The Credit Card Competition Act’s Potential Effects on Airline Co-Branded Cards, Airlines, and Consumers

Executive Summary

This study assesses the likely consequences of implementing the Credit Card Competition Act (CCCA), which proposes to require issuers of most Visa and Mastercard branded credit cards in the United States to include a second network on their cards, and to allow merchants to route transactions on a network other than the primary network branded on the card.

Proponents of the Credit Card Competition Act (CCCA) claim that it would “enhance credit card competition and choice in order to reduce excessive credit card fees.” In fact, by forcing most U.S. credit-card issuers to include a second network on all their cards, the CCCA would remove the choice of network from the issuer and cardholder, and place it in the hands of the merchant and the acquiring bank.

There is some uncertainty as to the legislation’s anticipated effects, as nothing quite like it has ever been implemented anywhere in the world. We can, however, make some inferences based on the known effects of prior regulations driven by similar motives, in the United States and in such jurisdictions as Europe and Australia.

The primary U.S. payment-card networks—Visa, Mastercard, American Express, and Discover—constantly vie with one another to attract customers, investing billions of dollars in innovations that improve the user experience and reduce fraud and theft.

At the same time, hundreds of banks and credit unions compete to offer a broad range of credit cards to American consumers, choosing the network for each card based on the fit between the network’s terms, the card’s purposes, and its intended market.

Credit cards offer numerous benefits, including access to credit (interest-free, if paid in full by the due date), fraud protection, and chargebacks. Many also offer purchase insurance, fee-free international transactions, and consumer rewards like loyalty points and cash back.

Many rewards cards are co-branded with partners such as airlines, hotels, and retailers. The relationship between partners and card issuers is highly synergistic, with issuers generating revenue—due to increased use and associated interchange fees—while partners receive payments for rewards, marketing, and other ancillary benefits (such as lounge access, in the case of airlines). For the top six U.S. airlines alone, these deals represent more than 5% of total revenue—and five times their net revenue.

Credit-card rewards, including cash back and travel points, have become an important part of many consumers’ budgeting decisions. Indeed, it is not uncommon for consumers to have two or three different rewards credit cards, enabling them to choose which to use at time of a purchase based, at least in part, on the rewards they receive from any particular card.

While the CCCA would likely reduce the interchange fees paid by acquiring banks to issuing banks, overall bank fees are unlikely to fall dramatically. Rather, banks would shift fees from interchange to other sources of revenue, including late fees and interest.

The reduction in interchange fees would almost certainly significantly reduce rewards and other benefits to cardholders, as happened when price controls were imposed on debit cards following the implementation of a provision of the Dodd–Frank Wall Street Reform and Consumer Protection Act of 2010 known as the “Durbin amendment,” after sponsoring Sen. Richard Durbin (D-Ill.), who is also lead sponsor of the CCCA. The reduction in interchange fees, in turn, would make certain types of cards less viable. As such, the CCCA would reduce choice for consumers.

Exempted card issuers—especially those of the large three-party networks, American Express and Discover—would likely benefit from the CCCA, as they would still be able to offer rewards and the security of their networks would not be affected.

Merchants who partner with exempted three-party card issuers also would almost certainly benefit, at the expense of other merchants whose co-branded cards are issued by banks that are covered by the legislation. For example, Delta Airlines, which has a card co-branded with American Express, would benefit at the expense of all other airlines. Merchants that co-brand with a three-party card would not only benefit from higher merchant fees, but also from customers switching to receive higher levels of loyalty rewards. Moreover, those who currently spend the most on their co-branded cards would likely be most motivated to switch.

Given the relatively low margins of the U.S. airline industry and the significant proportion of revenue that loyalty rewards represent, the combination of reduced loyalty revenue and reduced customer revenue could be absolutely devastating for the industry (except, as noted, for Delta).

To make matters worse, the CCCA may also affect many airlines’ costs of capital. For example, a reduction in expected revenue from the sale of rewards could result in credit rating agencies downgrading the bonds that United and American Airlines’ rewards-program subsidiaries issued during the COVID-19 pandemic. That could trigger covenants requiring the parent companies to post additional capital, which would, in turn, increase the parents’ capital costs.

In general, the combination of reduced revenue and reduced loyalty-program memberships—leading to lower revenue from higher-value customers—would reduce airlines’ expected future profitability, which would increase capital costs. This may not pose a problem in periods when demand for air travel is high. In a downturn, however, it could result in a bankruptcy—previously avoided due to the airline’s ability to securitize its loyalty program.

One potential outcome is that bank issuers and airlines choose to cancel their co-branded agreements by mutual consent, so that the airlines could make similar arrangements solely with three-party card networks. While this would clearly be beneficial for those three-party networks, and could mitigate the harm to the airlines, it would be enormously costly, and the losers would be issuers, four-party networks, cardholders (especially those with lower credit scores who did not qualify for the three-party-network cards), and the U.S. economy as a whole.

It is also possible that issuers will do what they appear to have done in the EU: increase interest rates and late fees so that they can continue to offer some level of rewards. In that case, the CCCA would have brought about what some critics of credit-card rewards have previously falsely accused issuers of doing: using credit cards to transfer wealth from lower-income, lower-spending consumers who maintain a revolving balance to higher-income, higher-spending consumers who pay off their balances every month.

Either way, the CCCA effectively picks winners and losers. The winners will be three-party cards—especially American Express—and merchants that co-brand with those cards, such as Delta (and their customers), as well as big-box retailers. The losers will be Visa, Mastercard, the other airlines, the card issuers, and their customers. Overall, merchants are also likely to lose, as consumers spend less, which could translate into lower rates of economic growth. Unfortunately, the number and scale of those who lose is likely to be far greater than the number and scale of those who win.

I. Introduction

Over the past 20 years, payment cards have become increasingly vital to the U.S. economy, largely replacing checks as the preferred means of making a whole range of payments. Underpinning this shift have been innovations in payments technologies that have made them quicker, more convenient, more secure, and less costly for both consumers and merchants.1F[1] These innovations have been driven by competition:

- The primary U.S. payment-card networks—Visa, Mastercard, American Express and Discover—constantly vie with one another to attract and retain customers, investing billions of dollars in innovations that improve the user experience and reduce fraud.

- At the same time, hundreds of banks and credit unions compete to offer a wide range of credit cards to American consumers. Those issuers choose the four-party network for each card, based on the fit between the network’s terms, the card’s purposes, and its intended market.

- Meanwhile, the two major three-party networks—American Express and Discover—compete both with each another and with the large issuers and the four-party networks over which they operate.

A. Counterparty, Default, and Collection Risk

Credit-card issuers guarantee payment to merchants, so long as those merchants comply with the terms and conditions set by the card network.[2] In so doing, credit cards provide a means of payment that has lower counterparty risk for the merchant than checks. At the same time, card issuers effectively assume the risk of default and collection.

Back in 2010, Sen. Richard Durbin (D-Ill.) himself recognized that operating credit cards is an expensive enterprise that entails counterparty, default, and collection risk, which is why credit cards were excluded from the original Durbin amendment. As he noted at the time:

About half of the transactions that take place now using plastic are with credit cards, and there is a fee charged—usually 1 or 2 percent of the actual amount that is charged to the credit card. It is understandable because the credit card company is creating this means of payment. It is also running the risk of default and collection, where someone does not pay off their credit card. So, the fee is understandable because there is risk associated with it.[3]

B. Understanding Interchange Fees

For early card-payment systems, offering a means of payment and being exposed to counterparty, collection, and default risk were pretty much the core features of the product. This is because there were only two parties: the merchant and the consumer. The “card” (a metal plate) enabled merchants to maintain a record of credit provided to regular customers, who would then settle up at the end of the month.3F[4]

So, had Sen. Durbin been referring to the Charge Plate—or to its modern equivalent, which are merchant-issued charge cards—his characterization of the costs would have been largely correct. But nearly all modern payment networks are either three- or four-party systems that are fundamentally more complex.

