ICLE Comments to Federal Reserve Board on Regulation II NPRM

Executive Summary

In this comment, we argue that the Federal Reserve Board’s interpretation of the Durbin amendment has had the opposite effect to that intended by the legislation. Specifically, it has harmed lower-income consumers and benefited the shareholders of large merchants. To understand how and why this has happened, we look at two aspects of the provision’s implementation: the price controls the Board imposed through Regulation II, and the competitive-routing requirement included in the Durbin amendment itself. We then consider the likely effects of the changes proposed in the NPRM and conclude that these will exacerbate the harms already inflicted by Regulation II. We encourage the Board to consider alternative approaches that would mitigate Regulation II’s harms, including raising or, ideally, eliminating the cap on interchange fees.

I. Introduction

The International Center for Law & Economics (“ICLE”) thanks the Board of Governors of the Federal Reserve System (“Board”) for the opportunity to comment on this notice of proposed rulemaking (“NPRM”), which calls for updates to components of the interchange-fee cap established by Regulation II.[1]

Section 1075 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”)—commonly referred to as the “Durbin amendment”—required the Board to issue regulations that would limit debit-card interchange fees charged by lenders with assets of more than $10 billion (“covered banks”), such that:

The amount of any interchange transaction fee that an issuer may receive or charge with respect to an electronic debit transaction shall be reasonable and proportional to the cost incurred by the issuer with respect to the transaction.[2]

Sen. Richard Durbin (D-Ill.) stated in 2010 that his amendment “would enable small businesses and merchants to lower their costs and provide discounts for their customers.”[3] Yet the evidence to date demonstrate that, in practice, the provision has done little, if anything, to reduce costs for small businesses and merchants; indeed, many have seen costs rise.[4] Meanwhile, consumers have seen little, if any, savings from merchants, and have been harmed by higher banking fees.[5]

These problems are, at least in part, a consequence of the way the Board chose to interpret the phrase “reasonable and proportional to the cost incurred by the issuer with respect to the transaction.” Specifically, as the Board notes in its summary of the present NPRM:

Under the current rule, for a debit card transaction that does not qualify for a statutory exemption, the interchange fee can be no more than the sum of a base component of 21 cents, an ad valorem component of 5 basis points multiplied by the value of the transaction, and a fraud-prevention adjustment of 1 cent if the issuer meets certain fraud-prevention- standards.

The Board now proposes to reduce further the interchange fees that covered banks may charge for debit-card transactions. Specifically:

Initially, under the proposal, the base component would be 14.4 cents, the ad valorem component would be 4.0 basis points (multiplied by the value of the transaction), and the fraud-prevention adjustment would be 1.3 cents for debit card transactions performed from the effective date of the final rule to June 30, 2025.

In this comment, we question the Board’s interpretation of the underlying legislation by citing, among other things, research conducted by employees of the Board and published by the Board.

II. Can Price Controls Be Reasonable and Proportional?

The heart of the matter is the meaning of “reasonable and proportional to the cost incurred by the issuer with respect to the transaction.” In most respects, the Board has chosen to interpret this phrase narrowly to refer to the pecuniary costs directly associated with the electronic processing of each transaction ($0.21 plus 0.05% of the value of the transaction). But even in deploying this narrow interpretation, the Board has been inconsistent, as:

- These fees represent, at best, an average of the pecuniary cost; and

- The Board permits issuers to add $0.01 if it “meets certain fraud-prevention standards.” [6]

This latter component clearly is not transaction-specific, as it is intended to cover the cost of investments made in security infrastructure.

A. What’s in a Cost?

The Board’s approach to “cost” fails to consider the two-sided nature of payment-card markets. A 2017 staff working paper by Board economists Mark D. Manuszak and Krzysztof Wozniak notes:

Interchange fees play a central role in theoretical models of payment card networks, which emphasize the card market’s two-sided nature (for example, Rochet and Tirole (2002)).[7] On one side of the market, interchange fees alter acquirers’ costs, influencing the transaction fees they charge merchants. On the other side of the market, inter- change fees provide a source of revenue that defrays issuers’ costs of card services for accountholders, and, thus, influence fees that banks charge accountholders. As a result, these theoretical models broadly predict that a reduction in interchange fees will induce issuers to increase prices for accountholders.

