Adding a Warning Label to Rewheel’s International Price Comparison and Competitiveness Rankings

By

- Christian Dippon, Ph.D., NERA Economic Consulting*

- James Alleman, Ph.D., University of Colorado Boulder

- Teodosio Pérez Amaral, Ph.D., Universidad Complutense de Madrid

- Aniruddha Banerjee, Ph.D., Independent Consultant

- Gaël Campan, Ph.D., Montreal Economic Institute

- Jeffrey Church, Ph.D., University of Calgary

- Robert Crandall, Ph.D., Technology Policy Institute

- Eric Fruits, Ph.D., International Center for Law & Economics

- Bronwyn Howell, Ph.D., Victoria University of Wellington

- Jerry Hausman, Ph.D., Massachusetts Institute of Technology

- Justin (Gus) Hurwitz, J.D., University of Nebraska

- Mark Jamison, Ph.D., University of Florida

- Seongcheol Kim, Ph.D., Korea University

- Roslyn Layton, Ph.D., Aalborg University

- Stanford Levin, Ph.D., Southern Illinois University Edwardsville

- Daniel Lyons, JD, Boston College

- Geoffrey Manne, J.D., President, International Center for Law & Economics

- Petrus Potgieter, Ph.D., University of South Africa

- Paul Rappoport, Ph.D., Temple University

- Georg Serentschy, Ph.D., Serentschy Advisory Services

- Lester Taylor, Ph.D., University of Arizona

- Dennis Weisman, Ph.D., Kansas State University

- Jason Whalley, Ph.D., Northumbria University

- Xu Yan, Ph.D., Hong Kong University of Science and Technology

|

The Internet is a fabulous means of communication. However, the Digital Fuel Monitor by Rewheel/research is a prime example of misinformation on the Internet.[1] To curb the spread of false information, social media platforms have started applying warning labels to content they believe the facts do not support. Still, far too many false claims have attracted attention because separating fact from fiction on the Internet often requires a specific expertise. In this paper, the authors apply their expertise about mobile wireless markets to expose the false claims put forth by Rewheel/research in the recent publication of its Digital Fuel Monitor. We find the Rewheel rankings to lack academic rigor owing to an unsuitable analytical concept, unrealistic assumptions, and the omission of marketplace realities. Counterintuitive results confirm the rankings’ ineptness.

Rewheel, a Finnish consultancy, periodically issues reports that it portrays as international competitiveness comparisons of retail prices for mobile wireless services across the globe; however, these comparisons are not accurate representations of the state of competition in the mobile wireless world. In these reports, Rewheel assigns providers and countries international ranks and various competitive labels. For example, Rewheel ranks a country with alleged high prices a laggardand considers itleast competitive. Conversely, countries that Rewheel views favorably obtain a most competitive ranking. As with much of the information on the Internet, Rewheel follows the freemiummodel. That is, it publishes attention grabbing headlines and some colorful charts for free, but anyone seeking to understand more about the derivation of the data must pay Rewheel’s fees for the full content.

Mirroring much of the free content on the Internet, Rewheel’s rankings are unscientific and erroneous. Unfortunately, this contributes to the spread of misinformation about the state of competition in mobile wireless markets. Rewheel should be subject to the same warning labels as those placed on other suspicious information. Before turning to the shortfalls of the Rewheel rankings, we highlight that valid inferences regarding the competitiveness of mobile wireless service provisioning in a country cannot be made from a simple, unadjusted ranking of international prices. Countries differ in many aspects including network quality, consumer preferences, income, regulatory and legal environment, factors of production costs, and market size. These and many other differences among jurisdictions contribute to price variations. A proper international comparison considers these factors and compares the value proposition not simply prices.