1. Three- and four-party cards

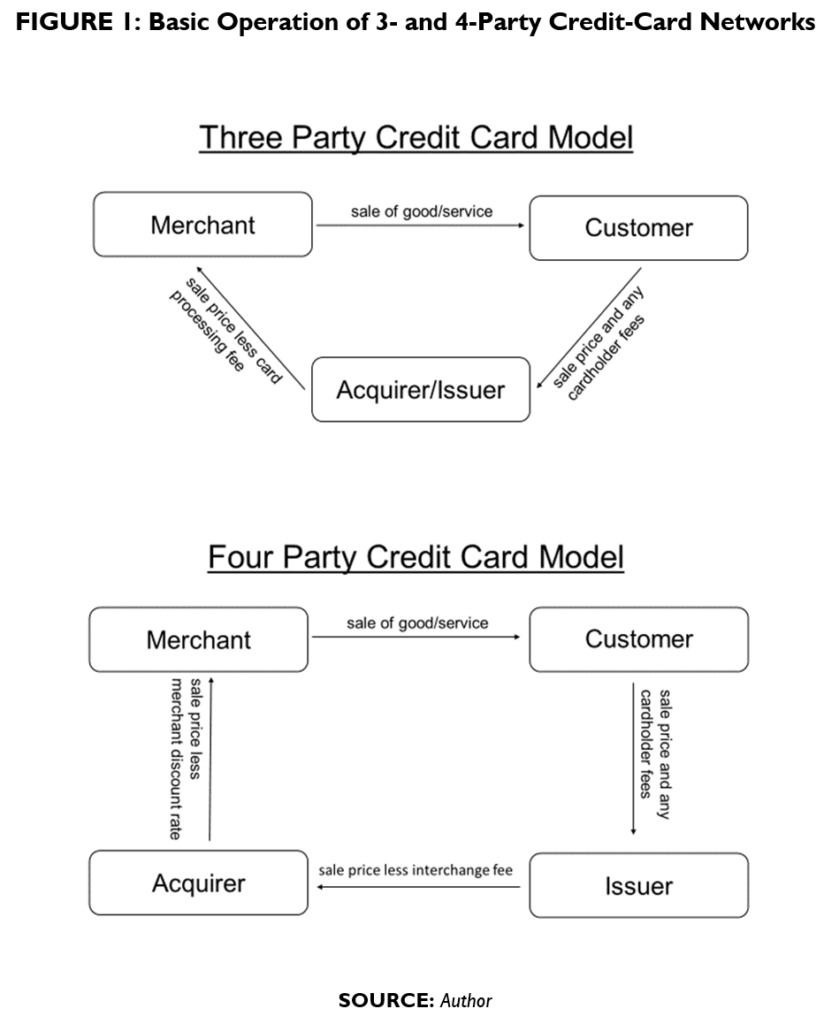

In the 1950s, Diners Club and then American Express both established “three-party” systems, which enabled consumers to use the same card at multiple merchants.4F[5] In a three-party system, the card issuer pays merchants directly, and bills and collects from cardholders directly.5F[6]

The following decade, several organizations developed “four-party” systems, which have four main parties: issuer, consumer, merchant, and acquirer. The issuer contracts with the consumer, providing the card, issuing bills, etc. The acquirer contracts with the merchant, making payment. The rules of the system are set by the network operator, which also facilitates settlement between the issuer and the acquirer, and monitors for fraud and other abuse.6F[7] Visa and Mastercard are the primary global four-party networks.

2. Two-sided markets

One of the major challenges faced by both three- and four-party payment systems is to persuade both merchants and consumers of their value. If too few merchants accept a particular form of payment, consumers will have little reason to hold it and issuers will have little incentive to issue it. Likewise, if too few consumers hold a card, merchants will have little reason to accept it.

Conceptually, economists describe such scenarios as “two-sided markets”: consumers are on one side, merchants on the other, and the payment system acts as the platform that facilitates interactions between them.7F[8] While payment cards are a prominent example of a two-sided market, there are many others, including newspapers, shopping malls, social-networking sites, and search engines. Indeed, the rise of the internet has made two-sided markets practically ubiquitous.

All platform operators that facilitate two-sided markets face essentially the same challenge: how to create incentives for participation on each side of the market to maximize the joint net benefits of the platform to all participants—and to allocate costs accordingly.8F[9] Thus, the platform operator can be expected to set the respective prices charged to participants on each side of the market to achieve this maximand.9F[10] If the operator sets the price too high for some consumers, they will be unwilling to use the platform; similarly, if the operator sets the price too high for some merchants, they will not be willing to use the platform. As the U.S. Supreme Court put it:

To optimize sales, the network must find the balance of pricing that encourages the greatest number of matches between cardholders and merchants.[11]

3. Transaction fees

This brings us to transaction fees, which are the primary mechanism that credit-card-network operators use to balance the market. In three-party systems (American Express and Discover), the card-network operator acts as both issuer and acquirer, and charges merchants a card-processing fee (typically a percentage of the transaction amount) directly. In four-party systems, the issuer charges the acquirer an “interchange fee” (set by the networks) that is then incorporated into the fees those acquirers charge to merchants (called a “merchant-discount rate” in the United States). The schematics in Figure 3 show how these different systems operate.

The interchange fees charged on four-party cards vary by location, type of merchant, type and size of transaction, and type of card. An important factor determining the size of interchange fee charged to a particular card is the extent of benefits associated with the card—and, in particular, any rewards that accrue to the cardholder.

The various three- and four-party payment networks have been engaged in a decades-long process of dynamic competition, in which each has sought—and continues to seek—to discover how to maximize value to their networks of merchants and consumers. This has involved considerable investment in innovative products, including more effective ways to encourage participation, as well as the identification and prevention of fraud and theft.[12]

It has also involved experimentation with differing levels of transaction fees. The early three-party schemes charged a transaction fee of as much as 7%.15F[13] Competition and innovation (including, especially, innovation in measures to reduce delinquency, fraud, and theft) drove those rates down. For U.S. credit cards, interchange fees range from about 1.4% to 3.5%, while the average is approximately 2.2%.18F[14]

In general, economists have concluded that the “optimal” interchange fee is elusive, and that the closest proxy is to be found through unforced market competition. They have therefore cautioned against intervention without sufficient evidence of a significant market failure.25F[15]

C. Regulation: In Whose Interests?

Despite these cautions, governments have intervened in the operation of payment systems in various ways. As we have documented previously, many of these regulations have slowed the shift toward more innovative, quicker, and more convenient payment systems, while also reducing other benefits and harming, in particular, poorer consumers and smaller merchants.2F[16]

Introduced in June 2023 by Sens. Richard Durbin (D-Ill.), Roger Marshall (R-Kan.), Peter Welch (D-Vt.), and J.D. Vance (R-Ohio), the Credit Card Competition Act of 2023[17] would continue this trend, to the detriment of consumers and businesses. As this paper documents, co-branded cards generate significant revenue for the merchants whose brand appears on the card. As Section II documents, this appears to be particularly true for airlines. While many other merchants also have valuable co-branded agreements, they generally represent a much lower proportion of total revenue. Hence, assessing the potential effect of the CCCA on airline co-branded credit cards—and on the airlines themselves—is particularly important.

As documented in Section IV, there are broadly two potential outcomes of the CCCA with respect of U.S. airlines:

- Businesses could implement workarounds that minimize the law’s effects. These workarounds are not costless; among other things, they would entail rewriting hundreds of millions of contracts. Issuers, merchants, and consumers would bear those costs. There would also be a significant redistribution of revenue and profits away from the largest four-party card issuers and payment networks and toward the two major three-party networks—perhaps especially American Express. And there would be a smaller redistribution of revenue and profits away from the larger airlines that currently have co-branded cards with Visa and Mastercard (especially American, United, Southwest, Alaska, and JetBlue) toward Delta, which is the one major domestic airline that has a co-branded card with American Express.

- If businesses are unable to implement adequate workarounds, the act’s effects could be much more severe. Most significantly, with the exception of Delta, the major airlines could potentially lose billions of dollars in revenue, mainly because of the reduction in revenue from co-branded cards, but also because some proportion of flyers would likely switch to Delta to take advantage of the more attractive benefits on Delta’s existing co-branded credit card. This, in turn, would affect airlines’ ability to operate some marginal routes, perhaps leading to a spiral of defections to Delta, which would become a huge beneficiary, as it would be relatively more profitable and attract additional fliers.

While the second outcome would clearly be worse, in both cases, Americans would have choices taken away, costs would increase, and economic growth would be adversely affected. Moreover, far from reducing merchants’ costs, most merchants would be adversely affected, as the costs of acquiring credit cards would not fall and could, indeed, rise (and, of course, merchants with co-branded loyalty-rewards cards would suffer substantial revenue losses). In short, there is basically no scenario in which the Credit Card Competition Act is actually good for competition, American consumers, or the U.S. economy as a whole.

D. Overview of the Study

The study proceeds as follows:

- Section II discusses the nature and economics of loyalty-rewards programs, with a particular focus on airline-rewards programs. It then explains co-branded credit cards and describes some of the major airline co-branded credit-card partnerships, including their likely revenue.

- Section III provides a brief overview of the CCCA.

- Section IV considers some of the primary examples of interchange-fee price controls and routing regulations that have been implemented in the United States and other jurisdictions.

- Section v considers, in detail, the potential effects of the CCCA. It discusses various implementation scenarios and the likely effects of these scenarios on the rewards received by holders of airline co-branded cards, on the behavior of those cardholders, and on the airlines themselves.