However, theoretical models of two-sided markets rely on an overly simple characterization of issuers, which diverges from reality in three important ways. First, issuers use nonlinear, account-based pricing rather than per-transaction fees typically assumed by the theory but rarely observed in reality. The theoretical literature on nonlinear pricing emphasizes the sensitivity of consumer demand to different price components. For the debit card industry, it predicts that higher costs will result in increases in prices for which consumers’ demand is less sensitive, and lower or no rises in prices to which the demand is more sensitive.

Second, issuers are multiproduct firms, cross-selling a variety of products in addition to card transactions. The theoretical literature on multiproduct pricing predicts that a firm’s price for one good will internalize its impact on the demand for the firm’s other products. In the debit card industry, this implies that, since a bank is best positioned to offer additional services to consumers who are already its accountholders, the price for such an account is less likely to reflect higher costs than it would otherwise.

Finally, issuers are heterogeneous firms, subject to idiosyncratic cost shocks based on their status under the regulation, and compete for customers in the market for banking services. An issuer’s prices are not determined in isolation by its costs and the market demand, but rather jointly with other issuers’ prices…. [8]

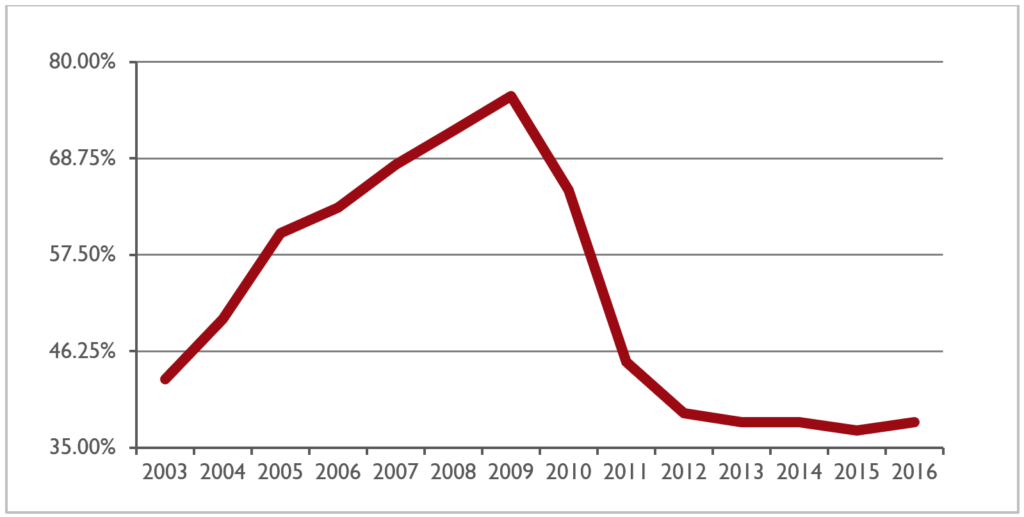

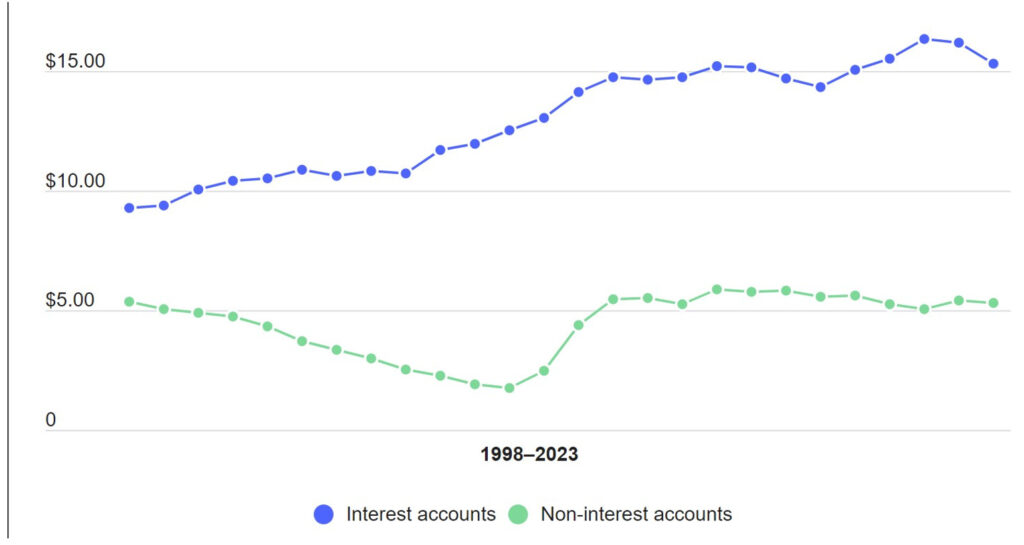

In the decade prior to the Dodd-Frank Act, banks had increased the availability of free checking accounts (Figure I) and reduced the fees on non-interest-bearing checking accounts (Figure II), which had widespread benefits. First, it enabled more people to open and maintain bank accounts, thereby reducing the proportion of unbanked and underbanked Americans. Second, it contributed to a shift toward electronic payments, as many consumers who previously lacked access to payment cards now had a debit card (Figure III). This shift was driven along further by banks offering rewards that encouraged the use of debit cards. Since the provision of checking accounts generates associated costs, banks that expanded their offerings of free and/or low-fee accounts had to recoup those costs elsewhere. They did so, in part, through revenue from interchange fees on debit cards.

