation between ISPs and consumers in response to evolving internet-usage patterns and demands. As technology enables new bandwidth-hungry apps and consumer behavior shifts, a strict ban on caps limits the pricing and service optionsthat ISPs can explore to sustainably meet that demand.[124]

While the NPRM is silent on data caps and UBP, the 2015 Order noted that data caps “may benefit consumers by offering them more choices over a greater range of service options,” but left open the possibility of future regulation:[125]

The record also reflects differing views over some broadband providers’ practices with respect to usage allowances (also called “data caps”). … Usage allowances may benefit consumers by offering them more choices over a greater range of service options, and, for mobile broadband networks, such plans are the industry norm today, in part reflecting the different capacity issues on mobile networks. Conversely, some commenters have expressed concern that such practices can potentially be used by broadband providers to disadvantage competing over-the-top providers. Given the unresolved debate concerning the benefits and drawbacks of data allowances and usage-based pricing plans, we decline to make blanket findings about these practices and will address concerns under the no-unreasonable interference/disadvantage on a case-by-case basis.[126]

Gus Hurwitz points out that data caps are a way of offering lower-priced services to lower-need users.[127] They are also a way of apportioning the cost of those networks in proportion to the intensity of a given user’s usage. He notes that, if all users faced the same prices regardless of their usage, there would be no marginal cost to incremental usage. Thus, users and content providers would have little incentive to consider their bandwidth usage. Network congestion does not go away by lifting data caps. Instead, it may be worsened, especially if there is no additional cost associated with additional usage.

As we note above, Lee & Whitacre found that low-income consumers were willing to pay for an extra GB of data each month, but were not willing to pay extra for a higher speed.[128] This indicates that even Lifeline subscribers have a positive willingness-to-pay for a greater data allowance.

Regardless of the effects of prohibiting data caps or UBP on consumers and providers, the more pernicious risk is the legal uncertainty of these practices under Title II regulation. Although the NPRM does not identify any specific proposals regarding data caps or UBP, there is a strong likelihood that these practices could be scrutinized or regulated under the overly broad proposed “conduct rules.” For example, Scott Jordan provides a thorough review of possible data-cap practices and which ones might fall afoul of the 2015 Order.[129] He concludes:

- Heavy-users caps on mobile-broadband service would likely satisfy the Order’s rules;

- Profit-maximizing caps on mobile-broadband service may or may not satisfy the rules; and

- Caps on fixed-broadband service are unlikely to satisfy the rules.

Jordan’s comprehensive survey demonstrates that many data-cap practices are in a gray zone of uncertainty regarding whether they would or would not satisfy the FCC’s conduct rules. This uncertainty would, by itself, likely stifle experimentation with innovative business models and practices, thereby hindering investment and diminishing users’ experiences.

III. Existing Policies Protect Consumers, National Security, and Public Safety

The Commission seeks comments on whether consumer-protection and antitrust laws provide sufficient protections against blocking, throttling, paid prioritization, and “other conduct that harms the open Internet.][130] In this section, we note that the United States has a multiplicity of agencies, laws, regulations, and rules that span competition, consumer-protection, and national-security issues. The Commission has provided little to no evidence that the existing regulatory regime has been deficient in enforcing existing policies or that new policies are needed—particularly outside of a congressional mandate.

A. Antitrust and Consumer Protection

Fundamental to the Commission’s position in the 2018 Order was the reasonable conclusion that ensuring ISPs do not interfere with consumers’ access to content over the internet would best be effected by adopting a competition and consumer-protection oriented approach. This is consistent with the Commission’s historical, deregulatory approach to information services, including in the 2015 Order. Since 2018, nothing has changed to disturb the soundness of this approach.