- Section VI offers some concluding remarks.

II. Airline Loyalty-Rewards Programs and Co-Branded Credit Cards

Loyalty-rewards programs have existed for hundreds of years. The first documented program in the United States was established in 1793 by a merchant in Sudbury, New Hampshire, who gave away copper tokens to customers, which could be redeemed for goods.[18] Over time, programs became more sophisticated, with copper tokens replaced, first, by stamps and, later on, by plastic cards with magnetic stripes that encoded the owner’s account information (reward information being recorded on a central database that could be accessed using the card, enabling rewards to be deposited or used). These days, rewards are mostly held in online accounts and accessed via websites and mobile apps, although cards are often still distributed—albeit mainly symbolically.

While we are mainly concerned here with airlines loyalty-rewards programs, and specifically with the role of credit cards co-branded by those programs, it helps to have a more general appreciation of the nature and function of loyalty-rewards programs. Toward that end, this section begins with a basic explanation of the economics of loyalty-rewards programs. It then explores the nature and function of credit-card reward programs, before discussing airline/credit-card co-branded reward programs in more detail.

A. The Economics of Loyalty-Rewards Programs

Loyalty-rewards programs function primarily as marketing tools to encourage customers to become and remain loyal to a particular merchant. Program participants typically receive points toward rewards each time they make a purchase associated with the program, creating incentives to buy goods and services from that merchant.

These incentives are enhanced by structuring the programs in tiers and making them time-limited, so that participants who purchase more goods or services in a particular period receive higher levels of rewards. Such features are prominent in airline-reward programs, which typically offer inducements to participants in the form of upgrades, waived baggage fees, and use of airport lounges, which become available upon spending a certain amount over the course of a year.[19]

Loyalty-reward programs that distribute specific goods or services in return for reward points, coupons, or stamps likely benefit from the ability to purchase goods or services at a bulk discount.[20]

Merchants may also use rewards redemptions as a means to practice price discrimination, offering specific goods and services to reward-program participants for reduced reward redemptions. For example, airlines typically offer seats for fewer reward points during off-peak periods. Such discounts reduce the marginal cost of the rewards program, enabling merchants to make use of otherwise-unfilled capacity or to sell bulk-purchased goods, while simultaneously providing additional benefits to loyal customers.

Card-based and digital (i.e., app-based or online) reward programs also collect data on the purchasing habits of program participants. As a result, program operators and partners can target marketing at specific participants and more effectively build longer-term customer relationships with them.

B. Airline-Rewards Programs

American Airlines established the first airline loyalty-rewards program, AAdvantage, in 1981.[21] The other major carriers soon followed suit, realizing that such programs can be an effective means to offer incentives for loyalty. The standard loyalty-rewards program was boosted in 1982 when American Airlines introduced a “gold” tier for higher-value customers.[22] Again, other airlines followed suit, and most have since developed multiple tiers. The evidence shows that airline loyalty-reward schemes are highly effective ways to attract and retain high-value customers.[23]

The value of airline loyalty-reward programs was demonstrated in an unusual way during the COVID-19 pandemic. The collapse in demand for air travel caused more than 40 airlines around the world to file for bankruptcy.[24] Initially, some U.S. carriers issued bonds with very high coupons, as they hemorrhaged cash.[25] Then, in June 2020, United Airlines created a separate bankruptcy-remote entity for its rewards programs, and used it as collateral to issue $5 billion in bonds at a more favorable rate than the airline itself would have received.[26] American and Delta took the same approach.[27]

C. Credit-Card Reward Programs

Credit-card rewards programs are similar in many elements of their basic operation to other reward programs. Card users receive rewards either in the form of cashback or points (or “miles”) that can be redeemed for various goods and services (the specific goods and services available vary, depending on nature of the rewards-program operator and any partners or affiliates).

Many card issuers offer credit cards that are co-branded with merchants, ranging from retailers to hotels. Among the most popular cards are those co-branded with airlines. Before delving into the particulars of airline co-branded cards, however, it is worth briefly considering the mechanics of co-branded cards in general.

Each co-branded card offering exists by way of an agreement between the card issuer and the co-brand entity. This agreement typically specifies the amount the card issuer will pay the co-brand entity for the purchase of loyalty-reward points, as well as marketing opportunities. These agreements enable issuers, in turn, to make further agreements with cardholders, offering them specific rewards in return for specific spending amounts.

By offering rewards, card issuers provide card holders with incentives to use their card. Meanwhile, the rewards themselves also create loyalty toward the co-brand entity. And the co-brand entity is typically able to adjust the redemption rate of loyalty rewards in order to encourage the use of rewards in ways that reduce the marginal cost of the rewards redemption to the co-brand entity. That, in turn, enables the co-brand entity to offer rewards to card issuers at a discount. In this way, rewards programs can generate significant profits for co-brand entities and issuers, while generating loyalty to the brand and the card for cardholders.

Credit-card-based reward programs can be a highly effective way both to increase the use of cards and to enhance customer loyalty. Survey data demonstrate the effectiveness of rewards programs as a means of encouraging loyalty. A 2015 survey by Technology Advice of U.S. shoppers found that more than 80% of respondents said they were more likely to shop at stores that offered loyalty programs.[28]

Credit-card issuers, in turn, fund the programs partly by charging annual fees to users and partly by charging interchange fees to merchants.

Merchants undoubtedly benefit from credit-card-reward programs both directly and indirectly. Direct benefits come from the ability to target marketing to reward-program members through discounts, additional rewards, and other inducements. As noted, card-based rewards programs enable merchants to customize marketing to specific individuals and groups based on information gathered through card use about their purchasing habits. This can result in a substantial increase in spending per-transaction (known as “ticket lift”).

Research by Mastercard, for example, found that international travelers to the United States who were offered incentives to shop at certain merchants spent four times as much on their cards as cardholders not redeeming such offers.[29] Indirect benefits come from increased use of credit cards in general, which leads to increased spending, due to reduced liquidity constraints, as well as reduced transaction costs and better transaction management.

Credit-card issuers also benefit from credit-card rewards programs, through additional card uptake and usage, as well as from fees charged to merchants and third-party reward-card operators for transaction-related information that better enables them to target marketing efforts.[30]

Arguably the greatest beneficiaries of reward programs, however, are consumers with reward credit cards. Such consumers benefit directly, both from the rewards themselves and from the various additional inducements offered by merchants and card issuers as part of marketing efforts. A survey by Ipsos conducted at the end of 2020 found that 60% of Americans consider credit-card rewards to be “very important” for them, while over half said the prospect of rewards influences their purchasing decisions.[31] Meanwhile, a more recent survey by WalletHub found that 80% of respondents said that inflation had made them more interested in credit-card rewards.[32]

Moreover, due to the better targeting of these inducements made possible by the use of individual transaction data, owners of rewards credit cards likely receive offers that are more relevant than poorly differentiated mass marketing and advertising. In the WalletHub survey, 58% of Americans said they go out of their way to spend at merchants who offer additional credit-card rewards.[33]

D. Airline/Credit-Card Co-Branded Reward-Program Partnerships

Many merchants with loyalty-rewards programs partner with affiliated (non-competing) merchants to expand their program’s reach. Airlines notably partner with providers of related travel services, such as hotels and car-rental services, offering additional loyalty-rewards points in return for spending dollars at those partners. The partners in these programs purchase the loyalty-rewards points from the airlines, thereby generating additional revenue for the airline.

1. The value of airline loyalty-reward programs

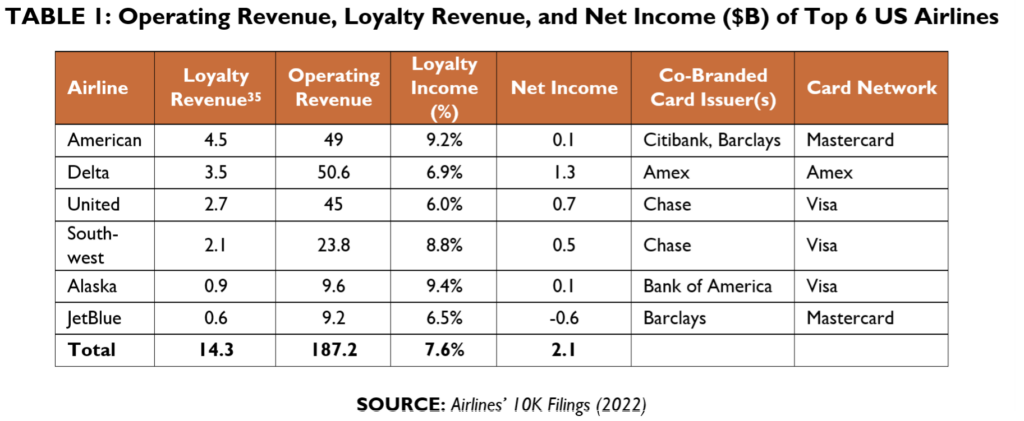

In 2022, loyalty-rewards programs represented 7.6% of total revenue for the top six U.S. domestic airlines (“loyalty income” column in Table 1). Given the airlines’ relatively thin profit margins (“net income” column in Table 1), this revenue is clearly important even in good times. Indeed, in 2019, the net cash income of the loyalty-rewards programs for the three largest U.S. airlines was $7.8 billion and the margin on those programs ranged from 39% to 53%.[34]

But loyalty-rewards income can be even more important during downturns. During the 2009-2010 recession, both American Airlines and Delta reported pre-selling $1 billion of loyalty rewards to their co-branded credit-card issuers (Citibank and American Express, respectively).[36] And during the COVID-19 pandemic, the airlines were essentially kept afloat by their loyalty-rewards programs, in general, and their co-branded cards, in particular.