In a 2014 staff working paper, Board economists Benjamin S. Kay, Mark D. Manuszak, and Cindy M. Vojtech found that Regulation II reduced annual interchange-fee revenue at covered banks by $14 billion.[9] Meanwhile, in their aforementioned 2017 paper, Manuszak and Wozniak showed that, following Regulation II’s implementation, covered banks sought to recoup the revenue lost due to lower interchange fees by increasing fees on checking accounts; reducing the availability of free checking accounts; and increasing the minimum balance required to maintain a free checking account. This resulted in “lower availability of free accounts, higher monthly fees, lower likelihood that the monthly fee could be avoided, and a higher minimum balance to avoid the fee.”[10]

Moreover, Manuszak and Wozniak show that “checking account pricing at covered banks appears primarily driven by the interchange fee restriction rather than other factors related to the financial crisis or subsequent regulatory initiatives.”[11] Finally, in the version of Kay et al.’s paper published in the Journal of Financial Intermediation, the authors “find that retail banks subject to the cap were able to offset nearly all of lost interchange income through higher fees on deposit services.”[12]

In a more recent study, Georgetown University economist Vladimir Mukharlyamov and University of Pennsylvania economist Natasha Sarin estimated that Regulation II caused covered banks to lose $5.5 billion annually, but that they recouped 42% of those losses from account holders. As a result:

the share of free checking accounts fell from 61 percent to 28 percent as a result of Durbin. Average checking account fees rose from $3.07 per month to $5.92 per month. Monthly minimums to avoid these fees rose by 21 percent, and monthly fees on interest-bearing checking accounts also rose by nearly 14 percent. These higher fees are disproportionately borne by low-income consumers whose account balances do not meet the monthly minimum required for fee waiver.[13]

FIGURE 1: Proportion of Banks Offering Free Checking Accounts, 2003-2016

SOURCE: Bankrate

FIGURE II: Average Fees for Checking Accounts, 1998-2023

SOURCE: Bankrate

FIGURE III: US Shares of Noncash Payments by Transaction Volume, 2000-2020

SOURCE: Authors’ calculations based on data from Federal Reserve payment studies

B. Effects on ‘Exempt’ Banks and Credit Unions

In a letter to Senate Banking Committee Chairman Chris Dodd (D-Conn.), House Financial Services Committee Chairman Barney Frank (D-Mass.), and the conferees selected to finalize the Dodd-Frank Act, Durbin claimed that:

Under the Durbin amendment, the requirement that debit fees be reasonable does not apply to debit cards issued by institutions with assets under $10 billion. This means that Visa and MasterCard can continue to set the same debit interchange rates that they do today for small banks and credit unions. Those institutions would not lose any interchange revenue that they currently receive.[14]

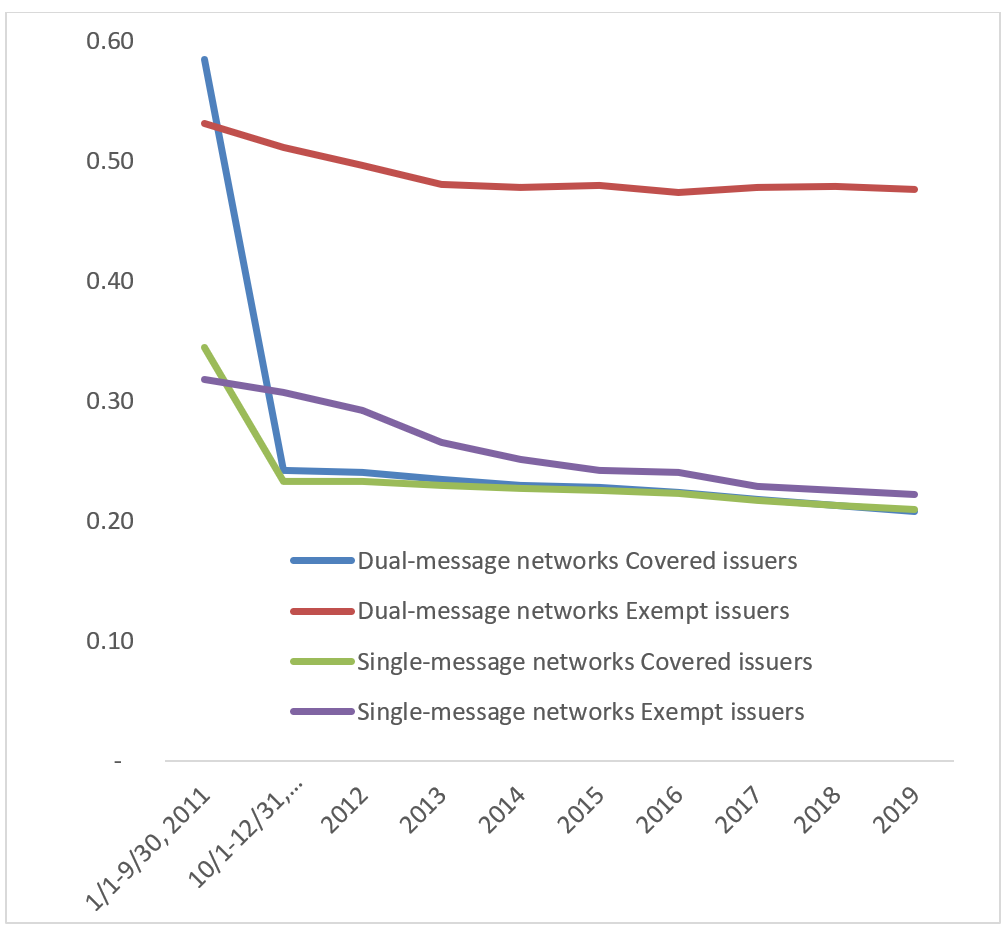

Yet as can be seen clearly in Figure IV, average per-transaction debit-card interchange fees fell across the board. For covered issuers, average interchange fees per-transaction fell to the regulated maximum for both covered dual-message (signature) transactions and single-message (PIN) transactions immediately following implementation of Regulation II in October 2011. Meanwhile, adjusting for inflation, average fees per-transaction for exempt issuers fell by about 10% for dual-message transactions.