In its recent ranking exercise, Rewheel ranks providers and countries by purportedly averaging the retail prices of 10 retail service plans. The 10 plans include five smartphone plans on 4G or 5G networks with varying levels of voice allowances, data allowances, and download speeds. Rewheel also includes three mobile broadband data-only plans and two home broadband (fixed wireless) plans. This exercise finds an average of €109 (US$127) for Canadian mobile wireless providers TELUS, Bell, and Rogers. Rewheel sweepingly declares that these providers offer “the least competitive monthly prices.”[2] With an average price of €29 (US$34), Finnish provider Elisa wins Rewheel’s distinction of offering “the most competitive … monthly prices.”[3] The Rewheel story is easy to understand. It is also completely wrong.

|

Comparing the prices of a collection of products (baskets) is not new. Prior to the introduction of the Internet, analysts used basket prices to compare supermarket prices. That is, they compared the costs of identically filled shopping carts across supermarkets. However, Rewheel’s application of the basket method is not appropriate for comparing prices of different mobile wireless services. Rewheel created its own version of the basket method that includes the calculation of meaningless averages, random combinations of different services, improper assumptions, and factual errors. Not surprisingly, as evidenced by the results derived by Rewheel, the rankings are incorrect and counterintuitive. We find Rewheel’s rankings are of no value in comparing prices and assessing the level of competition in wireless markets.

Comparing total grocery bills for two identical shopping carts from two different supermarkets might be a rational approach. However, knowing the average price of the items in the shopping cart clearly is useless especially when including a wide range of items. Nevertheless, Rewheel does just that – it compares average prices across varying items (in this case services). Knowing that the average price of a certain T-Mobile USA smartphone, tablet, and home Internet plan is €106 (US$125) is about as useless as knowing that the average price per item in a shopping basket containing a six-pack of beer, a dozen eggs, and a pound of oranges is US$10.

|

Rewheel does not explain why it would make sense to take the average of five smartphone plans, three data-only plans, and two wireless home Internet plans. Grocery bills are the sum of all items purchased at the supermarket. Presumably, consumers need all these items in their daily life. As such, the total grocery bill measures the household expenditure for food. Rewheel’s basket, however, does not represent anything. It does not represent an individual’s spending for mobile wireless services because subscribers do not need five smartphone plans. Subscribers also do not rely heavily on wireless home Internet access. Instead, the more prevalent means to access the Internet is through fixed broadband services offered by landline telephone and cable TV companies. Yet, fixed broadband services are missing from Rewheel’s basket. Thus, the average of Rewheel’s eclectic mix of services is meaningless. It certainly does not represent a consumer’s wireless spending, and it does not represent the average price of a particular service. Rather, the Rewheel basket is a mix of substitute and complementary items. Moreover, Rewheel’s basket overlooks an important item (fixed broadband) on a consumer’s shopping list.

The must-carry assumption. Rewheel assumes that in order for markets to be competitive all providers in the world mustoffer all 10 service plans in its basket. If a provider does not offer a specific plan, then that provider is “assigned the highest monthly price among all 168 operators.”[4] For example, per Rewheel, Vodafone in India does not offer a fixed wireless broadband plan with at least 1,000 GB of data and download speeds of 100 Mbps or faster. Therefore, under the must-carry assumption, Rewheel artificially increases Vodafone India’s price average by loading it with the highest observed international value for this plan. In this case, the highest monthly price that Rewheel found belongs to a provider in the United Kingdom by the name of EE Limited (formerly Everything Everywhere). Thus, Vodafone India’s average includes a plan price from the United Kingdom. Rewheel applies this exact price to no less than 133 of the 168 providers (79 percent) in its ranking.

Rewheel’s irrational assumption is akin to imputing that the price of buffalo meat in a vegetarian supermarket is the same as the price of the most expensive buffalo meat vendor in the world. There is no economic or statistical support for this approach. In fact, in some countries, Rewheel’s must-carry plans cannot even be offered because the regulator has yet to release 5G spectrum. Rewheel’s baseless assumption renders the comparison useless because the average price by which providers and countries are ranked is not composed of retail prices faced by subscribers in the respective markets.

The non-specialization assumption. Rewheel’s ranking unrealistically assumes that for a provider (and thus the market) to be competitive it must not specialize but must offer and compete on all plan levels selected by Rewheel. This assumption is counter to basic economic principles.

A rational business enterprise introduces service plans for the express purpose of earning positive economic profit. Based on this objective, an enterprise derives a strategy that determines its retail offerings. Unlike Rewheel’s assumption, this does not mean that all competing enterprises offer the same services. Quite the contrary, competitors seek to distinguish themselves from their peers through price and non-price service attributes and by offering new and innovative services to gain a competitive advantage.