In 2020, for example, American Airlines sold $3.65 billion of loyalty rewards, of which $2.9 billion came from sales to co-branded cards and other partners, resulting in adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) for the loyalty-rewards program of $2.1 billion.[37] It is noteworthy that those partner-rewards sales were only 25% lower in 2020 than in 2019, suggesting that co-branded cards were responsible for about 70% of the total.[38] Meanwhile, Delta, United, and American raised more than $10 billion by issuing debt backed by their loyalty programs, enabling them to avoid bankruptcy.[39]

2. The value of credit-card co-branded partnerships

For airlines, the most significant loyalty-reward partnership is with credit-card issuers.[40] While the airlines do not usually break out the numbers specifically for co-branded cards, they are clear in their annual reports about the importance of their partnerships with credit-card issuers. Consider the following four examples:

- American Airlines’ 2022 annual report noted that: “During 2022 and 2021, cash payments from co-branded credit card and other partners were $4.5 billion and $3.4 billion, respectively.”[41]

- United Airlines’ 2022 annual report noted that: “Other operating revenue increased $664 million, or 31.8% [to 2.75 billion], in 2022 as compared to 2021, primarily due to an increase in mileage revenue from non-airline partners, including credit card spending recovery with our co-branded credit card partner….”[42]

- Delta Airlines’ annual report noted that revenues from its loyalty program “are mainly driven by customer spend on American Express cards and new cardholder acquisitions.” Meanwhile, the company’s accounting of “miscellaneous income” was “primarily composed of lounge access, including access provided to certain American Express cardholders, and codeshare revenues.” In 2022, income from the loyalty program was $2.58 billion, while miscellaneous revenue was $894 million.[43] In total, the two revenue streams represented $3.47 billion.

- In 2022, Southwest declared $3.03 billion in “passenger loyalty” related revenue.[44] As the company’s annual report explained: “Passenger loyalty – air transportation primarily consists of the revenue associated with award flights taken by loyalty program members upon redemption of loyalty points.” Southwest accounts for loyalty points on an accrual basis as a liability, which becomes “revenue” when they are spent. Southwest separately accounts for “other revenues” which “primarily consist of marketing royalties associated with the Company’s co-brand Chase® Visa credit card, but also include commissions and advertising associated with Southwest.com ®.”[45] It notes: “The Company recognized revenue related to the marketing, advertising, and other travel-related benefits of the revenue associated with various loyalty partner agreements including, but not limited to, the Agreement with Chase, within Other operating revenues. For the years ended December 31, 2022, 2021, and 2020 the Company recognized $2.1 billion, $1.4 billion, and $1.1 billion, respectively.”[46]

As these descriptions indicate, revenues to airlines from co-branded cards are a combination of loyalty rewards, which issuers purchase from the airlines and then allocate to cardholders in accordance with the terms of agreements between the issuers and cardholders; payments for marketing, which includes such items as sending promotional materials to the airlines’ lists of loyalty-rewards members; and payments for ancillary benefits, such as lounge access for some cardholders.

Previous estimates indicate that the proportion of “loyalty revenue” attributable to co-branded credit cards is in the 70% to 80% range.[47] At the lower end of that range (70%), the top six airline co-branded cards would have generated just over $10 billion in value in 2022. Plausibly, the number is somewhat higher. As such, revenue from co-branded cards would represent at least 5% of the operating revenue of the six largest airlines and five times those airlines’ net revenue.

Per the discussion above about the beneficiaries of co-branded reward programs, it seems reasonable to infer that airline co-branded reward cards are highly valued by consumers, airlines, the partners, and the card issuers.

III. The Credit Card Competition Act

The Credit Card Competition Act of 2023 (CCCA) was introduced in the U.S. Senate on June 7, 2023, by Sens. Richard Durbin (D-Ill.), Roger Marshall (R-Kan.), Peter Welch (D-Vt.), and J.D. Vance (R-Ohio). If enacted, the bill would direct the Federal Reserve Board to promulgate regulations to prohibit banks with assets of $100 billion or more from issuing credit cards[48] that could be used with either (1) only one payment network, (2) only two affiliated payment networks,[49] or (3) only the two payment networks with the “largest market share.”[50] The bill also directs the Federal Reserve Board to promulgate rules prohibiting credit-card processors from limiting merchants’ ability to choose which network they use to route a payment.[51] Furthermore, it would effectively require interoperability of credit-card “tokens.”

While the bill does not explicitly name Visa or Mastercard, they are clearly its primary target. The legislation defines “largest market share” by number of cards issued, which is far larger for both Visa and Mastercard than for any three-party network (i.e., American Express and Discover), primarily because of the intense competition among banks to supply cards.[52] In addition, the Federal Reserve Board would be required to review market share every three years and, if the identities of two largest networks have changed, then the third requirement would no longer apply.[53] As if that weren’t clear enough, the legislation also states that “The regulations … shall not apply to a credit card issued in a 3-party payment system model.”[54]

A. Prima Facie, Would the CCCA Achieve Its Aims?

In his summary of the act, Sen. Durbin claims:

[T]he giant banks that issue the overwhelming majority of Visa and Mastercard credit cards would have to choose a second competitive network to go on each card, and then a merchant would get to choose which of those networks to use to process a transaction. This competition and choice between networks would incentivize better service and lower cost; in fact, for more than a decade, federal law has required debit cards to carry at least two debit networks and this requirement of a choice of debit networks has fostered increased competition and innovation in the debit network market and has helped hold down fees.

That is, to say the least, an optimistic appraisal of the proposed legislation. While it is highly plausible that the CCCA would, if enacted, lead to a reduction in interchange fees, it appears highly unlikely that it offers incentives for better service. Indeed, the opposite is far more likely. The reason is asymmetric counterparty risk and, specifically, the lack of adequate incentives on the part of larger merchants and acquirers to choose networks that manage fraud risk. This is a problem that Todd Zywicki and I discuss at length in our recent paper on the regulation of routing in payment networks.[55] As we note there:

[E]ach party to a transaction has somewhat different incentives regarding the choice of network. In general, the card issuer and cardholder both have strong incentives to route payments over the main branded network associated with the card, thereby ensuring the use of all the security and anti-fraud protections available from an EMV card, including 3DS for online transactions and the ability for cardholders to place temporary holds on their cards. Some merchants also have incentives to route over the main branded network, especially smaller merchants selling higher-value goods online, given the potential for very expensive chargebacks from unauthorized transactions. However, many other merchants, especially larger high-volume merchants, would have incentives to use the lowest cost routing, especially those that are able to take advantage of the EMV chip and PIN for POS transactions, and those that have their own machine-learning-based fraud monitoring systems that enable them to reduce potential chargebacks on their own. Finally, acquirers generally have less incentive to avoid fraud and stronger incentives to route transactions over the least-cost route.

Since the CCCA would shift the choice of network from the issuer to the merchant and/or acquirer, and since those parties generally have weaker incentives to route transactions over more secure networks with better fraud detection, the likeliest effect is that the CCCA would reduce investments in fraud prevention. As we also noted in the paper on regulating routing, mandating “competition” over routing would cause data fragmentation, with some transactions being routed over the primary network while others are routed over the secondary network. The end result is that the networks’ fraud-detection algorithms would be less effective.[56] Thus, at least when it comes to fraud prevention, the CCCA would likely result in worse service, not better.