Average fees per-transaction for single-message transactions, however, fell by 30% over the course of eight years. By 2019, they were only marginally higher than the regulated maximum for covered banks, despite the claimed intent to protect smaller issuers from the effects of the debit-interchange cap. The cause of this decline was the addition of the following subsections to the Electronic Fund Transfer Act (EFTA):[15]

- EFTA Section 920(b)(1) prohibits issuers and payment networks from imposing network-exclusivity arrangements. In particular, all issuers must ensure that debit-card payments can be routed over at least two unaffiliated networks.

- EFTA Section 920(b)(1)(B) prohibits issuers and payment networks from restricting merchants and acquirers’ ability to choose the network over which to route a payment.

These changes, which were dictated by the Durbin amendment, enabled merchants to route transactions over lower-cost networks. That has effectively forced the networks subject to such competition—primarily single-message (PIN) networks—to reduce the fees set for exempt banks so that they are in line with those set for covered banks.

This has inevitably caused many exempt banks and credit unions to experience losses similar to those experienced by covered banks. Indeed, in some cases, the effects have been markedly worse, because smaller banks and credit unions lack the advantage of scale.

FIGURE IV: Fee Per Transaction, Covered v Exempt Users, Single v Dual Message Networks (2011 Dollars)

SOURCE: Federal Reserve, St. Louis FRED[16]

C. Asymmetric Pass-Through

In a 2014 paper published by the Federal Reserve Bank of Richmond, Zhu Wang, Scarlett Schwartz, and Neil Mitchell analyzed the results of a then-recent merchant survey conducted by the Federal Reserve Bank of Richmond and Javelin Strategy & Research, which sought to understand the Durbin amendment’s effects on merchants and the response of those merchants. The authors found that, while some merchants enjoyed reductions following Regulation II’s implementation in the merchant-discount rate they paid, others saw their debit-card acceptance costs rise.[17] They also found an asymmetric response: merchants who saw their prices increase typically passed those increased costs onto their customers, while very few of those who saw their debit costs decrease passed those savings onto customers.

Using proprietary data from banks and one of the card networks, economists Vladimir Mukharlyamov and Natasha Sarin estimated that merchants passed through “at most” 28% of their debit-card interchange-fee savings to consumers.[18] The “at most” is worth qualifying: the authors base their analysis on savings at gas stations, but they note that:

It turns out, however, that the standard deviation of per-gallon gas prices ($0.252) is 168 times larger than the average per-gallon debit interchange savings ($0.0015). Relatedly, total Durbin savings for gas merchants amount to less than 0.07% of total sales. These points render the quantification of merchants’ pass-through with statistical significance virtually impossible. The existence of payment instruments exempt from Durbin and the presence of a fixed component in the regulation’s interchange-fee formula further complicate pass-through even for merchants willing to share savings, however small, with consumers.[19]

Meanwhile, as noted, they estimated that banks passed through 42% of their interchange-fee revenue losses to consumers. They estimate that the net result of this was a $4 billion transfer to merchants, of which $3.2 billion came directly from banks and $0.8 billion from consumers, who paid $2.3 billion more in higher checking fees, but received only $1.5 billion in lower retail prices.

D. Effects on Lower-Income Consumers

In a 2014 ICLE paper, Todd Zywicki, Geoffrey Manne, and Julian Morris offered a back-of-the-envelope calculation of the best-case scenario for the net effect of Regulation II on the “average” American consumer:

In 2012, the average household spent $30,932 in total on food, apparel, transportation, entertainment, healthcare, and other items that could have been purchased using a payment card (out of a total household expenditure of $51,442). If all of those items were purchased on debit cards and all were purchased from larger retailers and those larger retailers passed on all their savings (averaging 0.7%), then the average household would have saved $216.50. And that is the absolute best case – and most unlikely – scenario. But now assume that average household has two earners, each with a bank account that was previously free but now costs $12 per month. In that case, the household’s costs would have risen by $71.50 as a result of the Durbin Amendment. In other words, even in the best case, lower-middle income and poorer households who have lost access to a free current account—which is likely a majority—will be worse off after the Durbin Amendment.[20]