Consider, for instance, Freedom Mobile Inc., a Canadian regional mobile wireless provider owned by Shaw Communications, a Canadian cable provider. Freedom does not offer fixed wireless broadband services. Rewheel incorrectly deduces from this observation that Freedom’s offerings are not competitive. Freedom is a profit-maximizing firm; therefore, its decision not to offer fixed wireless services is simply an indication that the service does not align with the company’s strategic blueprint. Freedom finds that it can best compete by specializing in offering mobile wireless services in select regions of Canada. Rewheel’s approach also overlooks service providers that mainly specialize in fixed wireless broadband, like Xplornet, which is not listed among Canada’s providers.

The standalone assumption. Rewheel incorrectly assumes that consumers demand and are supplied with standalone only plans. In Rewheel’s ranking system, there is no demand for bundled service plans where a consumer purchases mobile wireless service along with TV, fixed Internet, or fixed telephony services. However, in reality, many subscribers bundle their services and thereby receive discounts on mobile wireless and broadband services. Relatedly, mobile wireless providers offer bundled services to competitively distinguish themselves. For instance, AT&T offers free HBO Max subscriptions to some of its customers.[5] By ignoring bundled offerings and discounts, Rewheel overstates actual consumer expenditures.

The no-sharing assumption.The Rewheel ranking exercise also contains the untenable assumption that the increment of demand is always one mobile phone line and never more, which is false. For instance, AT&T offers unlimited plans starting at US$30 “when you get 5 lines.”[6] Rewheel ignores this US$30 price point. Instead, it uses a US$65 price point, which is AT&T’s lowest price for an unlimited plan with a single line.[7] Yet, as of 2015, an estimated 68 percent of US subscribers were part of a shared or family plan.[8] By ignoring the fact that subscribers purchase in increments of more than one line, Rewheel significantly overstates US prices.

Specifically, instead of the US$65 price assumed by Rewheel, the average price of AT&T’s cheapest unlimited plan is closer to US$41.[9] For this example alone, Rewheel’s assumption results in an overstatement of prices by 58 percent. The popularity of shared plans in the United States is not the exception. In Canada, approximately half of mobile wireless subscribers purchase a plan shared with others.

The price-only assumption.Rewheel’s incorrect ranking assumes that consumers only care about price and not what they get in exchange for their money. In building its average, Rewheel looks for the price of the cheapest plan that meets or exceeds its selection criteria.[10] The plans offered by different providers exceed the selection criteria by different amounts. Yet, Rewheel ignores this fact and creates an apples-to-oranges comparison where consumers do not care about anything but price. Omitting the value of additional minutes, data allowances, or faster download speeds is not realistic.