B. The Effect of the CCCA on Airline Co-Branded Rewards Cards

As noted, for reasons explained in Section II, this paper is primarily interested in the effect of the CCCA on airline co-branded rewards cards. Subsequent sections draw on evidence regarding the effects of other interchange-fee regulations, both in the United States and around the world. As a prelude, here is what American Airlines said in its 2022 annual report about the legislation’s potential implications (referring to a near-identical bill that was introduced in the 117th Congress):

We may also be impacted by competition regulations affecting certain of our major commercial partners, including our co-branded credit card partners. For example, there has previously been bipartisan legislation proposed in Congress called the Credit Card Competition Act designed to increase credit card transaction routing options for merchants which, if enacted, could result in a reduction of the fees levied on credit card transactions. If this legislation were successful, it could fundamentally alter the profitability of our agreements with co-branded credit card partners and the benefits we provide to our consumers through the co-branded credit cards issued by these partners.[57]

IV. Lessons from Other Interchange Regulations

Over the past four decades, jurisdictions across the world have imposed a range of regulations on payment cards.[58] The most common of these have been price controls on interchange fees. Because three-party card networks are closed loop, there is technically no “interchange” fee and, in many but not all cases, regulations have been interpreted as not applying to them.[59] Some jurisdictions have also imposed other regulations, of which the most relevant for the current analysis is the Durbin amendment’s routing requirements. This section discusses evidence of the effects of these two types of regulation in order to provide insights into what might be expected from the CCCA. (For additional details, see our recent literature review.[60])

A. Price Controls

In every jurisdiction that has introduced price controls on interchange fees, issuing banks have responded by adjusting their offerings. In the case of credit cards, this has typically meant some combination of reduced card benefits (rewards, insurance, and so on); increased annual fees; and/or increased interest rates. In the case of debit cards, it has means reduced card benefits, increased bank-account fees, and overdraft charges. Some notable examples:

1. Australia: Fewer rewards, higher annual fees, and companion cards

When the Reserve Bank of Australia (RBA) imposed price controls on credit-card interchange fees in 2003, it made clear that one of its objectives was to reduce the use of credit cards by making them less attractive as a payment solution for consumers.[61] The ploy appears to have worked, as annual fees for rewards credit cards rose, and the rate of rewards fell significantly:

- Between 2002 (the year before the regulation came into effect) and 2004, the annual fee on a “standard” rewards credit card increased by 40% and the fee on a “gold” rewards card rose by 30%, from A$98 to A$128.61F[62]

- Between 2003 and 2011, the estimated benefit of rewards fell by one third, from $0.81 to $0.54 per dollar spent.59F[63]

In addition, issuers introduced caps on the total number of rewards that could be earned in a given period.[64] This turns the conventional rewards-card model on its head: instead of creating incentives to use the rewards card more to achieve specific additional benefits, Australian credit-card issuers now provide incentives for rewards-card holders to switch cards when they reach the cap.

Shortly after Australia’s interchange-fee caps for four-party cards came into force in 2003, two banks introduced three-party credit cards with annual fees and rewards similar to those that previously existed on their four-party cards.72F[65] In addition, several issuers introduced packages of two similar premium rewards cards, one that operates on a four-party network and one that operates on a three-party network.73F[66] The reason these “companion cards” were created is that far fewer merchants accept three-party cards than four-party cards; with both cards, consumers could use the higher-earning three-party card where it is accepted and the lower-earning four-party card elsewhere.

Unsurprisingly, the market share of three-party cards, while still relatively small, increased considerably following the 2003 regulations. By volume of transactions, three-party cards increased from about 10% in 2002 to about 16% in 2013 (a 60% increase). By value of transactions, they increased their market share from about 15% in 2002 to more than 20% in 2013 (a 33% increase).

In October 2015, the RBA designated American Express Companion Cards a “payment system”74F[67] and subsequently announced that, as of July 1, 2017, the cards would be subject to the same interchange-fee caps as other designated cards.75F[68] Following the introduction of these caps, companion cards were discontinued and the market share by volume of three-party cards fell back to between 7% and 8% (but subsequently rose again slightly to about 8%).76F[69] By value, three-party cards’ market share of transactions also fell steeply after mid-2017, but is now back to about 20%.[70]

2. Spain: Fewer rewards, higher interest rates, higher fees

In 2005, the Spanish government introduced gradually tightening price controls on interchange fees by “agreement” with the country’s banks. For credit cards, the controls started at 1.4% in 2006, falling to 0.79% in 2009-10. In response, local issuers reduced the rewards available from cards.57F[71] Meanwhile, from 2008 to 2010, issuers increased interest rates on credit cards from an average of 3% above the European Central Bank (ECB) base rate in 2005 to 4.6% above base.58F[72] As a result, income from interest payments was nearly 80% higher from 2006 to 2010 than in 2005, representing a total incremental increase in income from interest over the period of about €2.6 billion (although this could be an overstatement, since we are only comparing to revenue in 2005). At the same time, average annual fees on credit cards rose by 50%, from €22.94 to €34.39, generating incremental revenue over the period of €1.7 billion.

3. EU: Fewer rewards, higher interest rates, and foreign transaction fees

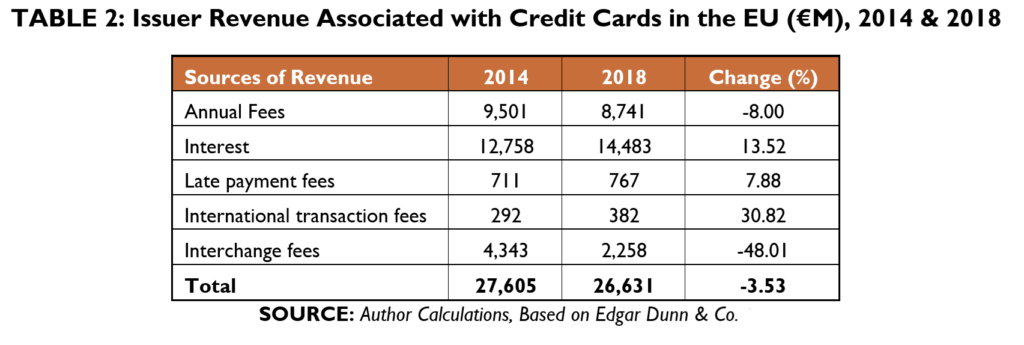

In 2014, the European Union (EU) adopted the Interchange Fee Regulation (IFR), which imposed price controls on debit- and credit-card interchange fees at 0.2% and 0.3%, respectively, with the regulation taking effect Jan. 1, 2015. The IFR initially applied only to four-party cards (primarily to Visa and Mastercard, but also some domestic payment cards).

In response to the IFR, credit-card issuers significantly reduced rewards on credit cards, or terminated rewards cards altogether.[73] Several airlines have nonetheless continued to co-brand rewards cards. American Express cards were all initially excluded from the rules, so airlines that already had an Amex co-branded card (such as British Airways) were not affected. Following a decision by the European Court of Justice in 2018, however, the IFR was deemed to also apply to co-branded cards issued by three-party networks.

As in Australia, issuers in the EU increased annual fees on cards that already had fees.[74] The total revenue from annual fees fell, however, presumably because consumers switched to cards without fees (Table 2). Issuers nonetheless made up much of the revenue lost from the interchange price controls by increasing interest rates. As noted below, this enabled them to continue to offer rewards. As Table 2 shows, while revenue from interchange fees fell by nearly 50% between 2014 and 2018, issuer revenue related to credit cards fell by less than 5%.[75]

[76]

[76]In addition, while rewards in the EU fell significantly across the board, some co-branded airline-rewards cards in the EU and the United Kingdom (which retained IFR caps on domestic transactions post-Brexit) earn at a rate that is nominally worth the equivalent of 1% to 1.5% of the amount spent on the card—that is, three to five times the interchange fee. For example, American Express (whose co-branded cards are now subject to the same fee caps as four-party cards) offers two British Airways co-branded cards in the UK, one that has an annual fee of £250 and earns 1.5 Avios per £1 on general spend, and 3 Avios per £1 spent on BA. The other card has no annual fee and earns 1 Avio per £1 spent. [77] Meanwhile, the value of each Avios is between 0.66 and 1.5p, depending on its use.[78]

There are several feasibly explanations for why the value of rewards exceeds the amount of interchange fees. First, issuers may be able to purchase airline-loyalty rewards at a significant discount. Because airlines know that they will be able to encourage holders to redeem them on flights that otherwise would not be full, the marginal cost is likely much lower than the nominal value. Second, other partner companies that redeem loyalty rewards may also be willing to do so at a discount, knowing that such redemptions both encourage loyalty to that partner and, in some cases, will only represent partial payment for goods and services, thereby acting effectively as a discount on larger purchases. Third, card issuers may be using other income—such as annual fees, interest, and late fees—to cover the shortfall. It is possible that all three explanations are true.

If card issuers in the EU are using additional revenue from higher-interest charges and late fees to cross-subsidize rewards cards—including airline co-branded rewards cards—then the IFR is effectively highly regressive. This is because late fees and interest charges are predominantly paid by individuals with lower credit scores and who spend less on their cards but keep a revolving balance, whereas rewards are earned primarily by people with higher credit scores who pay off their balance each month.