While the average consumer likely fared poorly, Regulation II was, quite frankly, a disaster for many lower-income consumers. Using data from the Board’s Survey of Consumer Finances, Mukharlyamov and Sarin found that:

over 70 percent of consumers in the lowest income quintile (annual household income of $22,500 or less) bear higher account fees, since they fall below the average post-Durbin account minimum required to avoid a monthly maintenance fee ($1,400). In contrast, only 5 percent of consumers in the highest income quintile (household income of $157,000 or more) fall below this threshold.[21]

Worse, Regulation II almost certainly resulted in an increase in the number of unbanked Americans. Mukharlyamov and Sarin note:

Nearly 8 percent of Americans were unbanked in 2013, with nearly 10 percent of this group becoming unbanked in the last year. Using data from the FDIC National Survey of Unbanked and Underbanked Households, in Table 12 we show that immediately following Durbin there is a significant growth (81 percent increase relative to survey pre-Durbin) in the share of the unbanked population that credits high account fees as the main reason for their not having a bank account. This difference is significant at the 1 percent level.

Respondents in states most impacted by Durbin (those with the highest share of deposits at banks above the $10 billion threshold) are most likely to attribute their unbanked status post-Durbin to high fees (over 15 percent of those surveyed in the highest Durbin tercile). The growth in the recently unbanked (those who had accounts previously but closed them within the last year) is also highest in states with the most Durbin banks, where the increase in account fees is most pronounced. As with the overall sample, these differences are significant at the 1 percent level. This suggests that at least some bank customers respond to Durbin fee increases by severing their banking relationship and potentially turning to more expensive alternative financial services providers such as payday lenders and check-cashing facilities.[22]

III. Conclusion

It is worth noting that the Board was well aware of the two-sided nature of payment-network markets and the implications for setting interchange fees prior to issuing Regulation II. A 2009 staff working paper by Robin A. Prager, Mark D. Manuszak, Elizabeth K. Kiser, and Ron Borzekowski stated:

A few characteristics of an efficient interchange fee are worth noting:

-

In general, an efficient interchange fee is not solely dependent on the cost of producing a card-based transaction nor is it equal to zero.

-

An efficient interchange fee may yield prices for card services to each side of the market that are “unbalanced” in the sense that one side pays a higher price than the other.

-

The efficient interchange fee for a particular card network is difficult to determine empirically.[23]

Based on the foregoing analysis, it appears clear that the optimal debit-card interchange fee is higher than that currently permitted for covered banks under Regulation II—and for exempt banks subject to Durbin’s routing mandates. It is, therefore, rather disconcerting that the Board would contemplate reducing the interchange fee further still in the NPRM to which this comment is addressed. If the Board wished to establish a “reasonable and proportional” fee for debit-card interchange, it would instead raise the cap. Indeed, since it remains “difficult to determine empirically” the efficient interchange fee for any card network, the Board should acknowledge that markets are the best mechanism to establish such fees, and remove the price controls altogether.

[1] Debit Card Interchange Fees and Routing, 88 Fed. Reg. 78100 (Nov. 14, 2023), https://www.federalregister.gov/documents/2023/11/14/2023-24034/debit-card-interchange-fees-and-routing.

[2] Pub. L. 111–203, 124 Stat. 1376 (2010), available at https://www.govinfo.gov/content/pkg/PLAW-111publ203/pdf/PLAW-111publ203.pdf.

[3] Press Release, Durbin Sends Letter to Wall Street Reform Conferees on Interchange Amendment, Office of Sen. Richard Durbin (May 25, 2010), https://www.durbin.senate.gov/newsroom/press-releases/durbin-sends-letter-to-wall-street-reform-conferees-on-interchange-amendment.

[4] Zhu Wang, Scarlett Schwartz, & Neil Mitchell, The Impact of the Durbin Amendment on Merchants: A Survey Study, 100 (3) Econ Quar. (Fed. Rsrv. Bank of Richmond) 183-208 (2014).