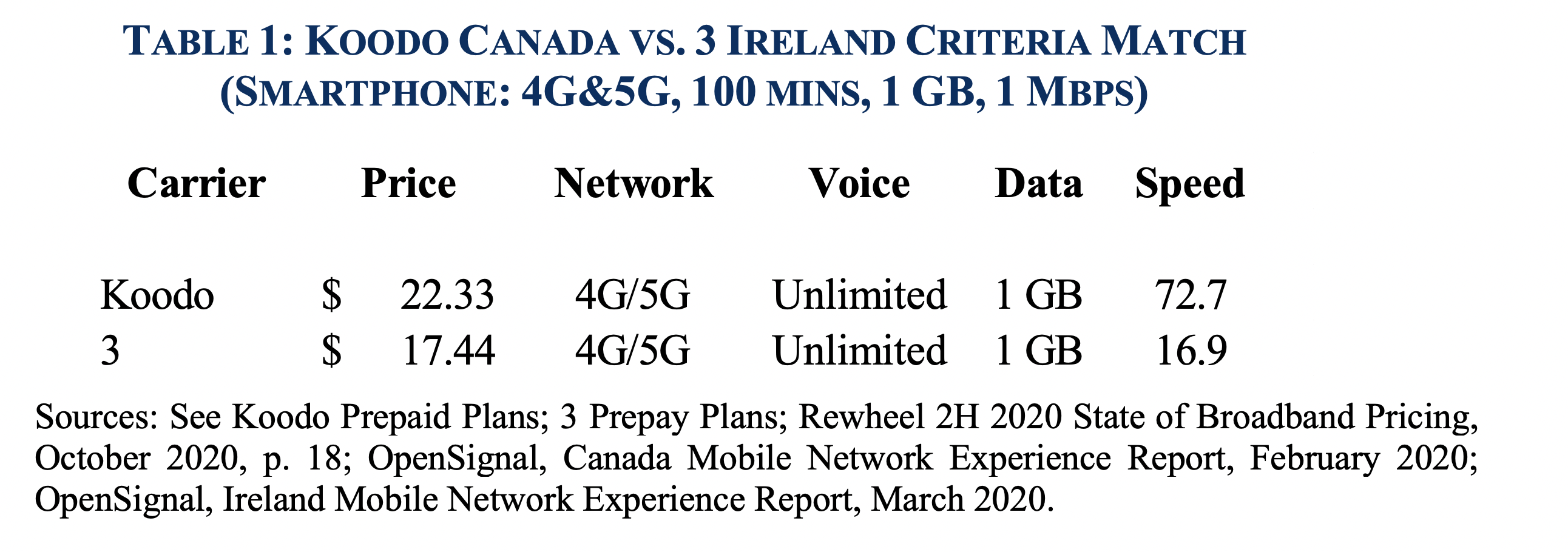

A real-world example illustrates the consequences of this baseless assumption. Koodo is a mobile wireless provider in Canada that is part of the TELUS family of brands. The cheapest Koodo plan that meets Rewheel’s criteria for its first plan (i.e., Smartphone: 4G&5G, 100 mins, 1 GB, 1 Mbps) is a plan priced at US$22.[11] Now, consider the Irish mobile wireless provider called 3 whose plan meets or exceeds the same Rewheel criteria and is priced at US$17.[12] Rewheel heralds 3 as a cheap provider and labels TELUS as “least competitive.”[13] Table 1 provides the details of these two plans.

As the table reveals, for an additional US$5 per month (not withstanding other differences), Koodo offers download speeds that exceed those offered by 3 by a factor of over four. By ignoring non-price service attributes, Rewheel assigns a least competitive label on Koodo and a most competitivelabel on 3, thereby incorrectly assuming that consumers do not care about network quality and that they would not be willing to pay for a higher speed. Presumably, Rewheel would also argue that consumers are not willing to pay more for high-grade Japanese wagyu beef than they would pay for a cheaper cut of beef.

The cost-equality assumption.Rewheel also ignores that building a network costs money. Rewheel unrealistically assumes that building a network in Finland (which Rewheel highlights as a competitive market) costs the same as building a network in Canada (which Rewheel highlights as a noncompetitive market) even though Finland has a population one-sixth the size of Canada and a landmass one twenty-ninth the size of Canada. Finnish mobile wireless providers also pay about 90 percent less for radio spectrum relative to their Canadian peers.[14] For a business enterprise to remain viable, it must recover its costs and earn a competitive return. Because all providers face buildout and spectrum costs, they are reflected in the retail prices for mobile wireless services. Yet, in Rewheel’s utopian world, all providers face the same costs.