4. US: Debit cards and the Durbin amendment

When the Federal Reserve adopted Regulation II, implementing the interchange-fee price controls required by the Durbin amendment to Dodd-Frank, some covered issuing banks initially responded by stating that they would introduce consumer fees for the use of debit cards.[79] That idea immediately met with backlash, so the banks instead increased monthly account fees and increased the minimum balance required for free checking, as documented by economists at the Federal Reserve.[80] Banks also essentially eliminated rewards for debit cards. Evidence suggests that the higher bank-account charges and higher minimum-balance requirement for free checking most likely led to a significant increase in the number of unbanked individuals. [81]

Meanwhile, the evidence also suggests that consumers received little, if anything, in return. A survey conducted by economists at the Federal Reserve Bank of Richmond two years after the implementation of Regulation II found that:

[T]he regulation has had limited and unequal impact on merchants’ debit acceptance costs. In the sample of 420 merchants across 26 sectors, two-thirds reported no change or did not know the change of debit costs post-regulation. One-fourth of the merchants, however, reported an increase of debit costs, especially for small-ticket transactions. Finally, less than 10 percent of merchants reported a decrease of debit costs. The impact varies substantially across different merchant sectors.

The survey results also show asymmetric merchant reactions to changing debit costs in terms of adjusting prices and debit restrictions. A sizable fraction of merchants are found to raise prices or debit restrictions as their costs of accepting debit cards increase. However, few merchants are found to reduce prices or debit restrictions as debit costs decrease.[82]

A subsequent study by economists Vladimir Mukharlyamov and Natasha Sarin investigated the Durbin amendment’s effects on consumers using a proprietary dataset of gasoline sales in different ZIP codes.[83] (Gas is a widely consumed commodity sold in a highly competitive market, and is thus arguably the product most likely to see interchange-fee savings passed through.) The researchers found that gas is, “cheaper in ZIP codes with a greater fraction of transactions paid with debit cards issued by large banks,” which suggests that at least some retailers passed on some savings. They note, however, that “the standard deviation of per-gallon gas prices ($0.252) is 168 times larger than the average per-gallon debit interchange savings ($0.0015). Relatedly, total Durbin savings for gas merchants amount to less than 0.07% of total sales. These points render the quantification of merchants’ pass-through with statistical significance.” In other words, whatever savings retailers passed on to consumers were tiny.

At the same time, using data from bank call reports and the Federal Deposit Insurance Corporation’s summary of deposits, Mukharlyamov and Sarin found that banks covered by the price controls “collectively lost $5.5 billion in annual revenue” from interchange fees. And using data from RateWatch, they found those banks “passed 42 percent of these losses through to their customers.”[84] Specifically:

We estimate that the share of free checking accounts fell from 61 percent to 28 percent as a result of Durbin. Average checking account fees rose from $3.07 per month to $5.92 per month. Monthly minimums to avoid these fees rose by 21 percent, and monthly fees on interest-bearing checking accounts also rose by nearly 14 percent. These higher fees are disproportionately borne by low-income consumers whose account balances do not meet the monthly minimum required for fee waiver.[85]

So, while the Durbin amendment served to dramatically reduce interchange fees on debit transactions, the main effect was to increase bank fees for poorer consumers, causing some of them to leave the banking system altogether and likely become reliant on more expensive forms of credit, such as payday loans.

B. Routing Regulations

The only jurisdiction to have thus far implemented regulations mandating “competition” in network routing is the United States, which included such a mandate for debit cards in the Durbin amendment. Some other jurisdictions, most notably Australia, have contemplated such regulations. But in its most recent report on the matter, the RBA rejected mandatory “least cost routing.”[86] This subsection thus focuses on the effects of the Durbin amendment’s routing requirements.

1. The Durbin amendment routing requirements

In addition to interchange-fee price controls on “covered” issuers—i.e., banks with assets of at least $10 billion—the Durbin amendment required the Federal Reserve Board to impose routing requirements on the debit transactions of all banks. Specifically, it mandated that these regulations should prohibit issuers and payment networks from imposing network-exclusivity arrangements.[87] In particular, all issuers must ensure that debit-card payments can be routed over at least two unaffiliated networks. It also required the Federal Reserve Board to prohibit issuers and payment networks from restricting merchants and acquirers’ ability to choose the network over which to route a payment.

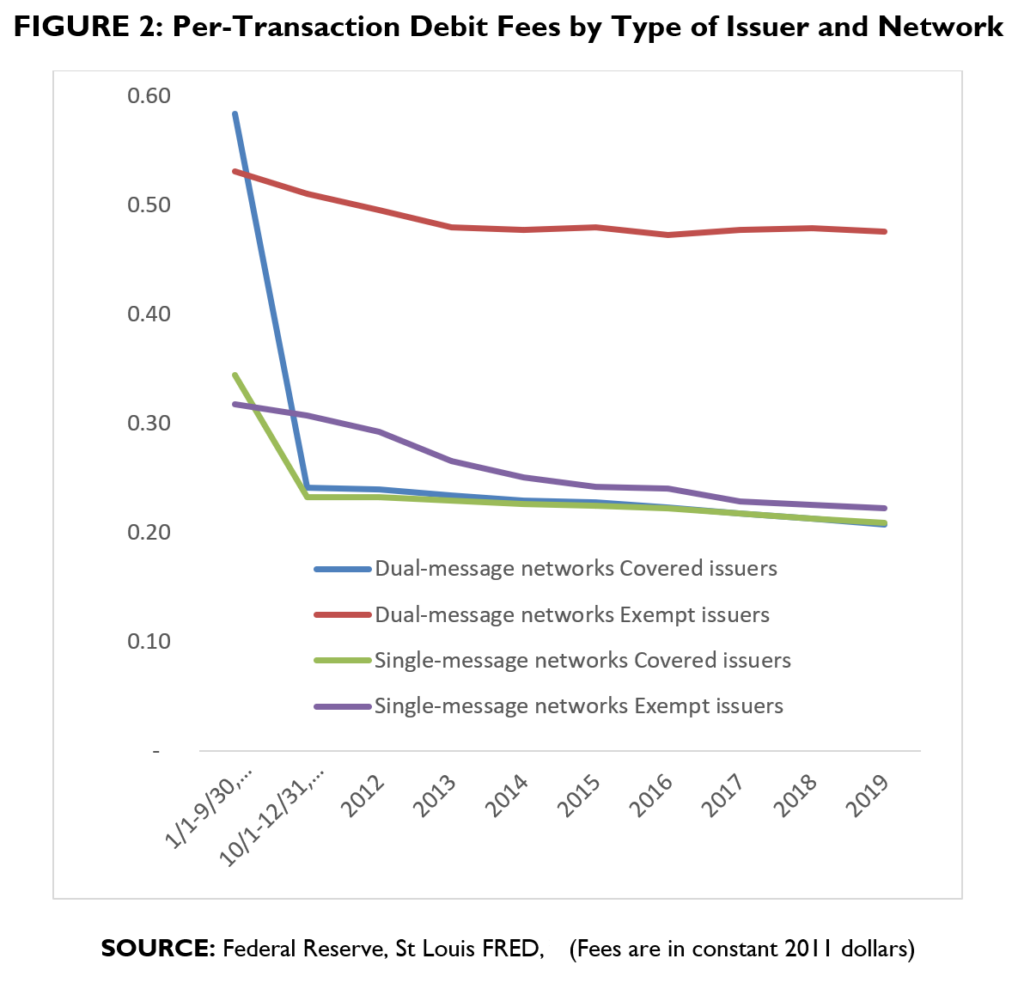

As Figure 2 shows, for covered issuers, average interchange fees per-transaction fell to the regulated maximum for both dual-message (signature) transactions and single-message (PIN) transactions immediately following implementation of the Durbin amendment in October 2011. Meanwhile, discounting for inflation, average fees per-transaction for issuers that were exempted from the price controls fell by only about 10% for dual-message transactions, which were not subject to direct competition for routing. For single-message transactions, however, routing was subject increasingly to direct competition, and average fees per-transaction for exempt issuers fell by 30% over the course of eight years; by 2019, fees were only marginally higher than the regulated maximum for covered issuers.

Based on the experience of mandatory routing under the Durbin amendment, then, it seems highly likely that the CCCA would, if implemented, drive down the price of interchange, as proponents want. And issuers would respond as they did to the Durbin amendment, by finding other ways to recoup lost revenue. Consumers would again almost certainly endure the most of this shift through higher card fees, higher interest rates, and fewer benefits, including less generous rewards.

V. How Would the CCCA Affect Co-Branded Credit Cards?

This section draws on the discussion in Section IV to infer the potential effects the CCCA would likely have on co-branded credit cards. It begins with a discussion of the effect on issuer revenue in general. It then looks at how issuers might address the loss of revenue through, e.g., increases in annual card fees, increases in interest rates and late payment fees, reduction in rewards, reduction in other benefits, and the introduction of “companion cards.” This is followed by a discussion of the potential effect on airlines.