Core to the distinction in these approaches is an evaluation of the appropriate way to judge risk. The 2015 Order was premised on the theory that because ISPs have any incentive and ability to engage in problematic conduct, they thus will very likely engage in that conduct.[131] The Commission used this assumption to justify strong ex ante regulation to curtail such expected conduct. In the 2018 Order, rather than simply presuming harm, the Commission undertook an extensive, thorough, and fact-based analysis to first assess the likely risk of harm.[132] Based on this analysis, the Commission concluded that the risk of harmful conduct was low, in terms of both the likelihood that ISPs will engage in such conduct and its potential adverse effects on consumers. Because this risk is low, the Commission reasonably determined that a “light touch” ex post competition-oriented regulatory approach was preferable to the ex ante prescriptive rules adopted in the 2015 Order and under consideration in this NPRM.

We believe that the Commission had the better analysis in 2018 and should continue to support this approach. Indeed, in the long history of the net-neutrality debates, the justifications for imposing Title II obligations on ISPs have been rooted in the precautionary principle, with little or no actual evidence produced demonstrating any intentional violation of “neutrality” principles. And since 2018, no other evidence has been produced.

The ideal regulatory framework for dealing with potential violations of neutrality principles is an ex post regulatory approach that reflects well-established competition law principles and is commensurate with the actual degree of risk and extent of harm associated with ISP misconduct, while also mitigating against the risk that over-regulation that would harm consumers by curtailing pro-competitive ISP activity.

As the Commission observed in the 2018 Order, “[t]he Communications Act includes an antitrust savings clause, so the antitrust laws apply with equal vigor to entities regulated by the Commission.”[133] Thus, the Commission has already struck the proper balance between indirect antitrust enforcement and direct regulation under the Communications Act, which incorporates competition policy as the generally applicable regulatory “default” in the absence of specific statutory mandates. As Justice Breyer has observed, “[r]egulation is viewed as a substitute for competition, to be used only as a weapon of last resort—as a heroic cure reserved for a serious disease.”[134]

Of course, the Communications Act does not speak directly to “net neutrality” harms. But to the extent the act permits the Commission to regulate in this area, it does so largely by requiring the agency to choose between Title I and Title II classifications, reserving Title II for circumstances where the Commission determines that the risk of harm from providers is sufficiently great that ex ante, prescriptive regulation is appropriate—“as a heroic cure reserved for a serious disease.”[135]

Moreover, the Commission’s prior efforts to promote net neutrality overlap substantially, if not entirely, with concerns over ISPs engaging in anticompetitive conduct. In the 2018 Order, the Commission specifically noted that this was a necessary logical justification for its previous order, observing that: “The premise of Title II and other public utility regulation is that ISPs can exercise market power sufficient to substantially distort economic efficiency and harm end users.”[136]

In the 2015 Order, the Commission acknowledged that “[c]ommitment to robust competition and open networks defined Commission policy at the outset of the digital revolution,”[137] and that “[t]he principles of open access, competition, and consumer choice embodied in Carterfone and the Computer Inquires have continued to guide Commission policy in the Internet era[.]”[138] Likewise, the Commission explicitly acknowledged in the 2015 Order that its asserted authority under Section 706 was based, at least in part, on a mandate to promote competition.[139] Most tellingly, in a section titled “Competitive Effects,” the Commission noted that:

As the Commission has found previously, broadband providers have incentives to interfere with and disadvantage the operation of third-party Internet-based services that compete with the providers’ own services. Practices that have anti-competitive effects in the market for applications, services, content, or devices would likely unreasonably interfere with or unreasonably disadvantage edge providers’ ability to reach consumers in ways that would have a dampening effect on innovation, interrupting the virtuous cycle. As such, these anticompetitive practices are likely to harm consumers’ and edge providers’ ability to use broadband Internet access service to reach one another . . . .[140]

Thus, as the Commission itself acknowledged in the 2015 Order, competition—and, by implication, anticompetitive behavior of ISPs—is one of the core concerns that drove development of internet policy. Indeed, in the present NPRM, much of the feared harms mentioned are largely derived from vertical foreclosure theory. Namely, they stem from the classic antitrust concern that dominant firms in a vertical supply chain may foreclose competitors from access to consumers, or extract supracompetitive prices from input providers.[141] For example, the NPRM declares that:

[W]e also propose to reinstate rules that prohibit ISPs from blocking or throttling the information transmitted over their networks or engaging in paid or affiliated prioritization arrangements. Additionally, we propose to reinstate a general conduct standard that would prohibit practices that cause unreasonable interference or unreasonable disadvantage to consumers or edge providers.[142]

These instances of potential ISP misconduct raise straightforward antitrust concerns with vertical conduct, squarely within the purview of antitrust law.[143] Importantly, antitrust enforcers and courts—following antitrust economists—assess these vertical restraints under the rule of reason, avoiding their presumptive condemnation because they only rarely result in actual anticompetitive harm.[144]

Under this approach, the effects of potentially harmful conduct are typically evaluated and weighed against the various aims that competition law seeks to promote; only following that review is it determined whether particular conduct is harmful and, if so, whether there are procompetitive benefits that outweigh the harm.

In fact, only a few types of conduct are presumptively condemned, and then only when experience has demonstrated that they are more-often-than-not harmful.[145] Vertical restraints are never evaluated under this per se standard.[146] With such a competition framework for assessing conduct that might threaten “Internet openness,” the Commission would be well-positioned to detect and remedy harmful conduct.

B. The Transparency Rule Is Adequate for Consumer Protection

One of the longstanding policies available to protect consumers is the Commission’s transparency rule. The existing transparency rule, as upheld by the D.C. Circuit in Verizon v. FCC, mandates that broadband internet-access service providers disclose network-management practices, performance, and commercial terms.[147] This rule, applicable to both fixed and mobile providers, is integral for enabling consumers and edge providers to make informed choices. This rule has, in one form or another, been operational since 2010, and has served as a valuable consumer-protection measure.

The Commission is, however, considering extending this rule in a number of ways. It’s important to keep in mind that no policy extended indefinitely presents an unalloyed good: even transparency requirements, taken too far, can bring more costs than benefits.[148] For example, the proposed enhancements include more tailored disclosures to various stakeholders—including consumers, edge providers, and the FCC[149]—that, despite best intentions, may impose significant costs in the form of compliance burdens on ISPs, while doing little if anything to inform consumers meaningfully.

Additionally, a rule change that leads to the publication of information like pricing will functionally resemble a de facto tariff system. Tariffing, however, is a core component of common carriage.[150] Thus, if the Commission opts not to reclassify under Title II, imposition of such a de facto tariff could be a violation of Section 706. Moreover, regulatory pressure to report pricing in uniform ways could lead to uniform pricing, which, though benign-sounding, could lead to downstream changes in service level and pricing that do not ultimately increase consumer welfare.

For example, although at times difficult to follow, internet-service pricing that is designed around discounts and incentives could be used to benefit economically vulnerable consumers and attract or retain them through a form of price discrimination. If, however, rates converge on a uniform schedule, it is possible that these forms of discounts and incentives will disappear, and that pricing will reflect a mean that is more difficult for lower-income consumers. This possibility has increased substantially with the FCC’s recently adopted digital-discrimination rules, which explicitly subject pricing, discounts, incentives and other terms and conditions to scrutiny and enforcement under the rules.[151] Thus, even in the absence of Title II regulation, the proposed reporting requirements can work hand-in-hand with the digital-discrimination rules to regulate rates in the direction of uniform pricing across providers, thereby limiting the scope of competition for broadband services.

Further, the utility of certain disclosures, such as those related to network congestion, is also questionable. The Commission opted to forego requiring disclosures related to network performance in the 2015 Order.[152] The Commission should continue in this manner, as such requirements are even less useful today than they were in 2015. With the availability of speed-test applications, consumers already possess tools to assess the performance of their ISP, casting doubt on the additional value of mandatory congestion disclosures.

IV. Title II Reclassification Will Present Significant Legal Challenges for the Commission