|

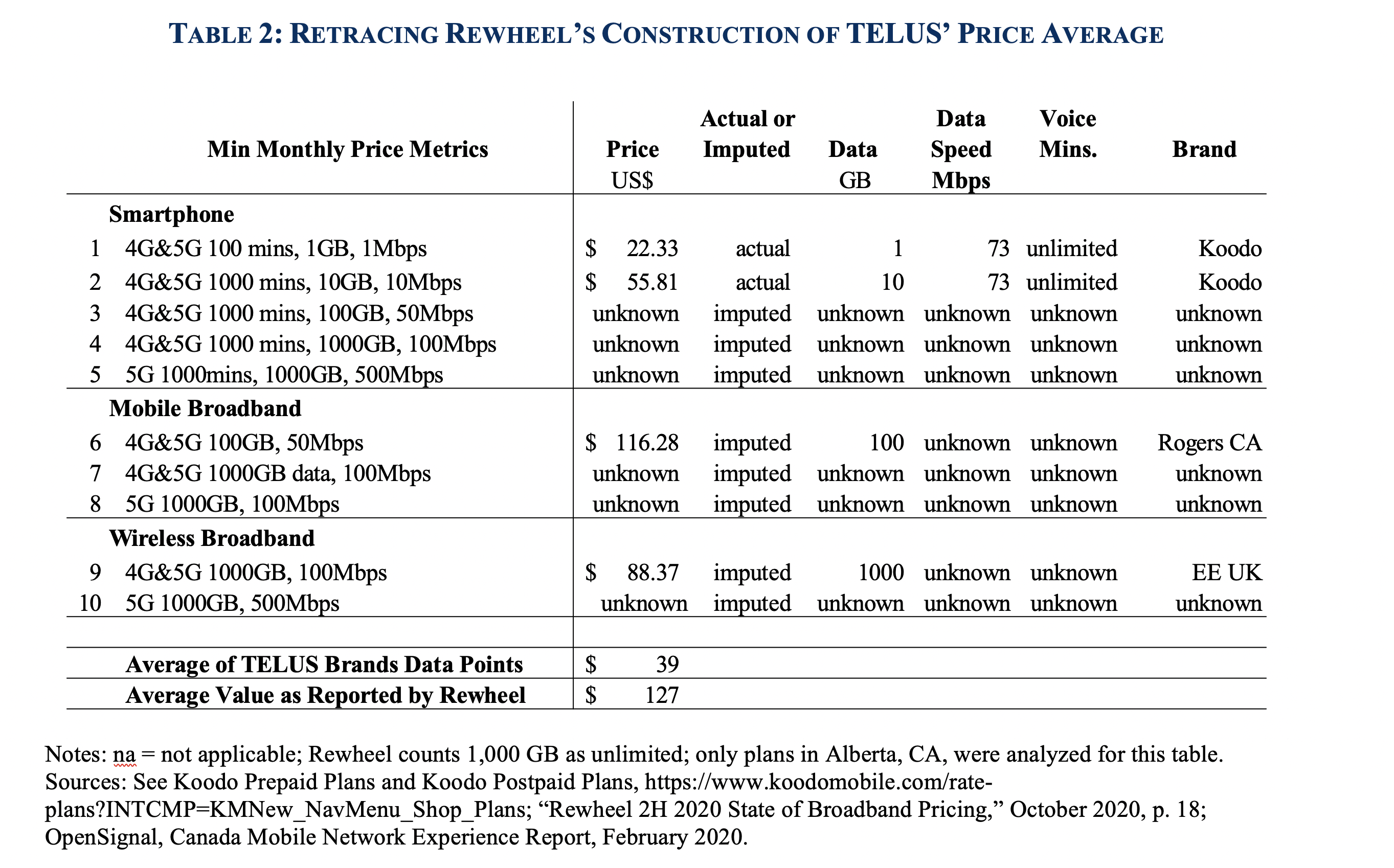

The counterintuitive results.Two simple examinations demonstrate that Rewheel’s results are incorrect and offer no economic insight. First, we retraced Rewheel’s construction of the ranking average for one mobile wireless provider, that is, TELUS, a mobile wireless provider in Canada, which offers three brands – TELUS, Koodo, and Public Mobile. Examining the websites of the TELUS family of brands reveals that across the three brands TELUS only offers two of the 10 specific plans that Rewheel uses for its average. Specifically, as shown in Table 2, Koodo offers a plan at US$22.33 that meets and exceeds the first Rewheel plan (i.e., Smartphone, 4G&5G, 100 minutes, 1 GB, 1 Mbps). Koodo also offers a plan at US$55.81 that meets and exceeds the second Rewheel plan (i.e., Smartphone, 4G&5G, 1000 minutes, 10 GB, 10 Mbps). The TELUS brands do not offer any of Rewheel’s other eight specific plans although TELUS offers many other plans.

Rewheel ignores the fact that it misses 80 percent of the sample and simply substitutes the missing data points with “the highest monthly price among 168 operators.”[15] The data provided by Rewheel in its free Public Version on the Internet does not disclose what prices it used in every instance where a provider did not offer a plan. However, it is possible to ascertain that for the ninth plan (i.e., fixed wireless broadband plans with at least 1,000 gigabytes and 100 Mbit/s peak speed) Rewheel used US$88.37, which is the price for the most expensive plan that Rewheel found for this plan type. EE Limited in the United Kingdom supposedly offers this plan. For the sixth sample plan, Rewheel blends a price point of US$116.28 from Rogers, another Canadian mobile wireless provider, into TELUS’ average.