A. Effect on Issuer Revenue

As noted, the stated intention of the CCCA is to reduce merchants’ costs by lowering interchange-fee revenue. One proponent of the CCCA has claimed that it “could result in annual savings upward of $15 billion.”[89] But this claim is not supported by any evidence; indeed, so far as this author can tell, it seems to have been plucked out of thin air.

While it is likely that interchange-fee revenue will be reduced, it is difficult to know with any degree of precision by how much, or what other effects might occur. (As to the effect on merchant costs—that is quite another matter, as will be discussed later.) Much will depend on which networks issuers include as the secondary networks on their cards. This, in turn, will likely depend on complex negotiations among the issuers, the primary networks, and the various possible secondary networks. Factors that will affect the decision regarding which network is included as a secondary network on a card are likely to include:

- The extent to which the secondary network is able to meet fraud and other security concerns of the issuer. For example, many of the alternative networks were designed to operate with ATMs, and are thus PIN-based single-message systems that do not offer dual-message transmission. Since at least some proportion of transactions on any credit card are likely to require dual-message transmission for the purposes of meeting such EMVCo standards as 3DS (in part, to limit the potential for card-not-present fraud), it is unclear how a single-message (PIN) network could be the secondary network.

- Issues related to brand reputation of the two networks. This could affect, for example, the willingness of three-party networks to function as secondary networks, because those networks have positioned themselves as premium brands. Meanwhile, similar to the issuer concerns, Visa and Mastercard would be understandably reluctant to have a network with poor security and fraud detection as a secondary network on cards bearing their brands.

- Relatedly, three-party networks might be reluctant to function as secondary networks if they expect that participation would result in a reduction in the rates they could charge merchants on their own closed-loop network.

- Whether issuers wish to and are able to issue “companion cards” by partnering with three-party networks as the sole network, as Australian banks did for a while (see Subsection B below), which might also affect three-party cards’ incentives to function as secondary networks.

- Which networks might be prohibited under Article D of the CCCA, which prohibits secondary networks that are either a national security risk or are “owned, operated, or sponsored by a foreign state entity.”[90] This would seem to eliminate China Union Pay, whose member banks are primarily state-owned. And potentially, it could be applied to any network, as “national security risk” is not well-defined.

These factors generally militate against single-message networks, three-party networks, and China Union Pay becoming secondary networks on credit cards. As such, many covered issuers might plausibly choose JCB Co. Ltd. (formerly Japan Credit Bureau) as their secondary network, assuming that JCB is not deemed to be a national security risk. JCB is a member of EMVCo and applies the same basic security standards as other EMVCo companies (Visa, Mastercard, American Express, Discover, and China Union Pay).[91] Unlike China Union Pay, however, JCB is a private enterprise, and so should not fall afoul of Article D of the CCCA. JCB has an agreement with Discover that enables JCB cardholders to use their cards in the United States by running them over the Discover network. By adding JCB as the secondary network, issuers would therefore effectively utilize Discover’s network, including the application of EMVCo rules, such as 3DS, which provides enhanced fraud protection for card-not-present transactions.[92]

Since the JCB secondary network would actually be run over the Discover network, the interchange rates that would be applied would presumably be Discover’s, which are similar on average to those of Visa and Mastercard, but appear to be slightly higher for standard cards and slightly lower for the higher-end rewards-type cards.[93] Assuming cards are programmed to apply interchange rates for somewhat equivalent products, the initial effect of the CCCA on interchange-fee revenue could, in theory, be modest.

That sounds like good news. Over the medium to longer term, however, this artificial “competition” between the networks on the card would almost inevitably lead to a gradual reduction in fees, as each network seeks to attract more users in each category. This is precisely what happened with PIN debit networks for banks and credit unions that were exempted from the Durbin amendment’s price controls on interchange fees. This would continue until each network could barely cover its costs in each category. In that case, the effect on interchange-fee revenue could be devastating.

The analogy here is not to the dynamic competition that drives innovation in conventional markets, guided by a process of price discovery that seeks to provide consumers with better goods and lower prices through the development of more efficient processes that consume fewer resources. The analogy here is, rather, the “tragedy of the commons,” or more precisely, the tragedy of open access. In effect, by forcing networks to compete on price alone—maximizing use, while minimizing expenditure on improvements—the result will be diminution in network quality, just as when anglers chase after fish stocks until they are economically exhausted (too depleted to be worth chasing).[94]

We can push the overfishing analogy further. Initially, fishers often do not notice that they are depleting the stock, but over time, they have to increase the amount of effort they put into fishing until the returns no longer justify the investment. A similar thing could happen with payment networks, with the effects initially being muted by decades of investment in security protocols and the collection of transaction data. But over time, the value of those investments and data will wither.

The solution to the open-access problem has been well-known to economists for more than half a century: establish clearly defined and readily enforceable property rights.[95] This has proved challenging in fisheries, but an increasing number of jurisdictions have developed successful approaches of various kinds.[96]

The irony is that the networks have expressly sought to avoid this tragedy by developing clear rules regarding who has access to the data transmitted from their cards, how it is transmitted, to whom, and under what conditions.

Interchange fees, as they exist today, are one of those rules: they are the default in open-network schemes and exist, at least in part, because of the high costs of negotiating and enforcing many bilateral agreements among banks.[97] They are set by payment-network operators, who are able to avoid the problems that would arise if individual issuing banks set their own fees. The latter might lead to fees being set at inefficiently high levels in order to maximize issuing-bank revenue, without regard to the impact on the value of the system as a whole.21F[98]

The CCCA would run roughshod over those rules.

B. Response by Issuers to Compensate for Revenue Losses

Proponents of the CCCA seem to assume that issuers will simply accept the loss of revenue from interchange fees and do nothing to try to compensate. Based on the experience of both the Durbin amendment and of interchange regulations in other jurisdictions, this is an incorrect assumption.

In practice, it seems almost certain that card issuers would implement one or more of several measures to recover the lost revenue and/or reduce costs. Among other things, they might:

- Increase annual card fees. In Australia, banks increased annual card fees by 30% to 40%. In Europe, they increased them by about 13%.[99] Such fees tend to be regressive, because they are charged at a fixed rate regardless of how much a cardholder spends. Thus, for lower-income cardholders who spend less, such a fee increase would be proportionately more onerous.

- Remove insurance and other benefits. Many U.S. credit cards currently offer cardholders a range of benefits, often including purchase-protection insurance, car-rental insurance, travel insurance, and fee-free international transactions. These benefits were also common on cards issued in the EU prior to the introduction of the IFR, but were removed afterwards. As a result, most cards—including rewards cards—now have limited, if any, insurance and charge a transaction fee of between 2% and 3% for international transactions.

- Increase late-payment fees (if not prohibited from so doing by other regulations) and interest rates. In the EU, issuers increased late-payment fees and interest rates following the introduction of the IFR. Between 2014 and 2016, interest rates on revolving balances rose from an average of 16.2% to 18.8%, while the European Central Bank base rate fell from 0.3% to 0.25%. This implies an increase in average real rates on credit cards of 2.75%. Likewise, in Spain, credit-card interest rates were increased at a substantially faster rate than increases in rates at the European Central Bank, with the result that revenue from interest rose by 80% during the period when IFRs were subject to national price controls on interchange fees, from 2006 to 2010.

The determination of which fees to increase and by how much will depend on issuers’ views regarding the willingness of cardholders to bear such fees. Likewise, the determination of which benefits to withdraw on which cards will be made—possibly simultaneously with the determination of any increase in annual fees (which could be used to cover such benefits in whole or in part)—on the basis of the effects such changes will have on demand for cards.

1. Responses by issuers of co-branded rewards cards

As noted earlier, issuers typically cover the costs of rewards on co-branded cards through some combination of annual fees and interchange fees. Issuers also often pay for other items, ranging from lounge access for cardholders to marketing fees for promoting the card and related services, the costs of which also must be paid for by some combination of merchants and users.

Since the costs associated with co-branded rewards cards are typically higher than the costs of other non-rewards cards, the effects of the CCCA would likely be much more severe for such co-branded cards. As such, issuers of co-branded cards may seek to implement additional measures in order to recover revenue and ensure that they meet their obligations to cardholders and co-brand partners.