[5] Todd J. Zywicki, Geoffrey A. Manne, & Julian Morris, Price Controls on Payment Card Interchange Fees: The U.S. Experience, George Mason Law & Economics Research Paper No. 14-18 (2014); Geoffrey A. Manne, Julian Morris, & Todd J. Zywicki, Unreasonable and Disproportionate: How the Durbin Amendment Harms Poorer Americans and Small Businesses, Int’l. Ctr. Law & Econ. (Apr. 25, 2017), available at https://laweconcenter.org/wp-content/uploads/2017/08/icle-durbin_update_2017_final-1.pdf.

[6] 76 Fed. Reg. 43394 (Jul. 20, 2011), https://www.federalregister.gov/documents/2011/07/20/2011-16861/debit-card-interchange-fees-and-routing and specifically 76 Fed. Reg. 43466 (Jul. 20, 2011), available at https://www.govinfo.gov/content/pkg/FR-2011-07-20/pdf/2011-16861.pdf; Debit Card Interchange Fees and Routing (Regulation II), 12 C.F.R. § 235 (2011), https://www.ecfr.gov/current/title-12/part-235.

[7] Jean-Charles Rochet & Jean Tirole, Cooperation Among Competitors: Some Economics of Payment Card Associations, 33(4) RAND J. Econ. 549-570 (2002).

[8] Mark D. Manuszak & Krzysztof Wozniak, The Impact of Price Controls in Two-sided Markets: Evidence from US Debit Card Interchange Fee Regulation, Finance and Economics Discussion Series 2017-074, Fed. Rsrv. (Jul. 2017), https://www.federalreserve.gov/econres/feds/the-impact-of-price-controls-in-two-sided-markets-evidence-from-us-debit-card-interchange-fee-regulation.htm.

[9] Benjamin S. Kay, Mark D. Manuszak, & Cindy M. Vojtech, Bank Profitability and Debit Card Interchange Regulation: Bank Responses to the Durbin Amendment, Finance and Economics Discussion Series 2014-77, Fed. Rsrv. (Sep. 2014), https://www.federalreserve.gov/econres/feds/bank-profitability-and-debit-card-interchange-regulation-bank-responses-to-the-durbin-amendment.htm.

[10] Supra note 7 at 21.

[11] Id.

[12] Benjamin S. Kay, Mark D. Manuszak, & Cindy M. Vojtech, Competition and Complementarities In Retail Banking: Evidence from Debit Card Interchange Regulation, 34 J. Financ. Intermed. 91–108 (2018), at 104.

[13] Vladimir Mukharlyamov & Natasha Sarin, Price Regulation in Two-Sided Markets: Empirical Evidence from Debit Cards, SSRN (Nov. 24, 2022), https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3328579.

[14] Supra note 3.

[15] 12 C.F.R. § 235.1

[16] Regulation II (Debit Card Interchange Fees and Routing), Fed. Rsrv., https://www.federalreserve.gov/paymentsystems/regii-data-collections.htm; Consumer Price Index: All Items for the United States, Fed. Rsrv. Bank of St. Louis, https://fred.stlouisfed.org/series/USACPIALLMINMEI (last visited Aug. 10, 2022).

[17] Wang et al., supra note 4. Some merchants saw their acceptance costs increase because—prior to Dodd-Frank’s price controls—some merchants, especially smaller merchants, had received discounts on acceptance costs. But the imposition of price ceilings also effectively created a price floor, leading some merchants to pay higher fees than previously.

[18] Supra note 13.

[19] Id. at 4.

[20] Manne, Zywicki, & Morris, supra note 5.

[21] Id. at 30.

[22] Id. at 30-31.

[23] Robin A. Prager, Mark D. Manuszak, Elizabeth K. Kiser, & Ron Borzekowski, Interchange Fees and Payment Card Networks: Economics, Industry Developments, and Policy Issues, Finance and Economics Discussion Series 2009-23, Fed. Rsrv. (Jun. 2009), available at https://www.federalreserve.gov/pubs/feds/2009/200923/200923pap.pdf.