As the TELUS example demonstrates, Rewheel’s ranking is pure fiction. Aside from its theoretical failings and the fact that it misses the plans purchased by 50 percent of Canadians, Rewheel observes only two data points for TELUS, which average €34 (US$39). Based on Rewheel’s ranking, an average of €34 would put TELUS in third place out of 168 providers, which would appear to make it one of the most competitive mobile wireless providers in the world. However, Rewheel reports TELUS’ average at €109 (US$127), which is purely an artifact of Rewheel’s methodology that assigns TELUS the highest price for eight out of 10 sample plans – plans that TELUS does not even offer.

Second, in Rewheel’s world where only price matters, one would not expect providers with the most competitive monthly prices to be in the same market as providers with the least competitive prices. The reason for this is simple. Like any other rational economic agent, subscribers would not select a more expensive plan over an identical but less expensive plan. However, the myriad of unreasonable assumptions in Rewheel’s ranking produces this counterintuitive result.

Consider the case of Romania where Rewheel calculates average prices of US$69, US$70, US$122, and US$123 for Orange, Vodafone, RCS-RDS, and T-Mobile, respectively. In the same order, per Rewheel, these prices would rank the four providers as 23, 25, 141, and 146. This ranking presumably offers Orange and Vodafone a label of most competitive, whereas RCS-RDS and T-Mobile are least competitive. If the Rewheel price-only world were accurate, RCS-RDS and T-Mobile would not have sustainable business cases because Orange and Vodafone allegedly offer better prices and thus would attract all market demand. Nevertheless, the actual market shares in Romania tell a different story. RCS-RDS and T-Mobile have market shares of 12.6 percent and 18.7 percent, respectively.[16] It is counterintuitive that two alleged highly uncompetitive providers would attract about one-third of the country’s subscribers. We observed similar anomalies in other countries, including Finland, Switzerland, the United States, and the UK. These economic anomalies are prima facie evidence that Rewheel’s results are incorrect.

|

The warning label. Given the many theoretical and practical flaws and errors contained in the Rewheel study, we find it of no value when comparing prices internationally or establishing the level of competition in a country. A warning label informing readers about the lack of intellectual rigor and the misleading and incorrect nature of the Rewheel study’s results is appropriate and recommended.

[*] NERA Economic Consulting received financial support from TELUS Communications Corporation for the research and initial drafting of this paper. No other authors received compensation. All views expressed are those of the authors.

[1] See Rewheel/research, “4G&5G connectivity competitiveness 2020,” Digital Fuel Monitor, Rewheel research PRO study (Public Version), November 2020 (hereinafter Rewheel).

[2] Ibid, p. 1.

[3] Ibid.

[4] Ibid.

[5] See AT&T “Stream HBO Max with some AT&T unlimited plans,” https://www.att.com/support/article/wireless/KM1261921/.

[6] See AT&T Wireless Plans, https://www.att.com/plans/wireless/.

[7] Ibid.

[8] See Pew Research Center, “U.S. Smartphone Use in 2015, Chapter One: A Portrait of Smartphone Ownership,” p. 2.

[9] 30*0.68+65*0.32 = 41.20.

[10] For example, Rewheel collected “4G&5G mobile broadband plans with at least 100 gigabytes and 50Mbit/s peak speed” plans. (Rewheel, p. 3, (emphasis added).)

[11] See Koodo Prepaid Plans, https://www.koodomobile.com/prepaid-plans?INTCMP=KMNew_NavMenu_Shop_PrepaidPlans. Rewheel 2H 2020 State of Broadband Pricing, October 2020, p. 18.

[12] See 3 Prepay Plans, https://www.three.ie/buy/prepay.html#prepay-phone-plans; see also Rewheel 2H 2020 State of Broadband Pricing, October 2020, p. 18.

[13] Rewheel, p. 1.

[14] See Richard Marsden, Dr. Bruno Soria, and Hans-Martin Ihle, “Effective Spectrum Pricing: Supporting better quality and more affordable mobile services,” GSMA, February 2017, Figure 13.

[15] Rewheel, p. 11.

[16] Shares are for third quarter 2019 just prior to Rewheel’s data collection. (See TeleGeography, Country Profile, Romania, as of November 9, 2020, p. 32).