2. Responses by issuers of airline-rewards co-branded cards

As noted, in the UK and some EU jurisdictions, issuers have continued to co-brand credit cards with airlines. Moreover, while rewards have been reduced significantly, and many other card benefits—such as insurance and fee-free foreign transactions—have largely been eliminated, the amount earned in rewards per euro or pound spent remains notionally higher than the interchange fee on the card. As also noted, there are several possible explanations for this, including that airlines may sell rewards at a discount, or that issuers were able to make up some of the losses on interchange fees by increasing interest rates, late fees, and foreign transaction fees. If the CCCA were enacted, we might see issuers adopt some combination of these approaches.[100]

In Australia, issuers put caps on the amounts of rewards that could be earned. As noted, this effectively inverts the purpose of such rewards, which are intended to engender loyalty, but if the amount that can be earned is capped or the earning rate declines after a certain spend, then users will have incentives at that point to switch to a different card. While this would reduce the loyalty element of the co-branded card (perversely encouraging disloyalty, in fact), U.S. issuers of multiple co-branded cards might be motivated to pursue this approach in order to drive short-term spending on each of their cards, especially if they have agreements to purchase a certain number or rewards at a discounted price.

C. The Effect on Airlines and Their Response

The effect of the CCCA on airlines will depend very much on which networks become secondary networks, whether issuers are able to issue companion cards, and all the other factors discussed above. But in almost any imaginable scenario, the airlines that currently co-brand four-party credit cards will see a reduction in revenue. In many scenarios, that revenue reduction could be significant—in some cases it could be 5% to 10% of total revenue. While this would be partly offset by a reduction in liability associated with outstanding loyalty-rewards points, there is a timing mismatch effect: The revenue loss will occur in the short term, while the rewards-redemption effect occurs over a longer time horizon.

In addition, to the extent that airlines are unable either to offer companion cards or switch altogether to three-party cards—and thereby offer their loyal customers continued benefits at a similar level to those available on their current cards—there will almost certainly be some attrition of loyalty. In other words, some proportion of fliers who are currently loyal to American, United, Southwest, JetBlue, Alaska, and other smaller airlines with four-party co-branded credit cards will switch to Delta. Moreover, the evidence suggests that those most likely to switch will be those most adversely affected by the change—that is to say, those who tend to spend the most on their co-branded rewards card.

This likely includes many middle-class consumers who live far away from family members and currently value the rewards from their co-branded card highly. To the extent that those individuals are also among the most loyal to the airlines whose co-branded cards they use, this could have a seriously detrimental effect on the profit margins of the other airlines.

The CCCA may also affect many airlines’ costs of capital. For example, at least for United and American Airlines, a reduction in expected revenue from the sale of rewards could result in the downgrading of the bonds issued during the COVID-19 pandemic by the subsidiaries that now own the rewards programs. That could trigger covenants requiring the parent companies to post additional capital, which in turn would increase the parents’ capital costs. In general, the combination of reduced revenue and reduced membership of loyalty programs—leading to lower revenue from higher-value customers—would reduce airlines’ expected future profitability, which would increase capital costs. In times when demand for air travel is high, this may not pose a dramatic problem. It would, however, likely affect fleet investment, which would adversely affect the flying experience and might lead to the termination of some routes. And in a downturn, it could result in the bankruptcy that the airlines previously avoided, thanks to their ability to securitize their loyalty programs.

VI. Conclusions

This study has focused relatively narrowly on the likely effects of the CCCA on co-branded reward credit cards and the knock-on effects on the co-brand partners, especially airlines. If enacted, however, the law’s effects would be far broader. For example, it would likely cause a reduction in investment in innovation by card issuers and networks for at least two reasons. First, by reducing prospective revenue, the CCCA would reduce network providers’ incentive and ability to invest in innovation. Second, by requiring networks to make tokens interoperable, the CCCA dramatically reduces the incentive to invest in improvements to the security, convenience, and other aspects of tokenized transactions.

Proponents of the Credit Card Competition Act (CCCA) claim that it would “enhance credit card competition and choice in order to reduce excessive credit card fees.” In fact, by forcing the majority of credit-card issuers in the United States to include a second network on all their cards, the CCCA would remove the choice of network from the issuer and cardholder and place it in the hands of the merchant and the acquiring bank.

Indeed, the name of the Credit Card Competition Act would appear to be unintentionally ironic, since one of its main effects would be to reduce competition between issuers, as margins would be reduced, and issuers would be less able to differentiate on the basis of such offerings as co-branded cards (airlines, hotels, retailers). As a result, there would be less pressure to compete on interest rates, which in turn would mean that—as happened in the EU and especially in Spain—issuers would likely increase interest rates in order to offset reduced interchange-fee revenue.

To the extent that issuers use this offsetting revenue from interest to enable them to continue to offer some level of rewards, the CCCA would have brought about what some critics of credit-card rewards have previously falsely accused issuers of doing: using credit cards to transfer wealth from lower-income, lower-spending consumers who maintain a revolving balance to higher-income, higher-spending consumers who pay off their balances every month.[101]

Even if issuers do continue to offer rewards, the evidence from Europe and Australia is that the CCCA would cause such rewards to be diminished significantly, harming consumers both directly and indirectly. The direct harms would come in the form of fewer rewards (except for those consumers who only use three-party cards). The indirect harms would come through the effects on businesses that currently rely heavily on revenue from co-branded cards that would be diminished by the CCCA.

As this study has demonstrated, airlines, in particular, could be adversely affected, leading to reduced fleet investment, termination of routes, and potentially to bankruptcy. There would also likely be a broader adverse effect, as consumers reduce their use of credit cards (including some who give them up), which would result in an overall reduction in consumption—harming both merchants and the broader economy.

Appendix: Routing in Payment Networks

When a cardholder submits a transaction for payment, information regarding that payment is sent over a proprietary network. This is called “routing.” There are, broadly, two types of payment network: single-message (PIN) networks that emerged from ATM networks, and dual-message (signature) networks that were developed by the credit-card networks (Visa, Mastercard, American Express, and Discover). In general, credit cards require dual-message networks, whereas debit transactions can run over either type of network. To understand why, it is worth briefly explaining the mechanics of the two systems.

- Single-message (PIN) debit networks

Single-message networks rely on the PIN stored in the card to authenticate a transaction. As a result, the only message that is required is a notification to the issuing bank to debit the account of the cardholder in the amount they have authorized, and to credit that amount the account of the merchant—less the discount fee, which is paid to the acquiring bank. Because of the nature of the transaction, settlement can be effected over banks’ electronic-funds-transfer (EFT) networks that were initially built to settle transactions at shared ATMs, and then over networks of ATMs.[102]

- Dual-message (signature) networks

As the name suggests, dual-message networks send two messages: the first is a request for authorization sent to the issuing bank, which confirms the authenticity of the card, checks whether the cardholder has sufficient credit available, and monitors for fraud. If authorized, the second message contains information confirming the amount to be credited to the merchant’s account during clearing and settlement.

For example, if you present your credit card at a sit-down restaurant, the check total would be authorized by the network and a “hold” or “pending transaction” amount would appear on your account. The opportunity to add a tip to the bill permits a second, later message that authorizes payment of the full amount of food, plus a tip to be credited to the merchant. Similar “holds” are also often used by online merchants in order to delay payment (sometimes by as much as several days), thereby reducing the likelihood of fraud and associated chargebacks.[103]

[1] See Developments in Noncash Payments for 2019 and 2020: Findings From the Federal Reserve Payments Study, Federal Reserve Board, (Dec. 2021), available at https://www.federalreserve.gov/publications/files/developments-in-noncash-payments-for-2019-and-2020-20211222.pdf, along with the various previous studies and associated data, https://www.federalreserve.gov/paymentsystems/frps_previous.htm.

[2] See, e.g., Mastercard Rules, Mastercard, https://www.mastercard.us/en-us/business/overview/support/rules.html (last accessed Nov. 16, 2023); Visa Rules and Policy, Visa, https://usa.visa.com/support/consumer/visa-rules.html (last accessed Nov. 16, 2023).

[3] 156 Cong. Rec. S3,571 (daily ed. May 12, 2010), available at https://www.congress.gov/111/crec/2010/05/12/CREC-2010-05-12-pt1-PgS3569-9.pdf.

[4] Claire Tsosie, The History of the Credit Card, NerdWallet.com (Mar. 15, 2021), https://www.nerdwallet.com/article/credit-cards/history-credit-card; see also Jeremy Norman, The Charga-Plate, Precursor of the Credit Card, Circa 1935 to 1950, HistoryofInformation.com, https://www.historyofinformation.com/detail.php?id=1710 (last accessed Nov. 16, 2023).

[5] See Todd J. Zywicki, The Economics of Payment Card Interchange Fees and the Limits of Regulation, International Center for Law & Economics (Jun. 2, 2010), available at http://laweconcenter.org/images/articles/zywicki_interchange.pdf. Several banks also attempted to establish three-party cards during the 1950s. Most of these were unsuccessful. The exception was Bank Americard, which subsequently became a four-party system and eventually rebranded as Visa.